Weekly | Volatility Galore, $SATS Rollercoaster, Post-Catalyst Investing

We have seen some incredible two-way volatility over the past 6-7 trading days with the chance to opportunistically add and trim several names:

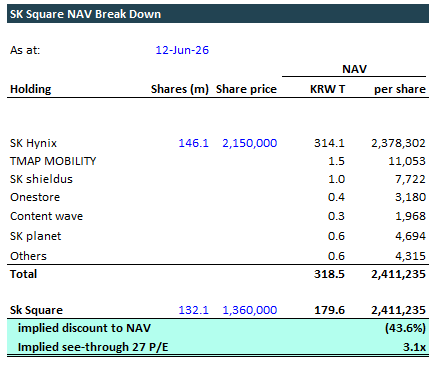

SK Square: 30% intra-week swing, trimming at new ATH

Did not pullback enough for us to compound back in and within days we were at a new ATH (KRW 1.41M)

Trimmed another ~8% at close to ATH levels at ~3x MOIC on our March buys

NAV discount compressed back to 43.6% by the end of the week after reaching pre-IBKR levels of ~48% on Monday

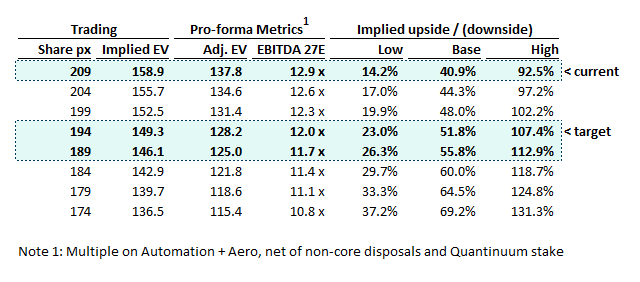

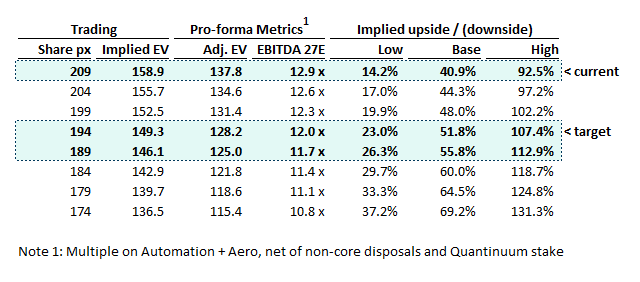

Honeywell: accumulation ahead of the spin-off

HON 0.00%↑ dipped back within our target range (<$210) and we are able to add between $206-209 ahead of the H 0.00%↑ ONA spin-off in less than 2 weeks

At our target levels we believe we are creating Automation + Aero at <13x 27E EBITDA

Still leaving some room for lower + potential post-spin dislocations however we have already bounced back to >$220 / share

Klarna: adding more ahead of 26th of June litigation verdict

On KLAR 0.00%↑ we added to our position in the $15-16 range

We like these levels independently of the impending litigation event

We have now received the full court filings from the Stockholm courts and are building conviction around a decent sized expected value payout as a % of market cap. Will be releasing our full findings ahead of the event, so stay tuned.

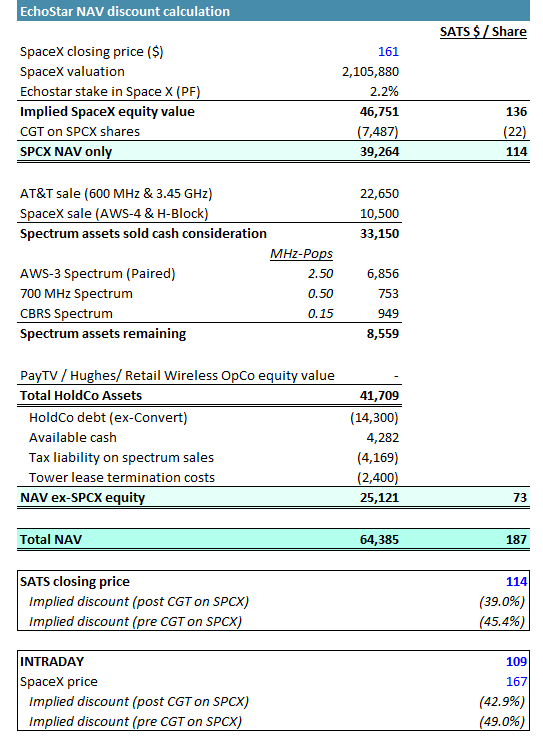

EchoStar Rollercoaster

With the SPCX 0.00%↑ IPO this week, SATS 0.00%↑ was all over the place!

We discussed our revised thought process last week going into the event: a revised bias towards maintaining exposure with some opportunistic sell-orders in the >$130 range if we got there.

While we did get triggered on some additional sales mid-week, we did not anticipate the level of dislocation on Friday and at some point the levels got too juicy to pass up.

With most of our original buys from late 2025 in the $75-$85 range, we set the bar high on any new purchases. At $108-112 we found ourselves in a situation where:

We were post FCC approval on the spectrum sale transaction

SPCX 0.00%↑ was trading live at a valuation well in excess of our original underwrite

On an intraday basis, we actually had a good 20-30 minutes where SPCX 0.00%↑ bounced back from ~$155 to >$168 while SATS 0.00%↑ remained below $110. This made very little sense to us and finally decided to compound back in while simultaneously placing a small SPCX 0.00%↑ hedge (~20%) on HL.

So where does this leave us? Here is a quick breakdown of where we are:

At SPCX 0.00%↑ closing price of $161, the attributable value per share EchoStar’s stake is $136 (gross) or $114 (net of CGT)

In other words, at the closing price of $114 EchoStar is trading at exactly the value of its SpaceX holdings net of CGT

Of course, EchoStar has significant other assets on balance sheet – even if we zero out any OpCo equity value, there is $42B of spectrum asset value of which 78% is in the form of cash receivables)

Net of HoldCo liabilities, this equates to an incremental $73 / share

At peak intraday dislocation we calculate that the (pre-CGT) NAV discount reached close to 50% after settling at 45.4% by CoB.

On NAV spread trades, we’ve discussed our approach in the past. We like to be opportunistic and exploit the move from completely egregious to only moderately egregious rather than strive for the perfect structural discount which can often be an elusive game. We think Friday represented excessive dislocation and were more than happy to reload in that range.

Post-Catalyst Investing?

Sometimes taking a position after a news-driven move can be highly +EV over a short time frame if assessed properly. There is a natural tendency to assume that big news gets priced close to perfection very fast.

Most recently, we covered easyJet and highlighted how there was a lot of room to run post the original announcement. In this scenario, it was clear that the Company was trading at a steep discount to break-up value. The Castlelake news shined light on the discount but even then it took over a week for the market to digest fully as it became clearer that there was a real commercial case to be made at a significantly higher level with workarounds for and legal / regulatory hurdles.

We hypothesised that Castlelake would have enough room to bid well north of 500p / share – and after 4 days of publishing we are now already there. While we annoyingly did not participate despite paying close attention to the situation, this was a relatively straightforward >20% trade opportunity (and perhaps more) over a 1 week time horizon.

We had a similar situation on EchoStar, where even AFTER the Spectrum sale to SpaceX SATS 0.00%↑ shares languished in the $75-85 range after an initial move higher. There can be many reasons for such “delayed market efficiency” – in the case of EchoStar there was a large credit / special sits oriented stakeholder base happy to get out on the initial move. Lack of natural long-term holders + the lack of research coverage on a name that was stressed/distressed meant that it took a few more months to overcome that initial technical sell pressure.

Something to keep in mind as similar situations pop up in the future!

On SATS, I've done a similar SoTP exercise, and I'm coming in lower. There are a few areas where we differ.

On SPCX stake, I think SATS owns 262m shrs, right? So multiplied by SPCX shr px of 161/shr, that is $42bn in pre-tax value. You have nearly $47bn in pre-tax so decent sized delta there. Your method is SPCX valuation x 2.2% SATS ownership. However, I'm guessing their diluted stake is lower than 2.2% after reflecting all the IPO/pref conversions/etc. I think it's simplest to calc their stake in terms # of shares which is known multipled by the SPCX shr price.

On the sale of spectrum to SPCX, I'm using $8.5bn versus your $10.5bn. I think the delta is SPCX is covering a future interest payment for SATS. However, that's just future burn avoided for SATS. It's not really an asset. That brings up another point of how to best reflect ongoing burn at SATS from corporate overhead + interest. I think that will end up justifying a discount to NAV over time, but that's for another day once we see the dust settle.

Lastly, on your cash balance. I think that might include some cash from DISH and Hughes. I think those are zeroes over the long term as debt likely exceeds fair value, so I assume that's not cash that is recoverable/usable at the SATS level. I think that's around $1.2bn.

So those 3 drivers explain $8bn delta, which is around $20-$25 per share in value.

Will review for any other differences and happy to compare notes if of interest.