Deep | easyJet vs. Castlelake: Put Up or Shut Up

Why a Castlelake bid is still far from being fully priced in

easyJet is currently in an offer period following Castlelake’s recent takeover overtures. Under the UK Takeover Code, Castlelake now has until 5:00pm on June 26th to either put-up or shut-up.

Specifically, this means announcing a firm (binding) intention to make a formal offer within 28 days, taking us to a July 24th Offer Date (at the latest) and from there kickstarting the official takeover timetable.

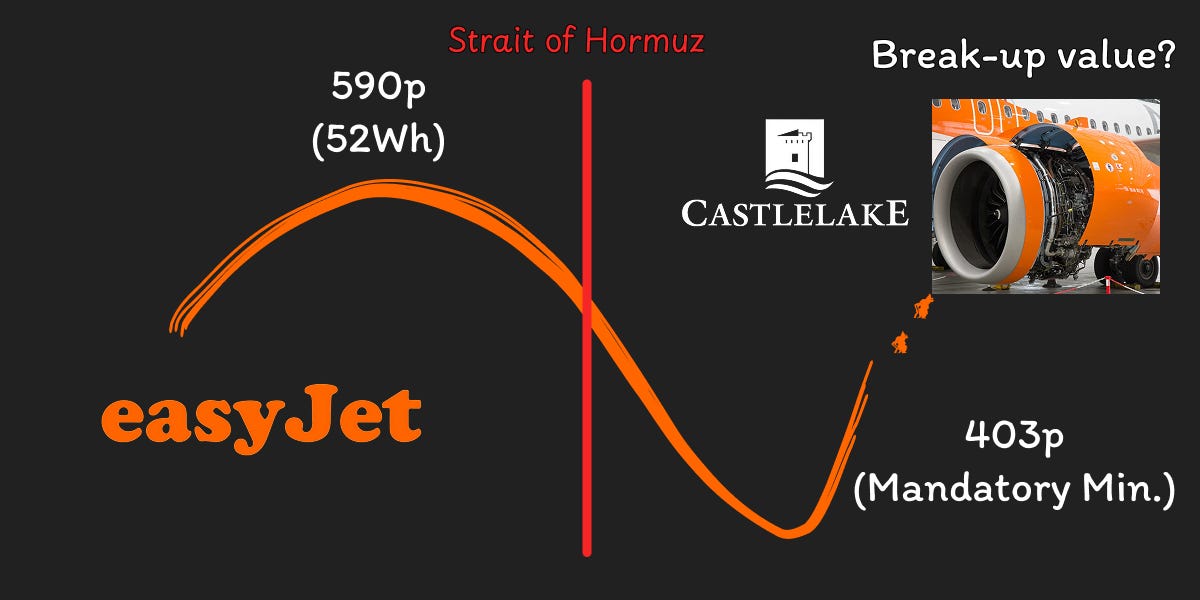

Having already acquired a >2% stake in the open market, Castlelake is subject to a mandatory minimum price for any offer at 403p / share (highest recent purchase), a level which is 32% below easyJet’s 52Wh.

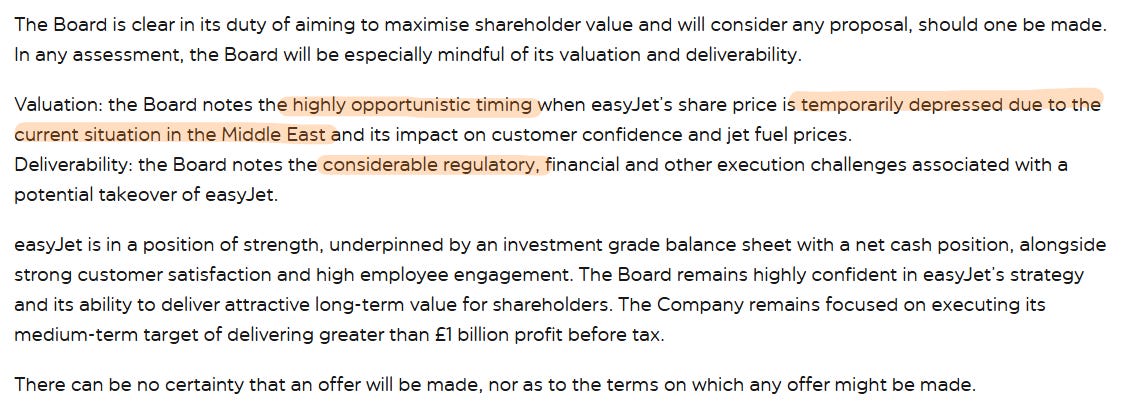

easyJet’s Board (as one might expect) dismissed Castlelake’s initial approach as being highly opportunistic following the Iran crisis and the knock-on effect on jet fuel prices and potential demand, while also questioning the deliverability of a transaction (alluding to foreign ownership rules).

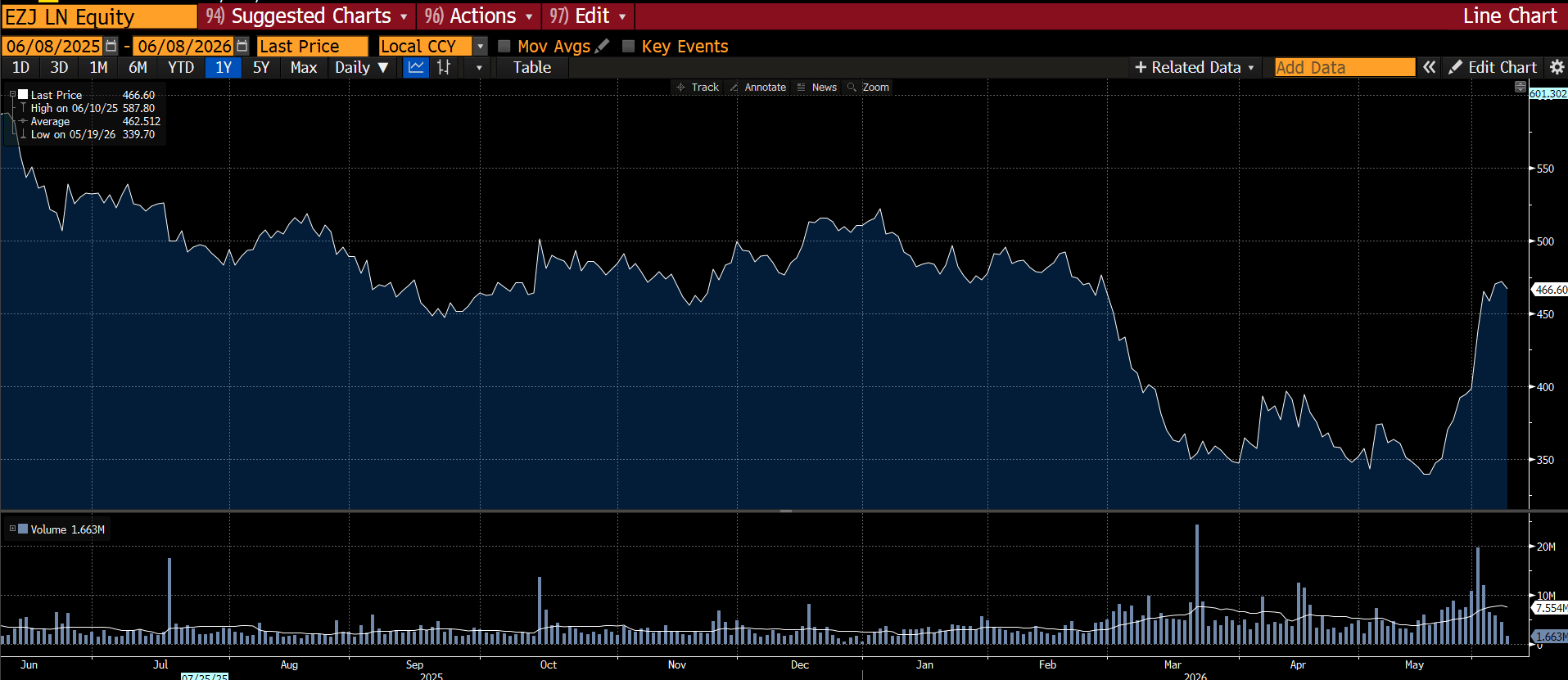

And so the dance begins. As at the time of writing, easyJet is trading at 469p / share.

While the analyst community agrees that 469p represents a discount to metal value, we take a look at the incremental swing factors that they are missing and why Castlelake likely has more room left in the tank.

The Middle Child

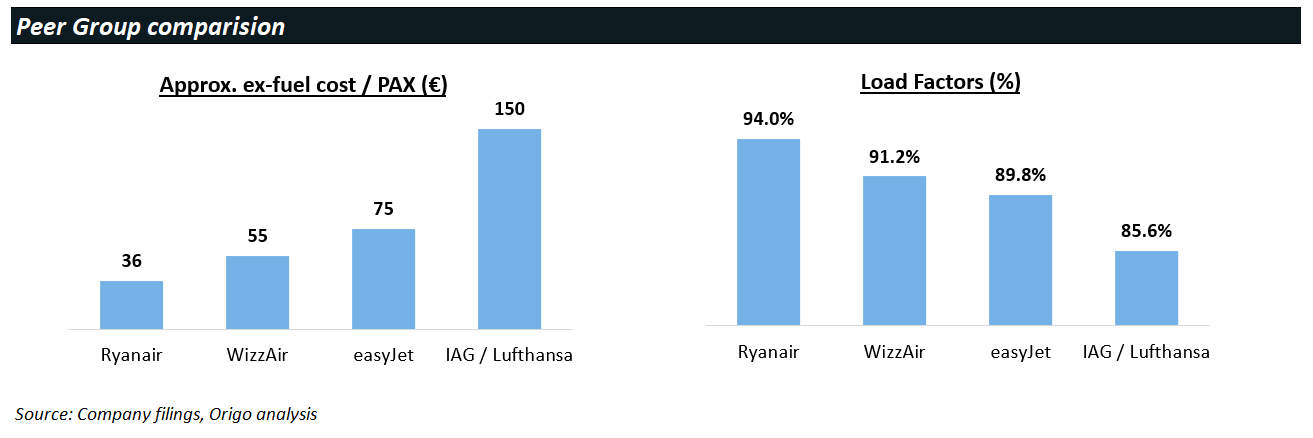

A competitive European LCC market has kept a lid on performance even ahead of the the Iran crisis. While historically profitable, easyJet has mostly traded at a discount to peers in recent years due to its hybrid market positioning and tougher unit economics.

easyJet is at the high-end of the LCC market when it comes to its opex per passenger (ex-fuel). This is in part due to higher labour costs & disruptions, but also due to the fact that – while valuable – it operates in more primary, slot-constrained airports with higher associated airport and handling costs.

As a result, easyJet also charges higher fares vs. the ULCCs and tends to suffer from lower load factors.

On the other side of the spectrum, flag carriers such as IAG / Lufthansa operate under a fundamentally different model offsetting their higher cost base with business class seating and long-haul flights.

In other words, easyJet in a somewhat awkward middling position within an already competitive market in need of further consolidation.

A Balance Sheet Story with a Ton of Optionality

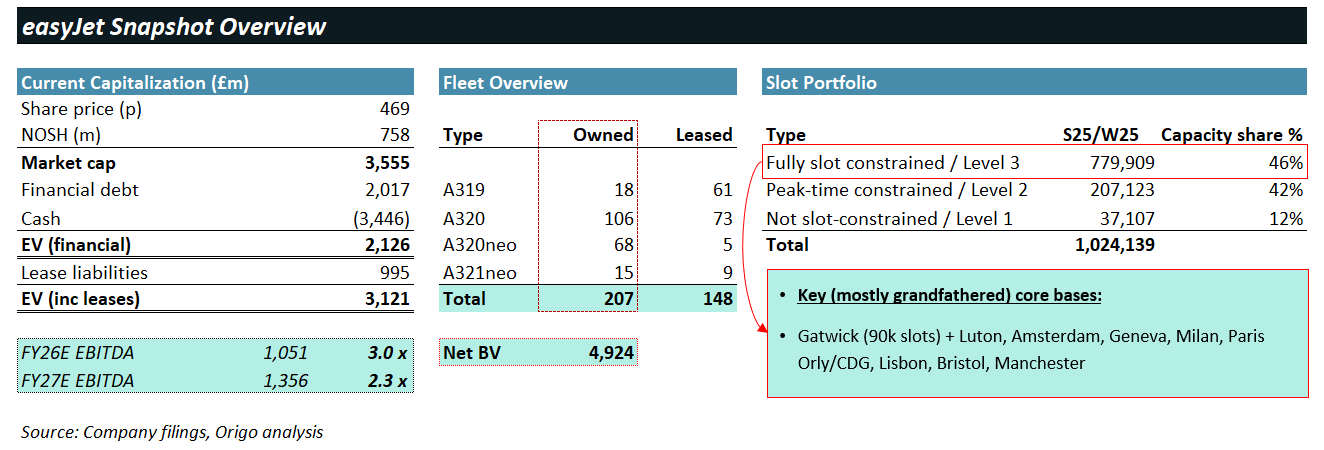

Despite this, easyJet’s balance sheet is very healthy. They own a majority of their fleet and have a £1.4B financial net cash position.

Additionally, they control a valuable slot portfolio with grandfathered landing rights in a number of core European airports, including 90k slots in Gatwick (~123 daily pairs). While historically marked at £155m within intangibles, the market value of these rights is likely materially higher with the value of prime daily slot pairs being potentially worth well north of >£2M each.

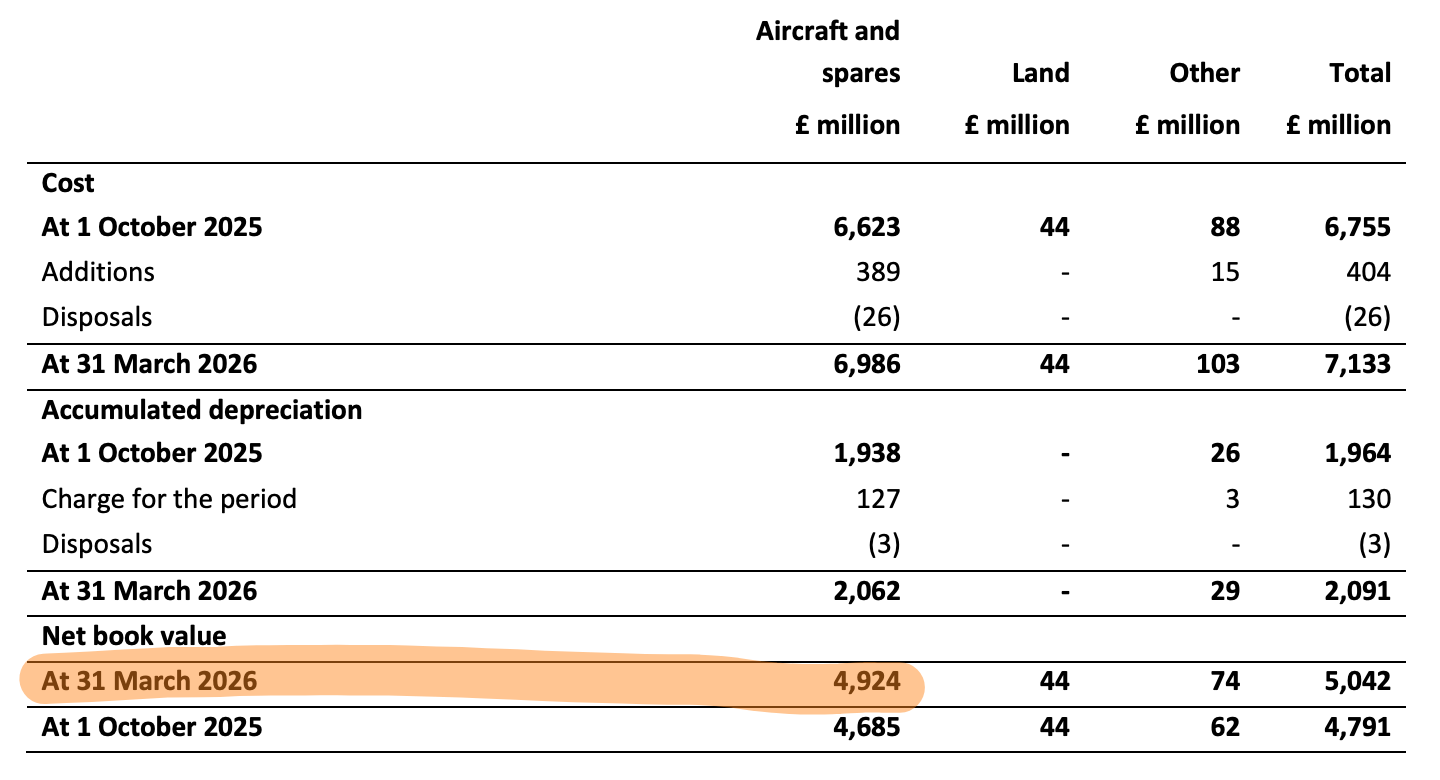

The owned fleet is carried on the books at a depreciated cost basis of £4.9B (which includes £626M related to advanced orderbook payments).

Again, the owned fleet value is likely understated here given the continued increase in engine values and downside protected part-out nature of the portfolio.

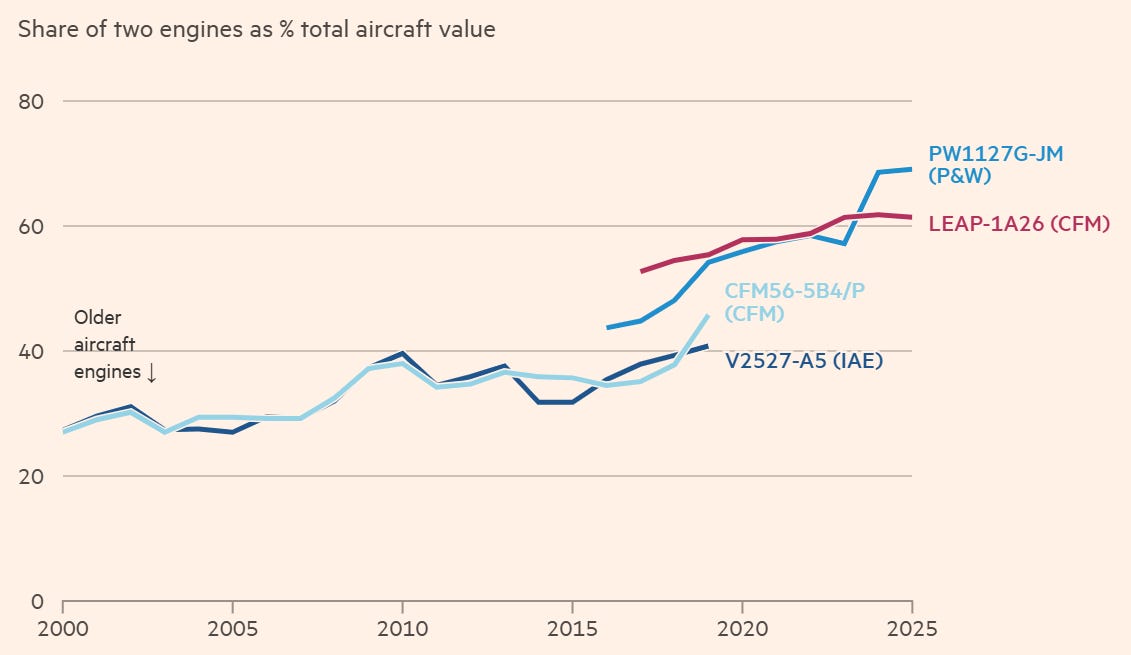

easyJet’s fleet is 100% narrowbody and 100% CFM engines which is as liquid as it gets. You may be familiar with CFM (Chris Hohn’s number one exposure via TCI’s holdings in GE Aerospace and Safran) – a great business which holds a quasi-monopolistic market position in narrowbody engines (P&W being the charitable competitor) with supply constrained escalation rates and pricing power. Labour shortages and MRO bottlenecks underpin valuation floors as engines represent an increasingly material % of ageing aircraft values.

In particular, their older generation A319/A320s are likely understated on an accounting depreciation basis vs. market value.

While we do not have the line-by-line breakdown of the mx adjustments by MSN, we can get to a reasonable half-life value ballpark range for the fleet.

Now let’s dig into how Castlelake might be looking at this, our assessment of a break-up value range including potential leakage & areas for optimisation. From there we reverse-engineer a potential range Castlelake may come in at.