Weekly | Apollo & Anthropic Jumbo deal, Klarna Free Option, $HON Quantinuum IPO

Apollo, Blackstone & Anthropic Jumbo Deal on TPU Chips

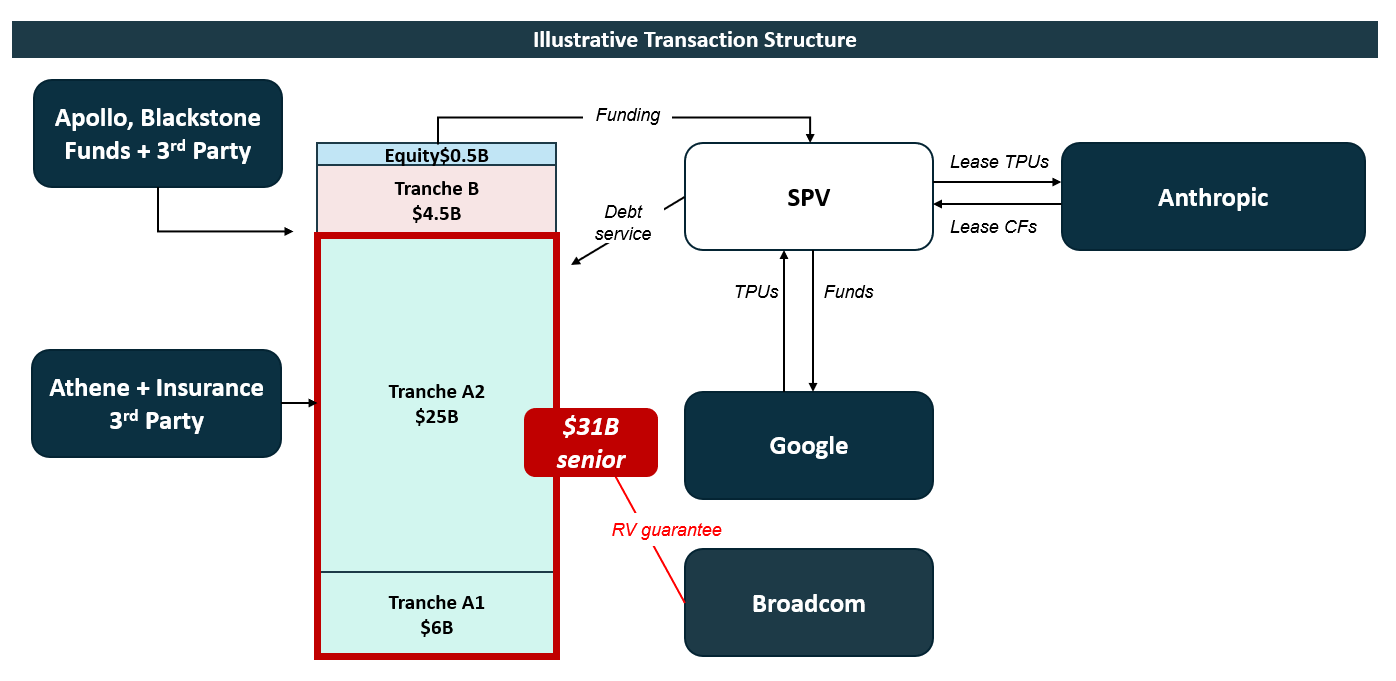

This week we saw APO 0.00%↑and BX 0.00%↑ announce a monster $36B TPU deal involving Google, Anthropic and Broadcom. While the deal is still fluid, our understanding of the transaction based on various news reports is as follows:

SPV to be funded via $35.5B of private debt and $0.5B of equity (est.)

Debt is split between

Senior debt of $31B (A1 = $6B and A2 = $25B)

Junior piece of $4.5B

SPV acquires Google TPUs (on a delayed draw basis as and when delivered) and subsequently leases these to Anthropic

Anthropic lease cashflows is utilised towards debt service

Senior tranche benefits from a Broadcom residual value guarantee (thus achieving investment grade status) while the junior/equity is more exposed to TPU chip RV risk

This type of transaction is very much in keeping with the multiple case studies we covered when looking at Athene:

Apollo asset management originates the transaction

Anthropic gets chips without having to use its balance sheet

Google/Broadcom get a large deal done

Athene leans on Broadcom RV guarantee for IG-rating (and in turn the RV-guarantee is off-balance sheet debt from Broadcom’s perspective)

Apollo / BX place a vertical slice of the cap stack between its own funds + insurance vehicles while incrementally getting syndication fees

Post syndication Apollo will facilitate trading which in turn improves capital efficiency at Athene

We will see how the final deal looks like but expect many more similar transactions over the coming quarters.

Klarna: unexpected catalyst?

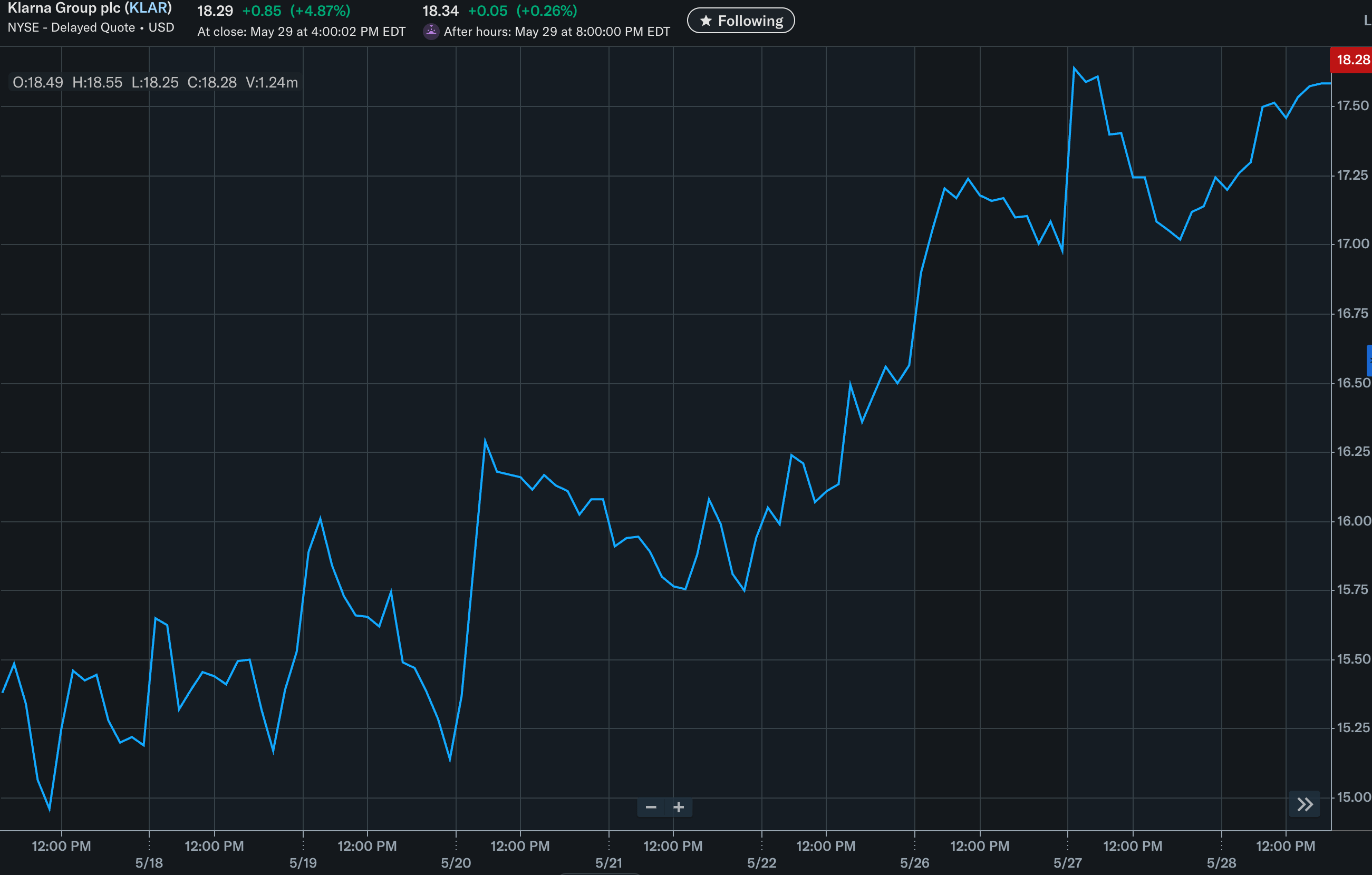

Our KLAR 0.00%↑ position has been working out well so far and is up ~22% since our May 16th write-up. While price action is king, it is a common ego mistake to assume 100% thesis correlation when things move your way.

Hence we will attribute initial performance as follows: 1/3 = identifying when it was technically oversold, 1/3 = broader market strength and 1/3 = initial thesis validation as Q1 results got digested.

The good news being that we actually think this has a lot more room to run as the thesis component strengthens over the next 2-3 quarters and we move beyond the name being merely a dead-cat-bounce.

Now, there is one other factor which could explain some of the price action, although for the moment we would be in the camp that this is purely a free option given the lack of sell-side / broader coverage (unless someone, somewhere, knows something).

On June 10th we should receive a verdict on the Klarna vs. Google $8.3B anti-trust lawsuit (yes, 140% of Klarna’s market cap).

This is a lawsuit that stems from the European Commission’s 2017 ruling where they fined Google for €2.4B in the Google shopping case.

PriceRunner filed for follow-on damages in the Swedish courts (with an initial claim of ~€2.2B).

Klarna inherited the case via its acquisition of PriceRunner in 2022 and subsequently updated the damages claim to $8.3B once the full trial was underway in late 2025. The court was supposed to deliver judgement on April 10th but extended the verdict date to June 10th.

A couple of things to note:

PriceRunner / Klarna are using a litigation funder (share a % of the ups)

PriceRunner legacy shareholders will likely have negotiated an earn-out

$8.3B is likely a “kitchen sink” type of number

Notwithstanding the above, there is a very real chance that Google is found liable since the basis of the suit, the 2017 ruling, was upheld by the European Court Justice in 2024 – and there have been succesful comparable follow-on cases including:

Idealo vs. Google (Germany): German price-comparison site Idealo filed in 2019, claim was originally €500M, expanded to >€3.3M after the ECJ ruling. On 13/14 November 2025, the Berlin Regional Court ruled Google liable and awarded €465M (€374M in lost profits + €91M interest).

Twenga vs. Google (France): Paris Commercial Court ruled in November 2025 ordering Google to pay €51.5M

The Idealo case is particularly interesting given damages awarded were more or less inline with the initial claim.

A potentially realistic outcome would be a ~€1-3B award in which KLAR 0.00%↑ receives ~50%, which would be ~15% of market cap at the mid-point.

While court records are publicly available in Sweden, you have to make a formal request (which we have done) to receive any documents related to a case. We will share any potential incremental updates that come from that. Of course, caveating all the above with the fact that we are are not lawyers (just applying reasoning to known facts + some background experience in litigation claims).

Honeywell | Quantinuum IPO

Quantinuum is set to IPO this coming week and will be listed under the ticker $QNT. The indicative price range is $45-50 and the book currently ~2x oversubscribed.

As is now a habit with pre-IPO names, we can refer to trade.xyz markets on Hyperliquid to catch a glimpse on valuation expectations post trading.

Based on these markets, $QNT is trading at $100 or ~$25B implied valuation which would be worth ~$19/share for Honeywell.

We would also note that many analysts are currently fully consolidating opex burn (run-rate ~$330M) and capitalising that number at over 17x (i.e. negative ~$9/share) – they will be switching to equity method ex-post so we may see further uplifts in SOTP / price targets coming from that.

You can refer to our original Honeywell write-up here (+ access to excel for paid subscribers).

Have a great end to the weekend!

Thank you. Good work

The fascinating thing about business decisions is they affect every aspect of society, from how we invest in research, to how people conduct their daily lives. It requires therefore a broad education and a profound understanding of basic psychology.

To give a simple example: should you invest in manufacturers of electric vehicles? Are they actually the future or are you headed for financial complications with this approach? Well you should read my article: why piston engines can outcompete EVS if you had a knowledge Renaissance.

Suppose you want to assess investing in Jeff Bezos' or Elon Musk's space technology? Well you should read my article: the Magnificent E-rocket.

Suppose you're thinking of investing in quantum computing as the big new thing that's going to be a massive disruptor? Well you certainly should read some of my articles in particular: unmasking quantum mechanics: when did magic become science.

What if you're thinking of investing in the Trump families company that's planning on going public to build a fusion reactor? Well you definitely should read by article titled: who says the sun is not a fusion furnace? Dinosaurs that's who! There I explain that it's impossible to get energy fusing atoms where some leftover mass magically turns into energy.

Or suppose you would like to take advantage of this spectacular knowledge Renaissance and make a fortune? Try reading: I sent this letter to TVs shark Superstar Barbara Corcoran under the subject title: we desperately need your social media skills to save civilization.

If you don't want to become the richest person on earth taking over piston engine production, maybe you'd like to just be incredibly rich helping me get these ideas out? Try reading my article titled: why do we accept such ridiculous ideas as science? Then you can make wise business decisions!