Deep | Inside Athene: An Exposé on Apollo's Growth Engine

Preface

Apollo Global shares hit -46% peak to trough a few weeks ago and despite the recent bounce remain 34% off ATHs. Depending on who you speak with this is either the beginning of the end or an opportunity to jump in alongside some of the savvier private capital operators of our generation.

What we can say for sure is that BDC redemption headlines on ADS alone are a red herring when it comes to evaluating Apollo:

I have spent over 100 hours digging into Athene – forming my own view from the bottom up, parsing data from its >9,000 page statutory filings all the way down to CUSIP level credit analysis, reverse engineering its largest exposures and forming my own assessment away from NAIC designations.

Recent debates on Private Credit have predominantly centred around a relatively small segment of the overall market: non-IG, semi-liquid vehicles.

The life insurance industry is clearly far more consequential with >$5T of capital in fixed income and policyholders who depend critically on annuity streams for retirement – perhaps bearing risk they did not elect to assume – unlike HNW retail choosing to participate directly illiquid in Private Credit vehicles (caveat emptor, anyone?).

Doomers will point to BDCs as the canary in the coal mine – source of negative reflexivity threatening broader systemic contagion fuelled by all of the above.

Others temper that rhetoric – not all credit is created equal. Forced sale triggers are lacking beyond the world of levered BDCs.

Executives at Apollo themselves seem to oscillate between defence of the broader Private Credit industry and what comes across as gleeful contempt at competitors’ missteps. Perhaps a tell-tale sign that they are positioned to win either way?

As an opportunistic investor that thrives on complexity, this is exactly the type of divisive situation that gets my juices flowing.

Why has the captive insurance model been so successful for Apollo? Is it really at risk of unravelling? Are they more likely to be a victim or a beneficiary of dislocation and widening spreads? Let’s dive in.

The Athene Era

Financial firms rarely pioneer new business models once, let alone twice. Apollo wrote the playbook on distressed capital structures in the early 90s and in the past decade redefined the scope of private capital through Athene.

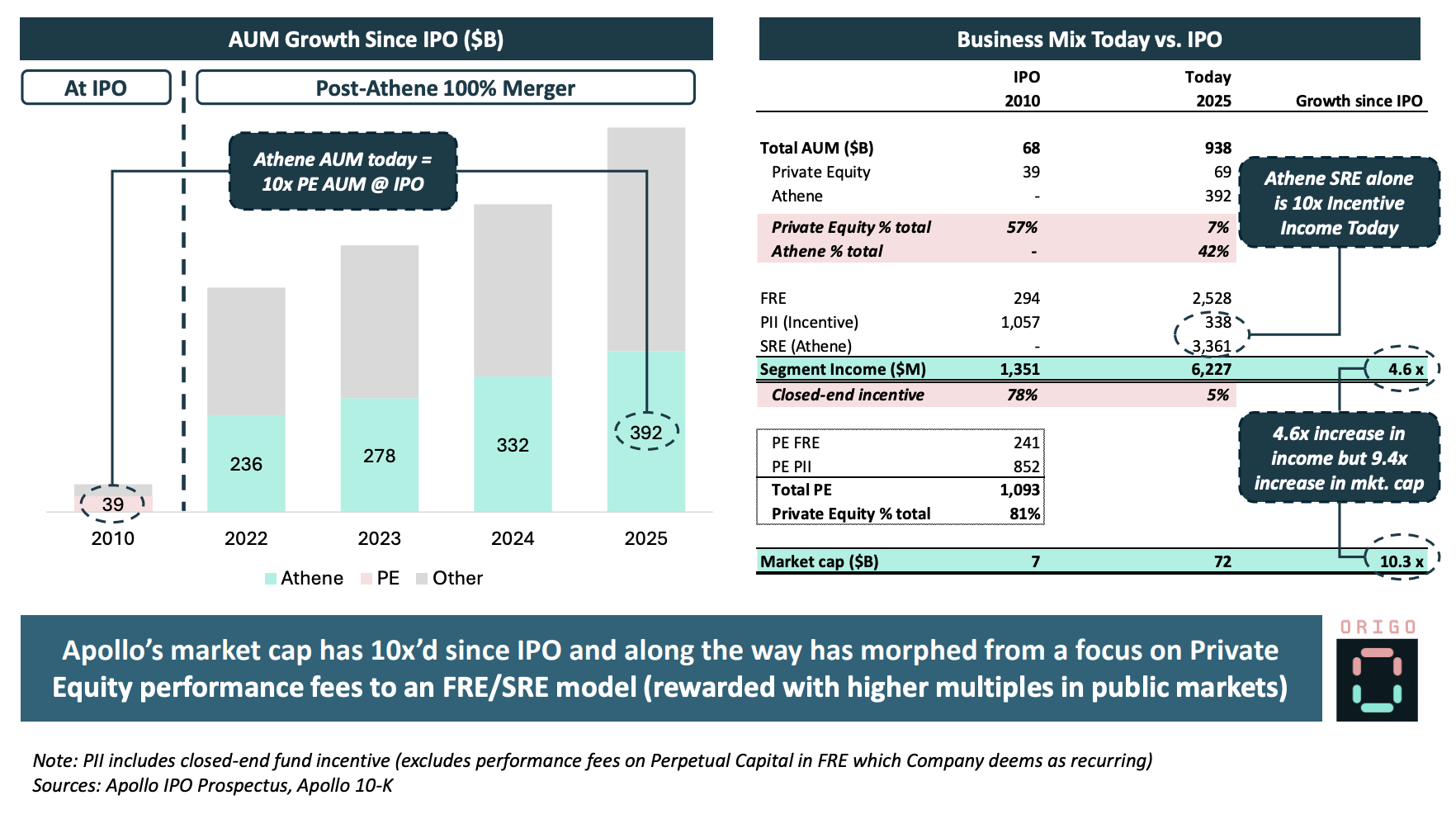

At $392B in AUM, what started out as Marc Rowan’s side-project now accounts for ten times Apollo’s Private Equity AUM at IPO.

The original Apollo model took advantage of capital cycles to generate eye-watering performance fees in a private partnership model – in 2010, over 78% of Apollo’s total income was carry-related. Today this number is less than 5%.

Public markets reward predictability. While Athene has been instrumental in driving 5x earnings growth, the enhanced mix and resulting multiple expansion have propelled Apollo’s 10x increase in market cap since IPO.

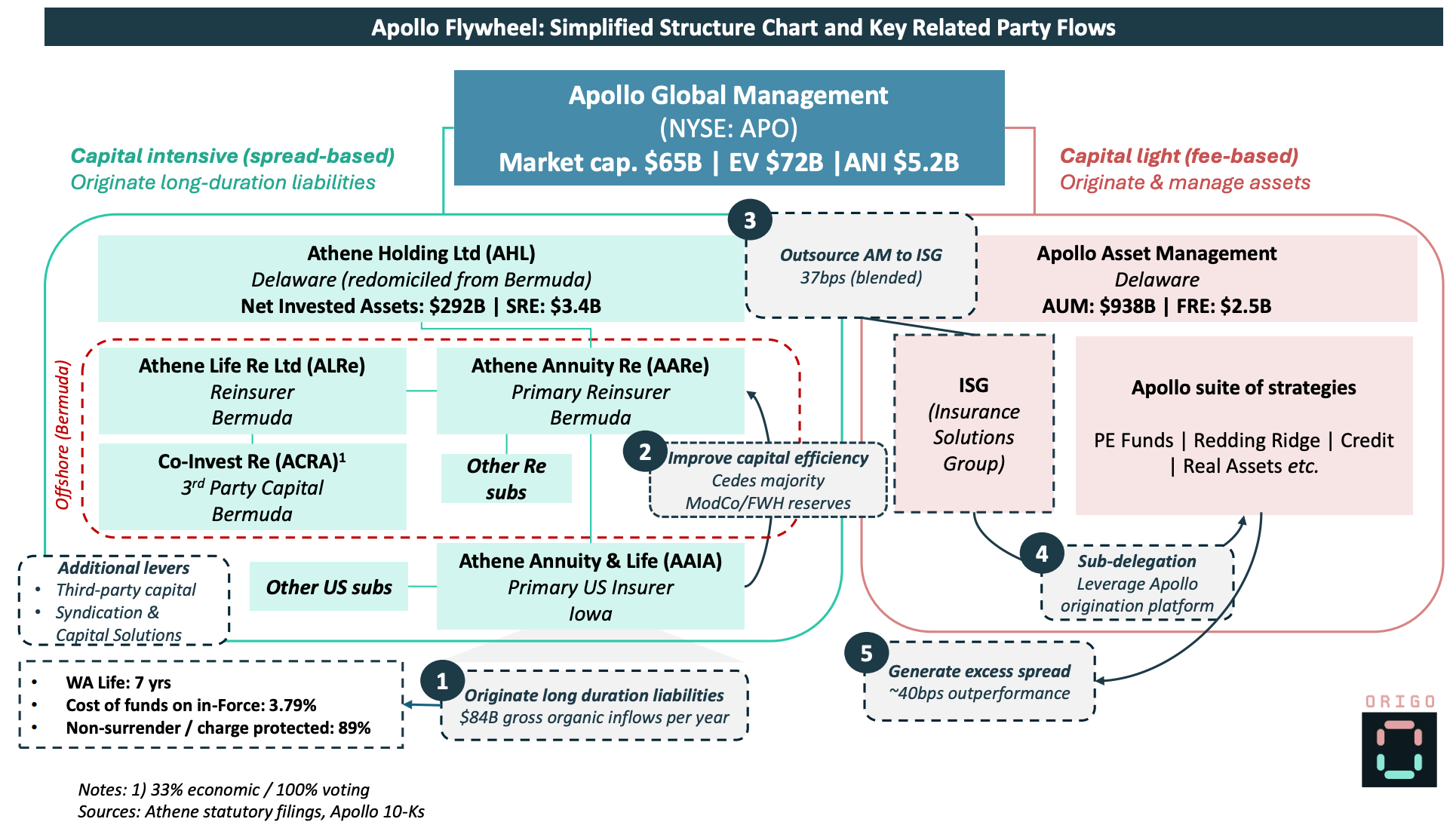

The Apollo & Athene Flywheel

Athene and Apollo operate as two well-oiled machines complementing each other. One, Athene, is a (somewhat) capital intensive business with a model that is reliant on generating excess returns on its spread-based liabilities. The other, Apollo Asset Management, is purely asset light and generates recurring fees based on its ability to originate product at excess returns.

The basic mechanics are as follows:

Athene originates long-duration liabilities, primarily by selling annuities via its US facing entity Athene Annuity & Life (AAIA).

AAIA in turn cedes reserves via ModCo/FWH to AARe in Bermuda for improved overall capital treatment. Along the way Athene will also leverage third-party capital through Bermuda sidecars (ACRA) which magnifies volume and ROE (additional fees).

Athene is then party to an investment management arrangement with ISG (Insurance Solutions Group) which sits under Apollo Asset Management. Under this agreement Athene pays Apollo a base fee + a premium depending on the type of asset originated. Under the latest restated agreement this has amounted to ~37bps blended.

ISG sub-delegates as necessary to other Apollo strategies whose mission is to originate excess spread on Athene’s spread-based liabilities + capital and turbocharge Athene’s investment returns (SRE).

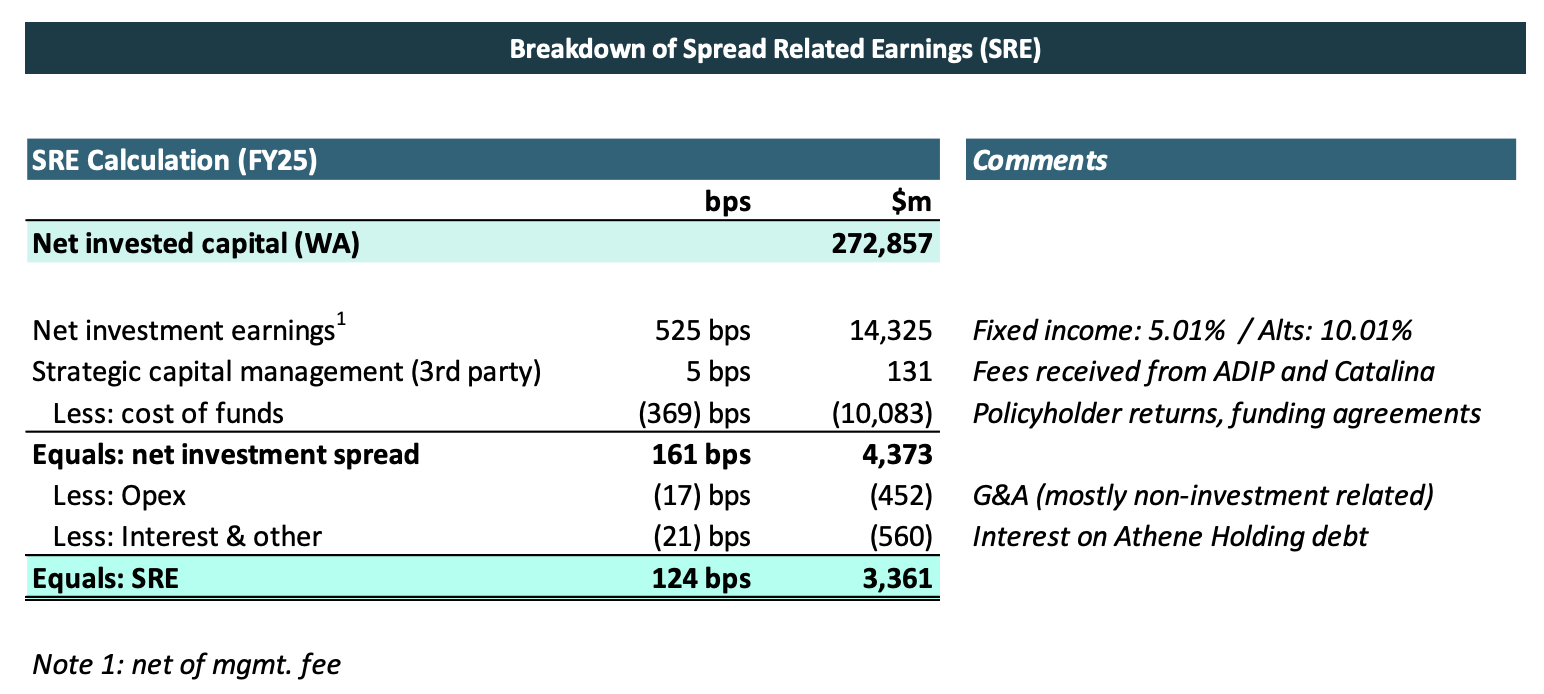

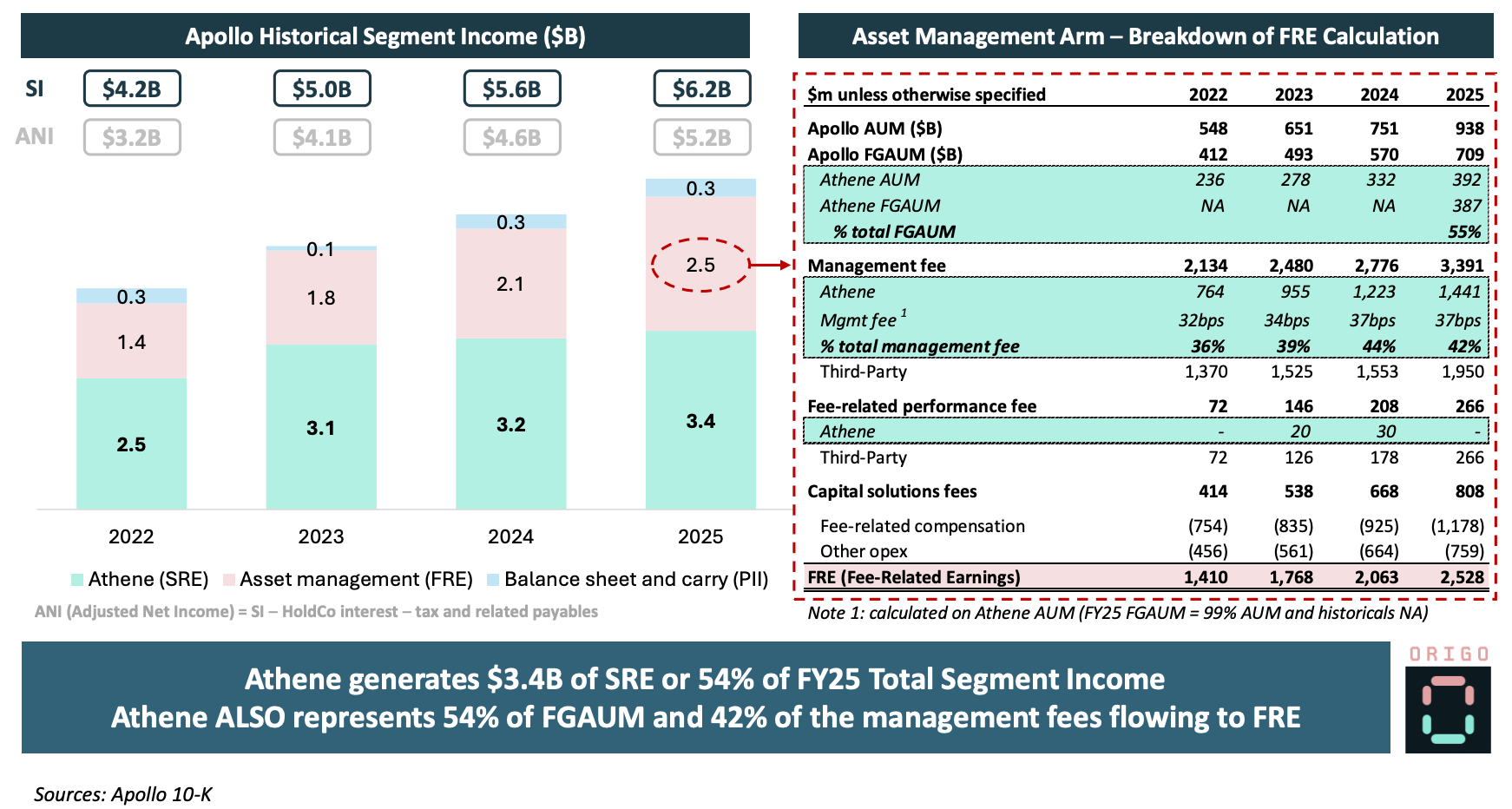

Spread Related Earnings (SRE): small bps, large numbers

Much like a bank, Athene is in the business of earning a spread on customer assets. Unlike a bank who borrows short to lend long, Athene seeks to borrow long to lend long – its liabilities have a ~7Y WA life at a cost of funds-in force of 379bps. In both cases, the name of the game is volume.

Throughout FY25 Athene earned a net investment spread of 161 bps on $273B of average net invested assets (ex-minorities). This spread is the delta between its net investment earnings of 525 bps and its cost of funds (policyholder returns) of 369bps. In addition Athene earns fees through the ADIP Funds on sidecar vehicles that participate in volume origination (5bps).

In total, Athene generated $3.4B in SRE (54% of total segment income):

Not just a spread game: Fee Related Earnings (FRE) on captive AUM

SRE alone vastly understates Athene’s importance to Apollo’s overall valuation. As we have seen, Apollo’s Asset Management arm ALSO earns a fee on the AUM managed on its behalf (a fee which is already netted off the 525bps of net investment earnings).

Athene paid $1.4B in FY25 or 42% of the management fee flowing into FRE.

The captive AUM component is critical to Apollo’s valuation since FRE is perceived to be the highest quality cashflow stream of the business.

FRE is asset-light, scalable and sticky. As a result this segment earns the highest multiple in the public markets (historically 25-30x).

Apollo’s SRE in turn is valued on the strength of its ROE and earns a premium multiple vs. peers assuming it can originate at attractive spreads in a capital efficient manner.

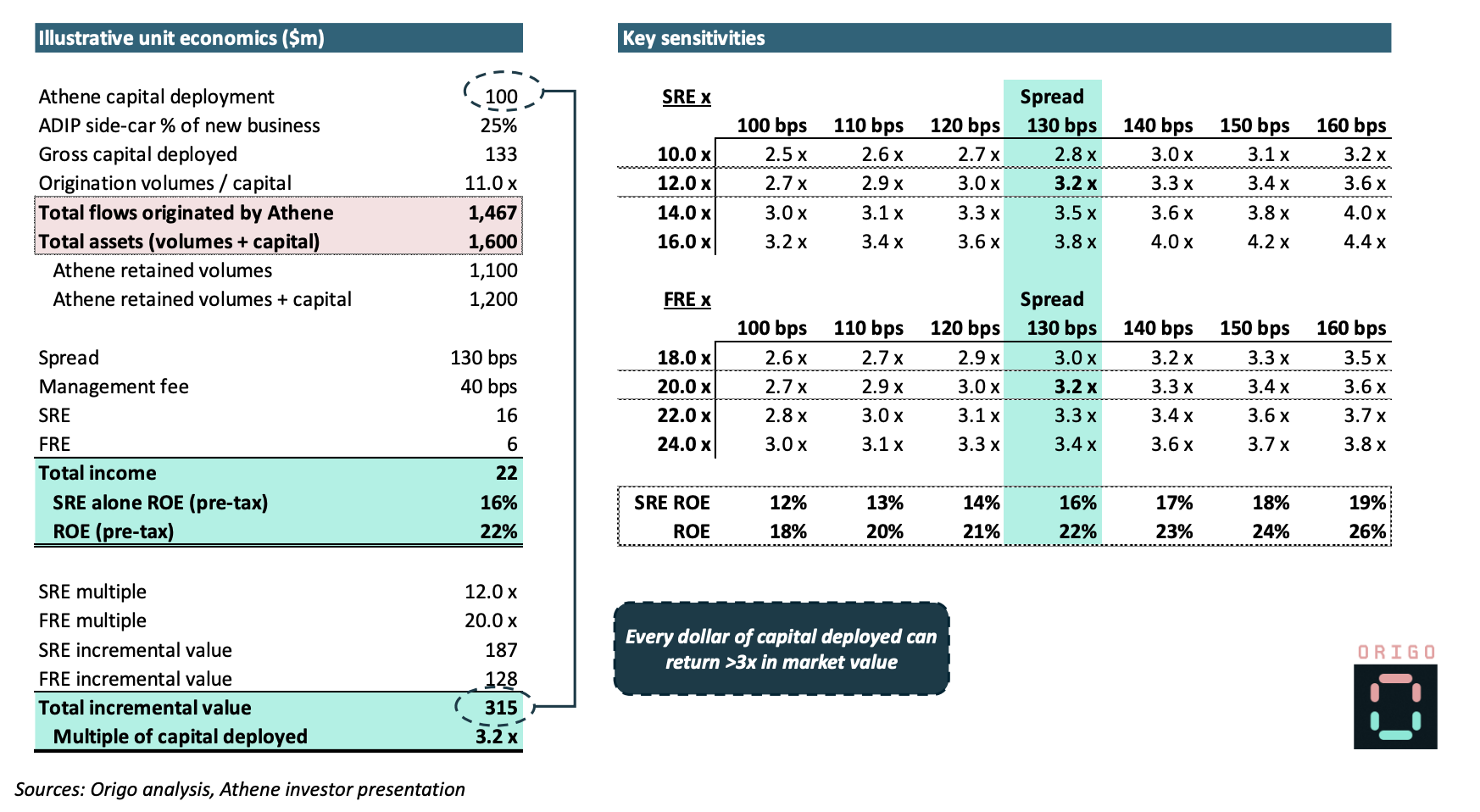

Unit economics: compounding machine

Putting this all together, it’s easy to see how attractive the captive insurance model can be from a unit economic perspective if all cylinders are firing in harmony.

I estimate every $ deployed through Athene to return >3x in market value on relatively undemanding assumptions. While this table should make clear the key variables at play, it also highlights how Apollo executives can drive value without having to shoot the light outs on investment outperformance.

The captive insurance model for asset managers has been so attractive with each dollar of capital deployed having positive cascading effects and nowhere has this been more evident than with Athene / Apollo.

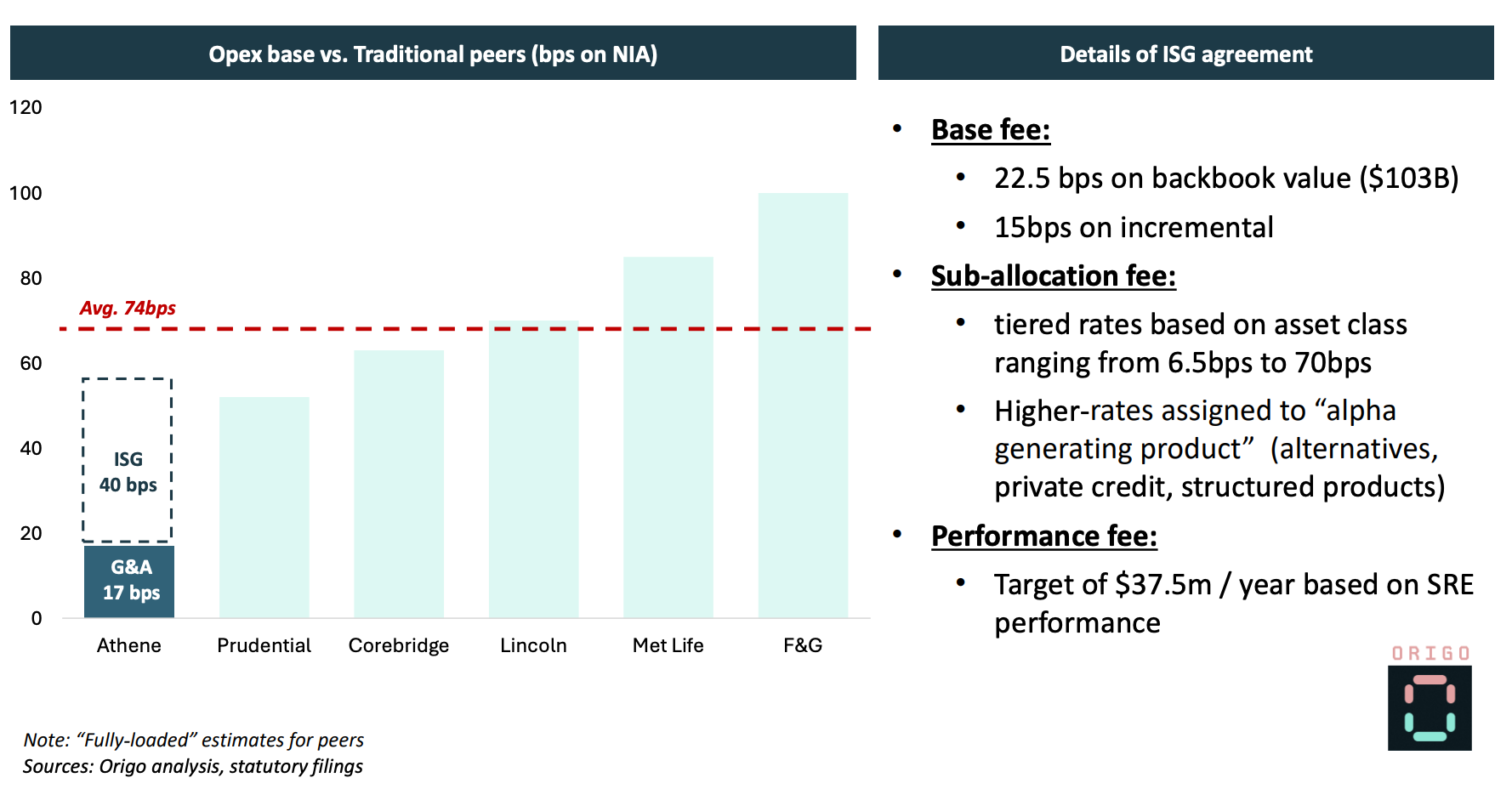

Related party shenanigans? a word on Opex

A natural question to ask would be whether Apollo has an incentive to overcharge Athene for its services in order inflate FRE (given the potential arb in terms of valuation multiple).

Athene’s outsource model allows it to run very lean operations with G&A representing ~17bps of Net Invested Assets (NIA). Traditional insurers which run internal investment teams typically operate closer to ~74bps.

On a “fully loaded” basis the 35-40bps Athene pays to ISG appears to be (i) arms length and (ii) source of competitive cost advantage.

This is also before taking into consideration the incremental alpha its cost structure is supposed to generate vs. peers.

Importantly when comparing to traditional insurers, Apollo’s asset management unit is already self-sufficient and highly profitable on a standalone basis through its management of third party capital. In a game of small bps on large numbers, these opex considerations are crucial.

It is worth highlighting that Apollo’s disclosures on the topic are the most transparent out of all the captive insurers. KKR’s arrangement with Global Atlantic is more opaque and it gets even murkier with other players further down the totem pole.