Deep | Honeywell: Catalysts Galore and an Option on Quantum

A spin-off and an IPO in a set-up reminiscent of GE

Honey, well I bought the dip

After patiently waiting around, we are excited to finally initiate a position in Honeywell (HON), taking advantage of the recent pull-back (-15% off the highs) on temporary Aero supply-chain related volume concerns, which we view as immaterial to the longer term thesis.

While we are keeping some powder dry for lower, we were keen to acquire a toehold ahead of a now compressed timeline with imminent catalysts ahead.

Wait, you’re excited to buy refrigerators?

Not quite. Honeywell has a storied history, from early thermostat innovations in the late 1800s to a critical role in the Space race, supplying controllers for America’s first satellite Explorer 1 and over 16,000 parts for Apollo 11. Like many large industrial companies of its era, HON’s footprint morphed through organic initiatives and M&A into a sprawling conglomerate.

The Company embarked on an initial transformation in 2017, spinning-off its residential & consumer operations and shifting its focus towards “software-industrial” B2B.

This accelerated under the new CEO Vimal Kapur who in 2023 sought to further realign Honeywell across three megatrends: automation, the future of aviation, and energy transition.

Following a portfolio review in 2024 the Board agreed to embark on a series of spin-offs and we are now in the final phases of this transformation.

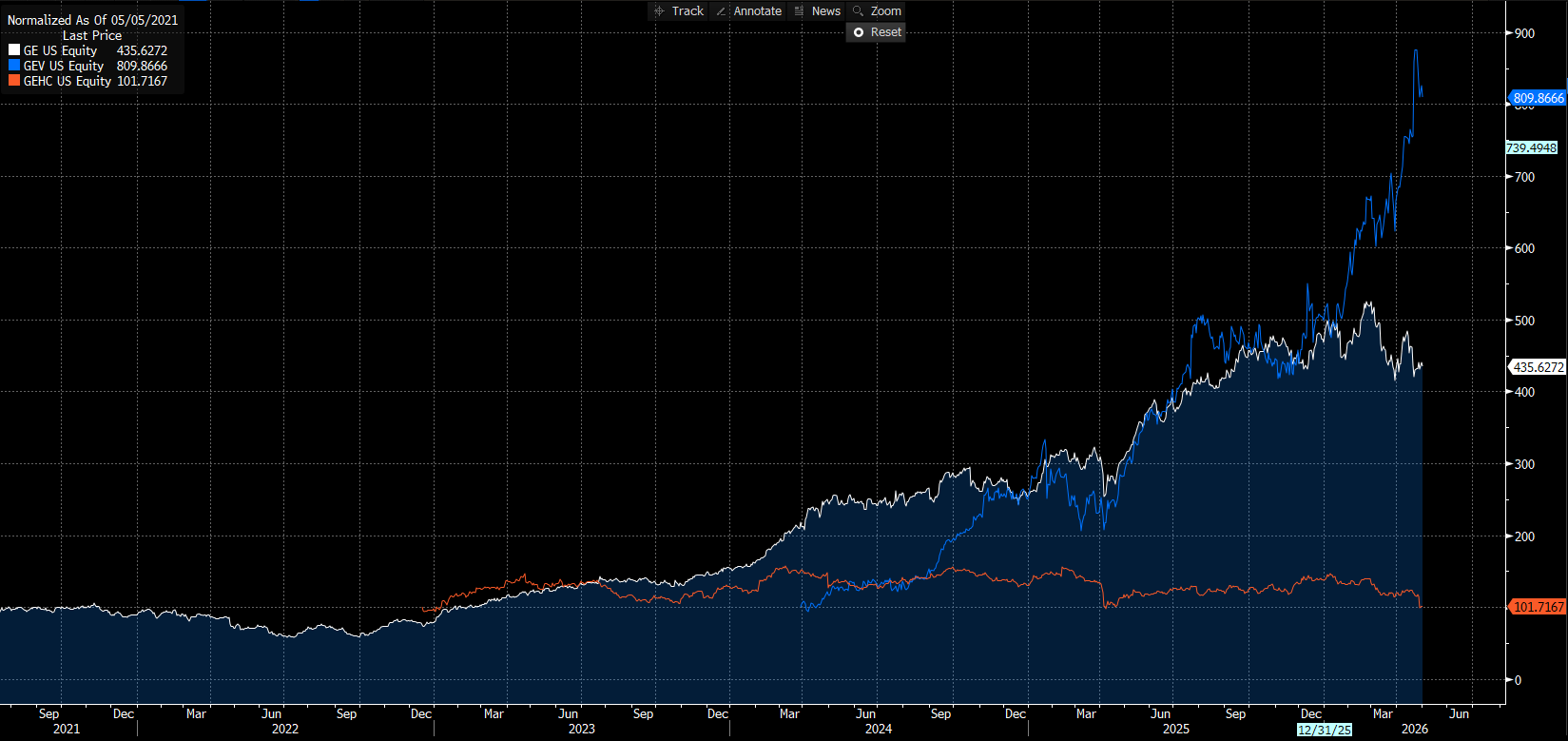

The GE blueprint

The set-up is reminiscent of General Electric when they decided to split the business in three in late 2022 – after stagnating sideways for years the strategy unlocked the following share price performance:

Spin-off: GE Vernova: +909%

Spin-off: GEHC: flat

StubCo: GE (Aerospace): +535%

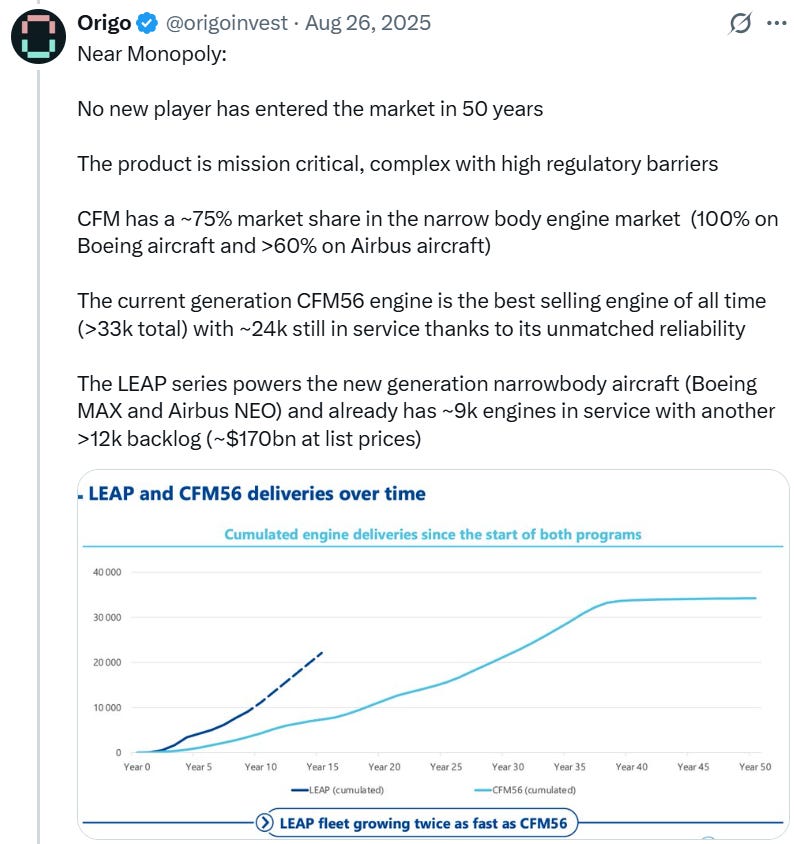

GE Aerospace is an incredible business and also Chris Hohn’s (TCI) top holding, helping him drive the biggest annual gain ever recorded by a hedge fund last year (+$28B). The crown jewel of GE is CFM, its JV with Safran which dominates the engine market for narrowbody commercial aircrafts: large installed base with highly visible (>30 year) cashflow profile through new equipment and after market services.

Prior to the spin-off, Chris Hohn was already very familiar with the business through his investment in Safran (the other side of the CFM JV) which he had held for >13 years. Safran shares have compounded at 20% IRR for him over that time frame (!) In other words, the type of business you are more than happy holding for the long-term even at a fair price.

So what about Honeywell?

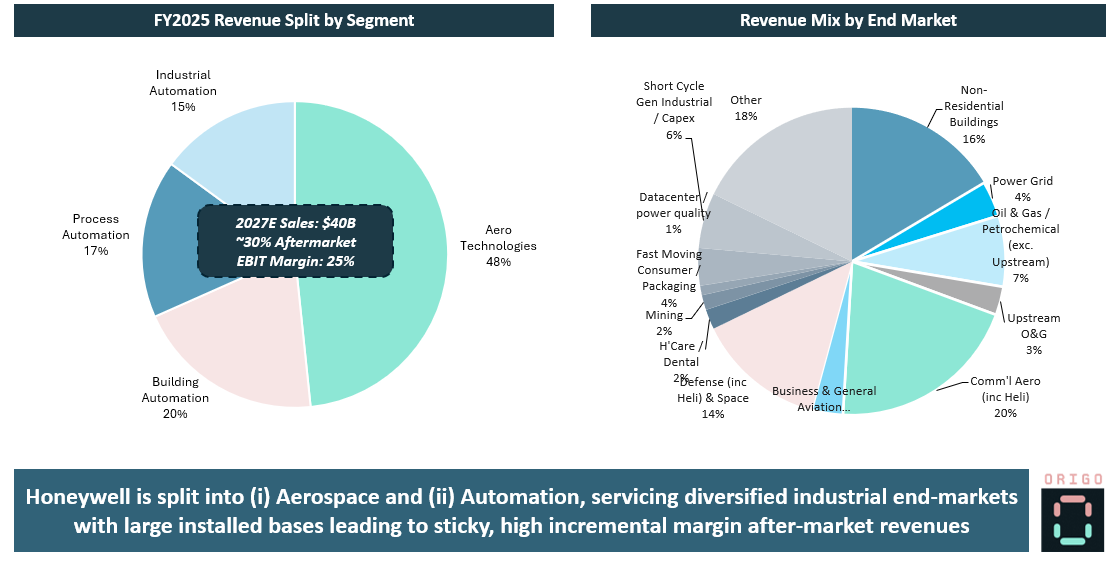

HON has recently reorganised its reporting lines across (i) Aero Technologies and (ii) Automation which together generate close to $40B in sales across diverse industrial end-markets. This is post spinning-off its Advanced Materials division (SOLS) at the end of last year (SOLS is +60% already).

The Aero Technologies business, on the aircraft side, specialises in avionics and auxiliary power units (APUs) amongst others. While not 100% comparable to engines, HON’s market position in APUs is very similar, with an effective monopoly on legacy and current generation commercial narrowbody platforms.

In addition, HON is entrenched in Defence where it equips 70% of military aircraft worldwide and in the Satellite market where its hardware flies on ~80% of satellites currently in orbit.

Automation comprises (i) Building (safety & sustainability solutions for fire prevention, energy management etc.) (ii) Industrial (sensors, logistics automation etc.) and (iii) Process (emissions reduction, cybersecurity etc.).

Overall, Honeywell benefits from large installed bases and a growing aftermarket sales component (currently ~30%) with high incremental margins.

Catalysts, timeline, and the cherry on top

HON is in the final stages of its transformation and looking to execute on two important milestones in very the near-term:

Spin-off of Aerospace division June 29th

Divesting non-core (lower margin) assets PPS and WWS (H2 closing)

This is not all, however.

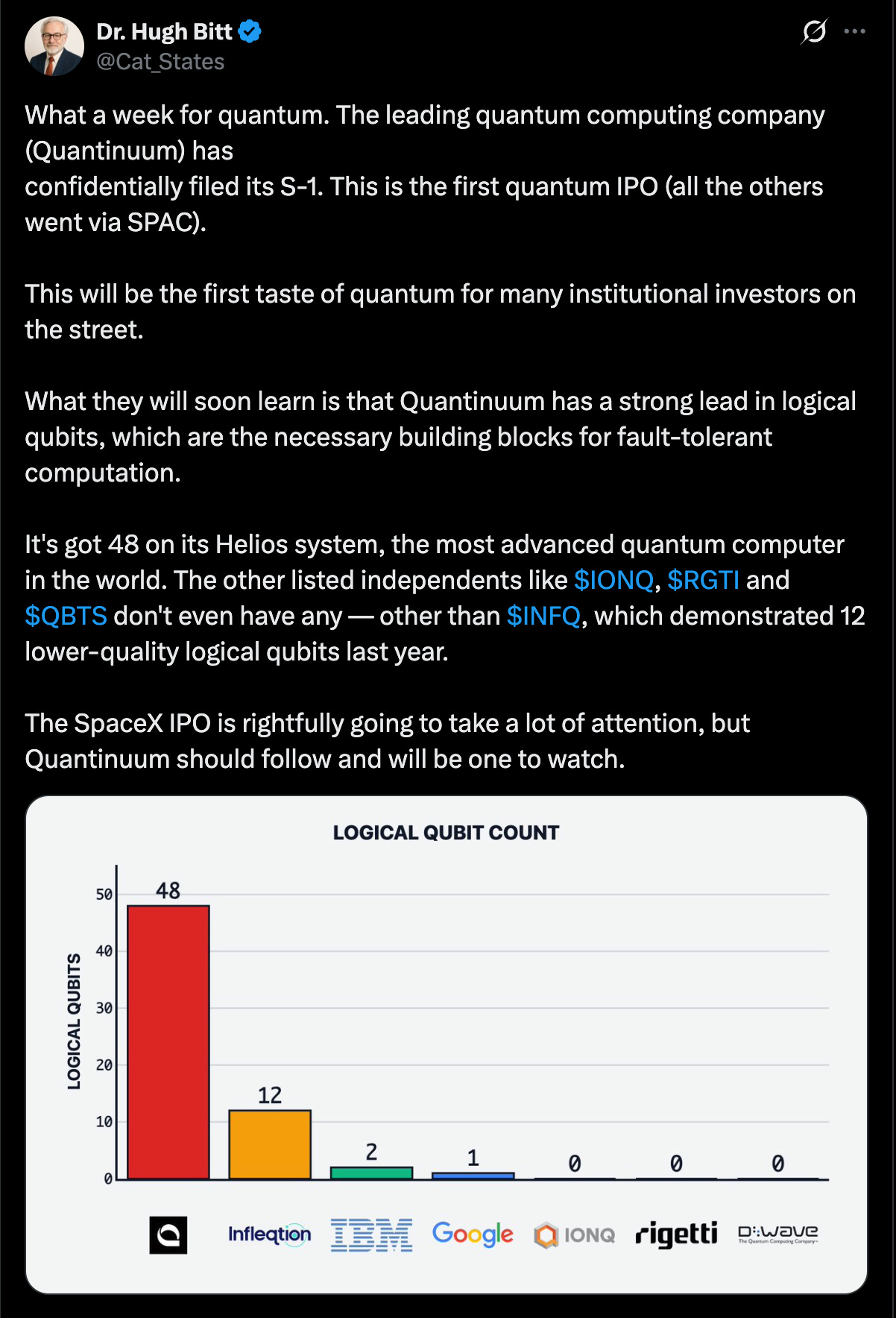

Honeywell is the majority owner (54%) of Quantinuum, widely perceived to the THE leader in quantum computing. Back in 2021, HON combined Honeywell Quantum Computing (trapped-ion hardware pioneer) with Cambridge Quantum Computing (quantum software). In September 2025 it raised capital at a $10B pre-money valuation from the likes of NVIDIA and JP Morgan (who lead prior rounds). Quantinuum was the first hardware provider to integrate NVIDIA’s CUDA-Q platform and in November 2025 they launched Helios, the first commercial quantum computer, leaps ahead of its competition (yes even IONQ despite recent progress).

Quantinuum confidentially filed its S-1 in February and is slated for an IPO later this year.

We love free options that can go “ballistic” and Quantinuum represents an exciting “swing factor” to an already attractive set-up.

The rest of the post is for paid subscribers. Now that we’ve provided the background, let’s dig into valuation, target levels and our overall thought process on the trade.