Weekly | State of the IPO Market, Tactical Considerations, $HONA Spin-Off Incentives

After a monster +32% run in the span of 60 days, the NASDAQ dipped -4.8% on Friday accompanied by a surging VIX which was +40% on the day.

As we touched upon last week, markets have been in a hybrid state of euphoria and paranoia – dancing with one foot towards the exit, as evidenced by SoftBank’s equity and CDS simultaneously reaching ATHs.

Friday’s move was symptomatic of this. While the tendency will be to look for underlying triggers (jobs report, UST yields, Broadcom), the reality is that the market was reaching a point of local exhaustion and looking for any excuse to trade lower as it hunts out pockets of increasing leverage and exuberance. A healthy and perhaps overdue sell-off.

State of the IPO market

The competition for attention and capital has been intensifying. Hold periods have been trending lower with participants keen to front-run narratives and “new shiny toy” syndrome dominating the timeline.

This obviously manifests itself most clearly through new IPOs, but only for select companies. The current reality is that the IPO market is incredibly bifurcated and late-stage / top-heavy. Many processes have been downsized, postponed or withdrawn as the list of sectors perceived to be prone to AI disruption grows. Just ask anyone in Private Equity how their DPI is going!

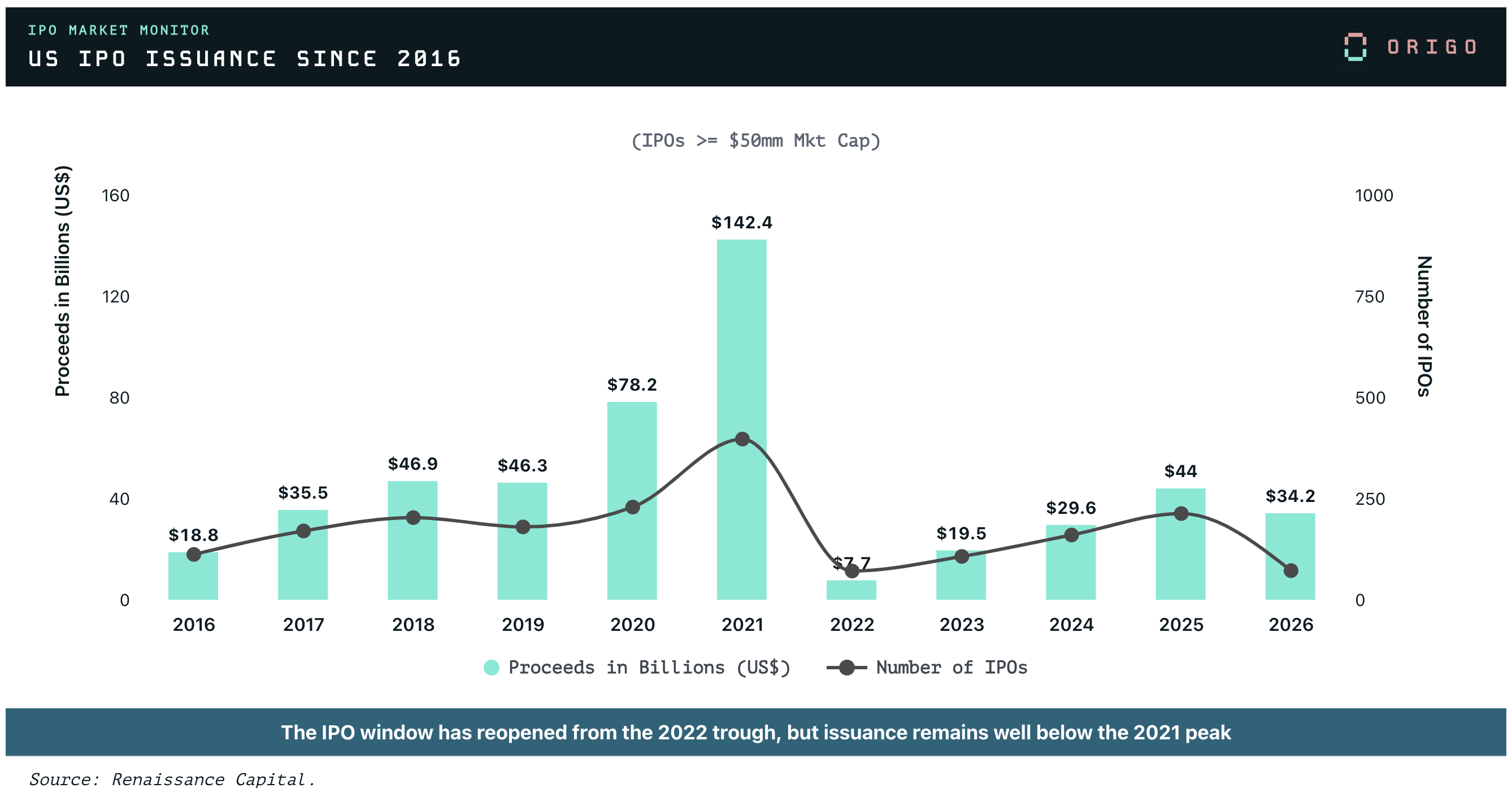

Overall, $34B has been raised to date across a limited amount of deals. We are FAR from the craziness of 2021 (which feels odd to say given shared similarities with that time period).

The Meta is evolving

When it comes to the select “hot” IPOs, there seems to have been a shift in Meta over the past week. Hyperliquid originally influenced the game, creating a shadow-book for opening trades at listing. With Cerebras the pre-IPO market was spot on, anticipating a >80% uplift on the first trade.

This established a confirmed yardstick for upcoming IPOs, reinforcing a >40% delta between guidance and pre-IPO markets on Hyperliquid.

The actual performance of Cerebras since then (almost all the way back to the $185 offer), however, has now inflected this paradigm.

Quantinuum was a clear victim of this trend-shift this week as the “IPO pop” failed to materialise to the extent initially anticipated on Hyperliquid.

Naturally, this creates a cascading effect and SpaceX is currently trading at $172, a more modest implied uplift of +27.5% vs. the ~50% implied a week ago.

What does it mean to be oversubscribed?

Seeing a lot of commentary around SpaceX “only” being ~2x oversubscribed.

$SPCX book-build is obviously unique given the sheer quantum being raised and with the number of channels they are pursuing, it also makes sense to settle on a single, properly pre-sounded price target rather than play the usual iterative game on guidance & subscription amounts.

What is important is that the offering is already de-risked at that level. Whether this was done at 2/3/4x doesn’t “fundamentally” make a difference.

Is 10x better? Yes and no. In truth, subscription multiples are not a clear indication of how a stock will trade post-listing, only of how high the offer price can be/was pushed. We just saw this on CBRS 0.00%↑ of course (20x oversubscribed, initial pop and down back to offer) as well as KLAR 0.00%↑ .

What matters is the mix of holders. If there is a lot of fast-money in the books, they (i) tend to oversize orders in anticipation of reduced allocations and (ii) typically “flip” the stock immediately, taking advantage of the initial pop + greenshoe stabilisation mechanism and thus intensifying any sell pressure.

Tactical considerations

As always volatility should be embraced. Having been reasonably disciplined with our buy/sells so far this year, we have dry powder to put to work.