Deep | Grid Wars: License to Connect

Alpha at the heart of Europe's structural grid deficit

Introduction

Markets have felt manic lately. Even with the S&P 500 at all-time highs, paranoia still reigns as AI threatens to redraw terminal values across large swaths of the market.

SaaS giants of yesteryear have been demoted to melting-ice-cube status, obscure bottleneck stocks are mooning, and the hot ball of money is already sniffing out the next rotation play (did you listen, anon?).

AI is widening outcome distributions like never before.

Ergo, the value of long-term assets with multi-decade visibility is going up.

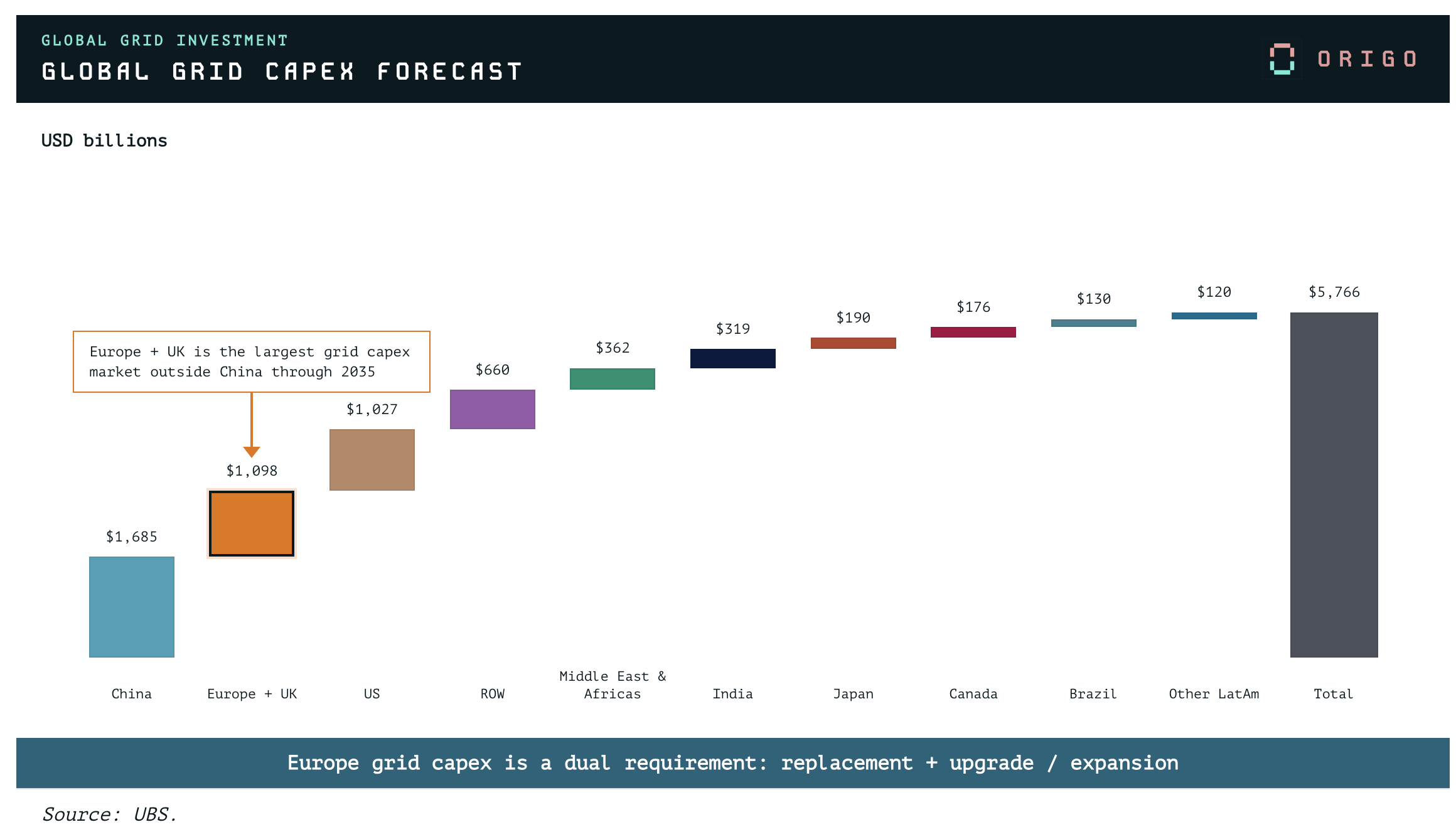

With this backdrop, we believe few set-ups are as inevitable as the $6T required to upgrade grid infrastructure in the coming decade.

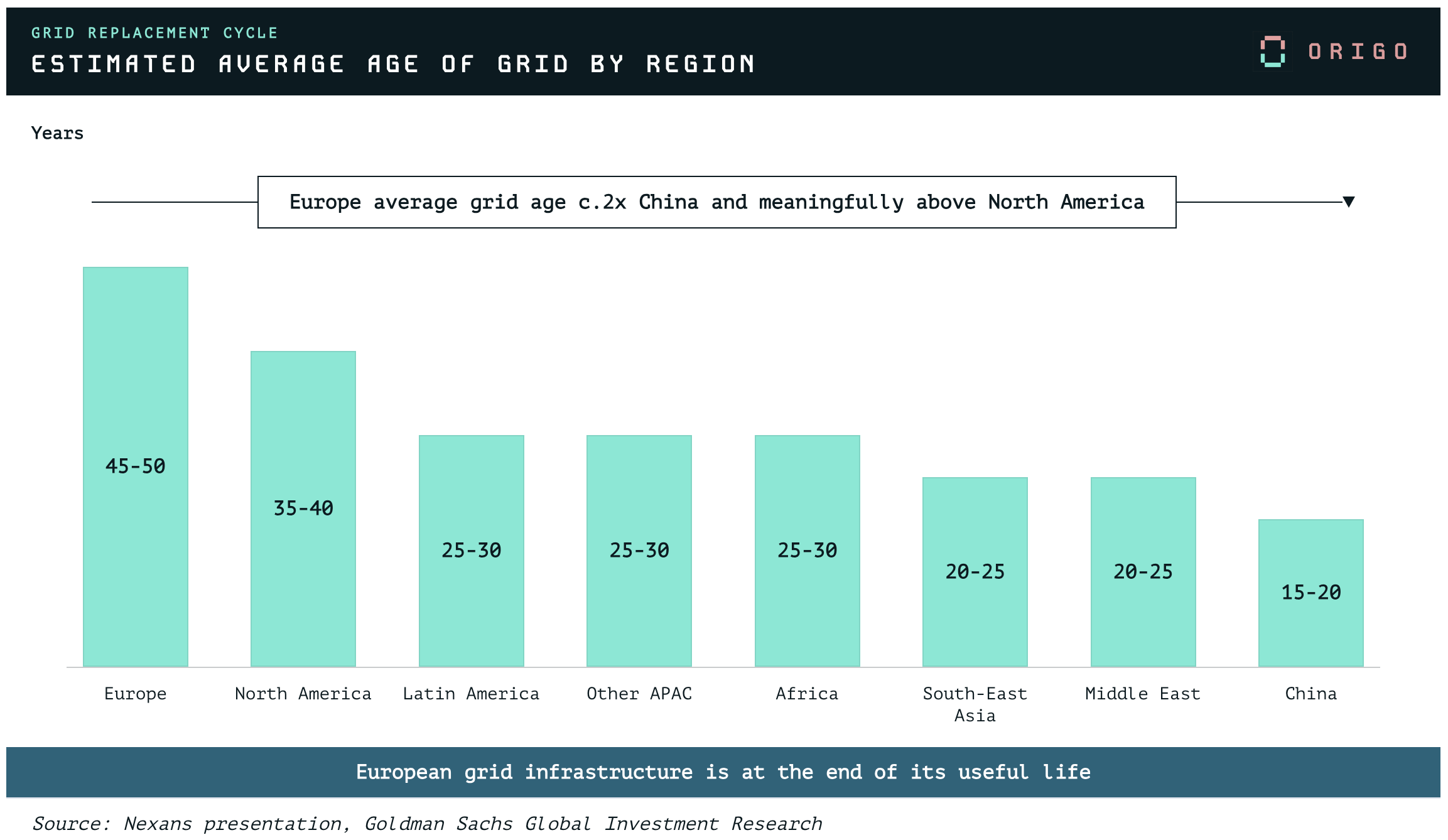

Europe is the most obvious manifestation of this: a grid reaching the end of its useful life, unable to cope with the energy transition let alone incremental load from 280 GW of datacenter connection requests.

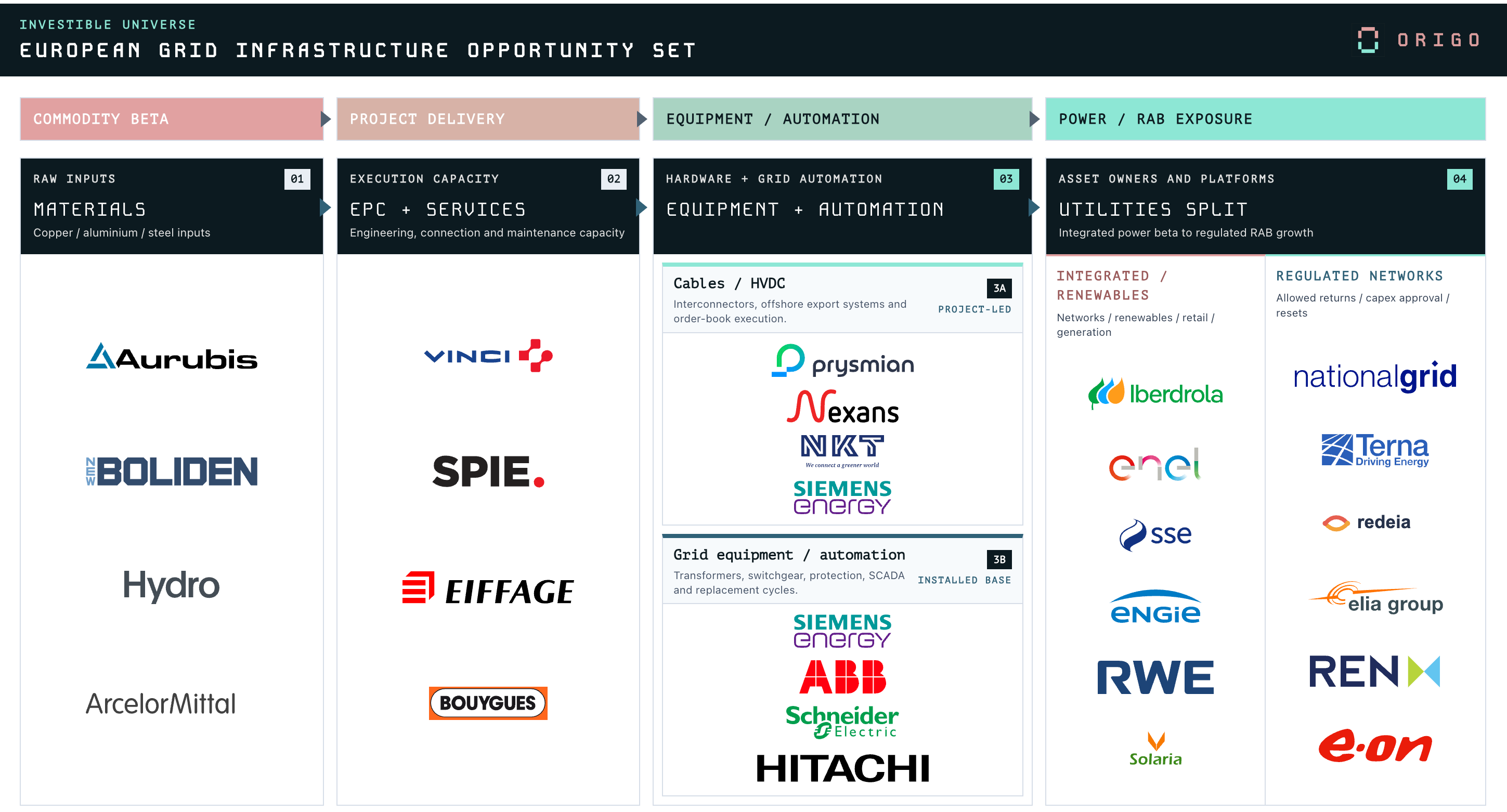

While there are obvious ways of playing this – regulated networks being one (which we expect to perform well) – readers know we are laser-focused on differentiated security selection and uncovering idiosyncratic convexity.

Our preferred expression is a <€4B mkt. cap owner operated platform that is capitalising on Europe’s structural grid deficit through a regulatory advantage built over two decades. We are in Y1 of a high-visibility, multi-year re-rate in which the sell-side will be playing catch-up.

Must-have, not nice-to-have

While ageing infrastructure is certainly a factor and a catalyst towards mandatory if not pro-active investment, the theme runs much deeper than that.

For Europe, the issue is particularly acute. After decades of incentivising renewables, the energy transition has been mired by stranded generation capacity with curtailment hitting record highs in 2025. In Germany, there were 576 hours of negative electricity prices last year, while Spain suffered through a blackout of unprecedented scale and duration.

Grid reliability over the next decades means managing electrification, distributed systems, and more volatile two-way flows. T&D, transformers, interconnectors, offshore cables, BESS, co-location, substations, automation and more will all need to be part of the solution as Europe plays catch-up.

This is all happening at a time when energy security is top of mind following multiple crises in the past 5 years alone – Covid, Russia, Strait of Hormuz.

While grid-related capex is a global necessity with $6T required through 2036, the scale and urgency of the situation is most pronounced in Europe.

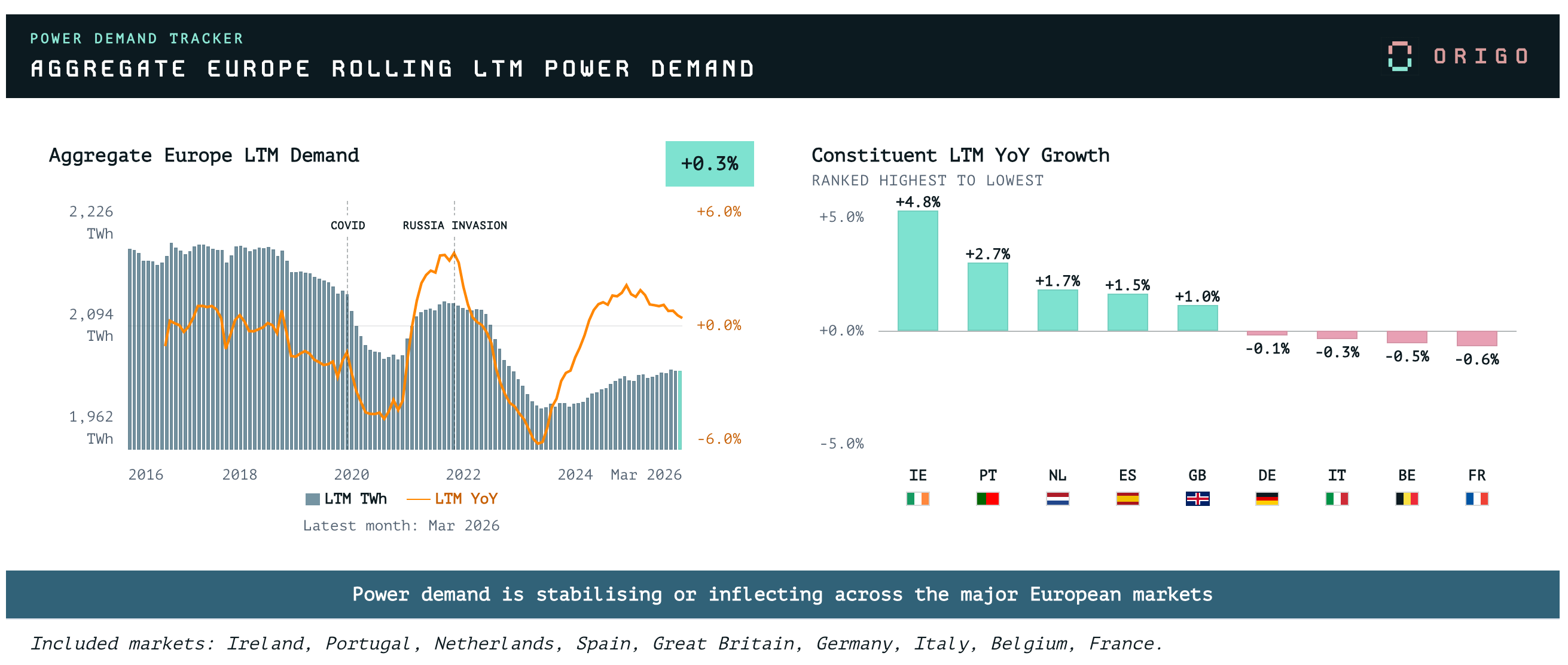

European power demand is inflecting

Renewables integration and supply-side volatility is being met with increasing peaks on the demand side as well.

After decades of declining power demand, Europe has reached an inflection point which is only set to accelerate with electrification and datacenters.

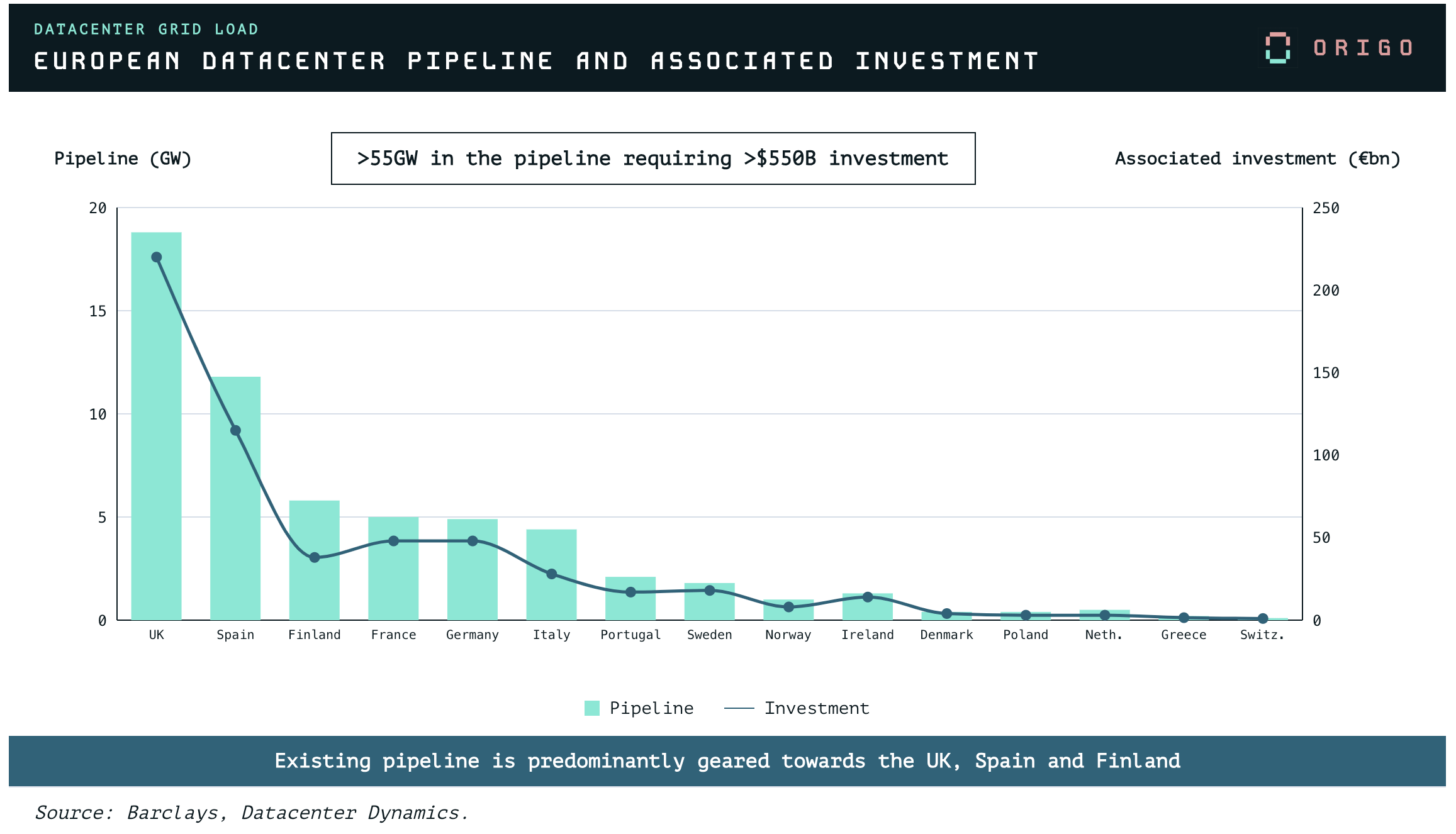

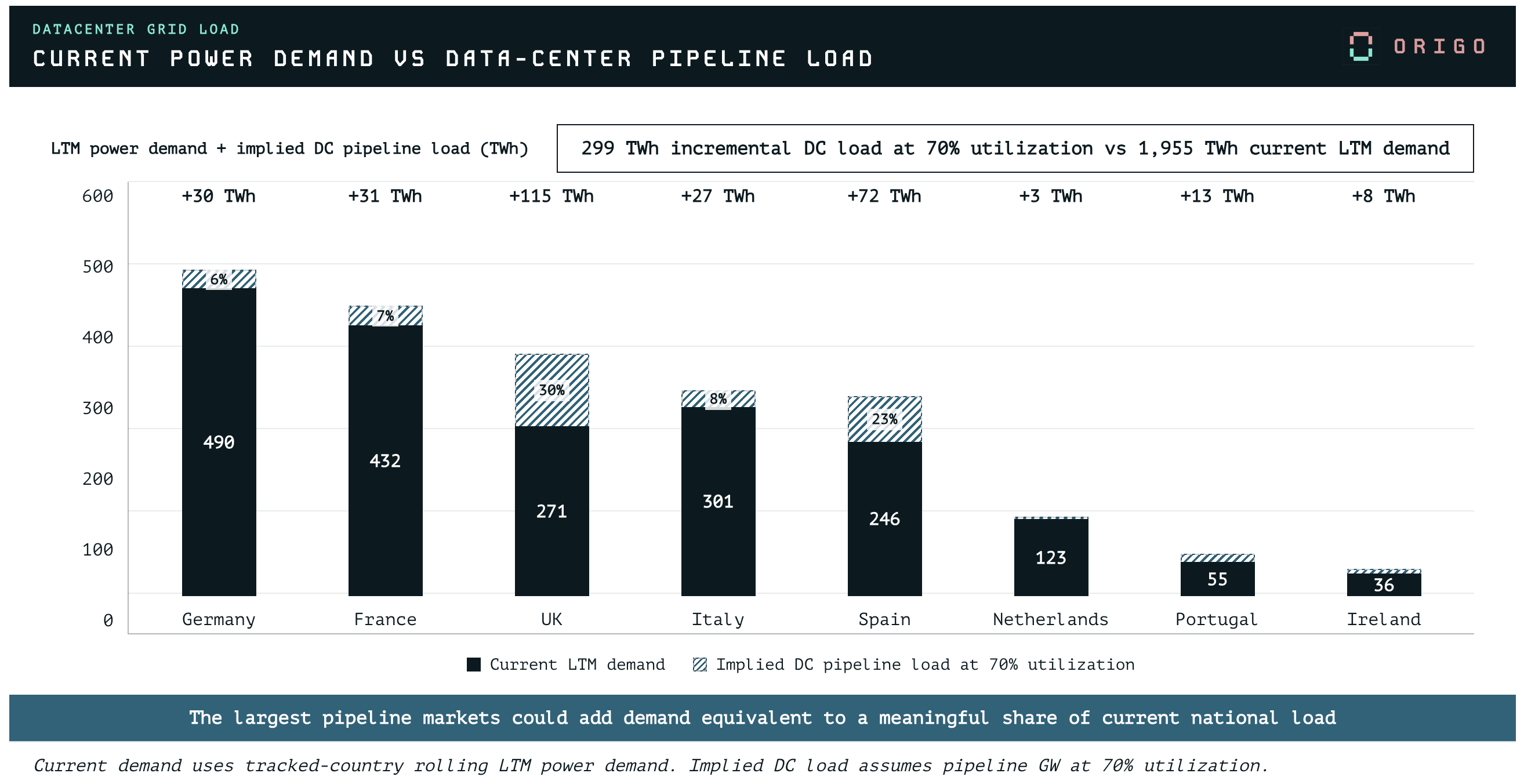

Incremental datacenter load alone is expected to represent a meaningful % of current power demand. According to numbers from Barclays / Datacenter Dynamics, there is >55 GW of committed datacenter pipeline in Europe:

Based on this, assuming a 70% utilisation rate, we calculate incremental datacenter load would translate into approximately 15% of existing demand for the core European markets – and north of 20% for Spain and the UK. For some of the more saturated markets such as Ireland, datacenter already represents >20% of overall consumption.

Of course, given the state of the grid, not all this capacity will be able to come online and there is an ongoing race as to who gets there first.

The Datacenter Grid Connection Wars

The demand is not the issue. The paradox of Europe has been its inability to harness lower power prices after decades of investment in renewables, which all comes back to grid infrastructure.

“the timeline for getting a grid connection had become one of the biggest deciding factors in the company’s data center investments. Connecting to the transmission network in Europe can take up to seven years, versus the roughly two years it can take to develop a data center.”

Pamela MacDougall, Amazon Web Services’ (AWS) head of energy markets and regulation in EMEA

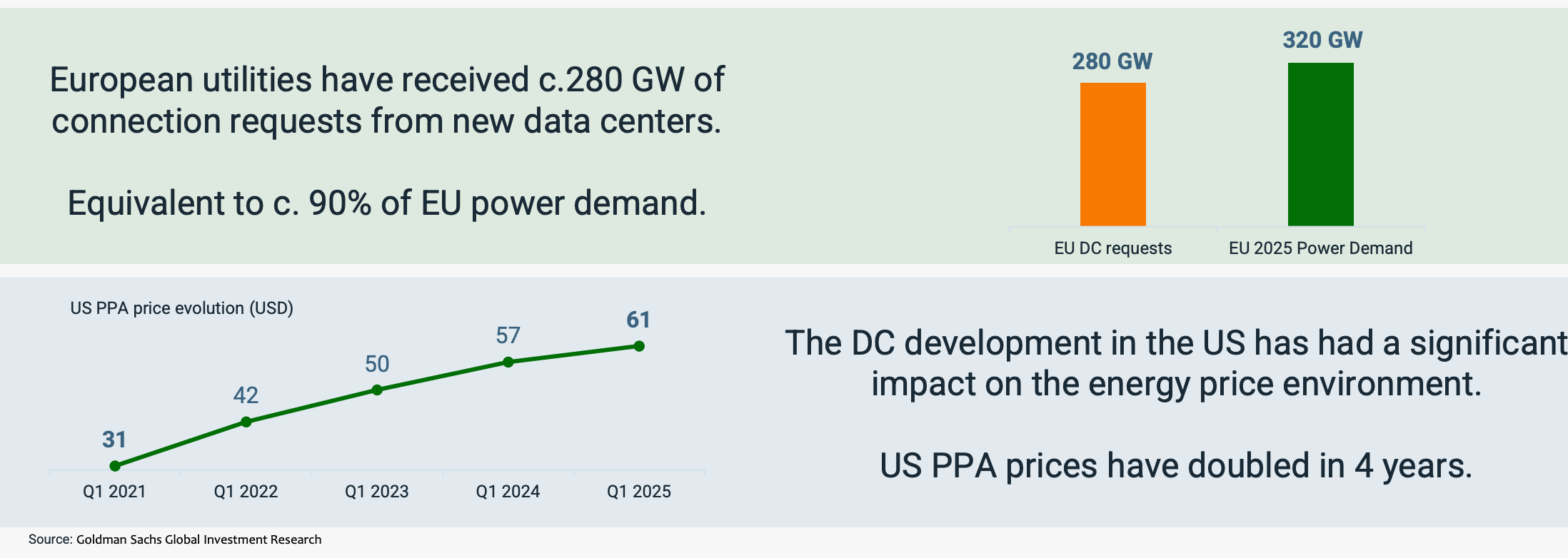

If we look at earlier stage pipeline, utilities in the EU have apparently received 280 GW in connection requests from new datacenters – equivalent to 90% of EU power demand! (granted, a large portion of this is likely testing/low-intention).

In the US, where market structure has allowed for a much more accelerated datacenter build-out (at least until recent permitting issues), we saw what happened to initially low prices as PPA $/MWh doubled in 4 years.

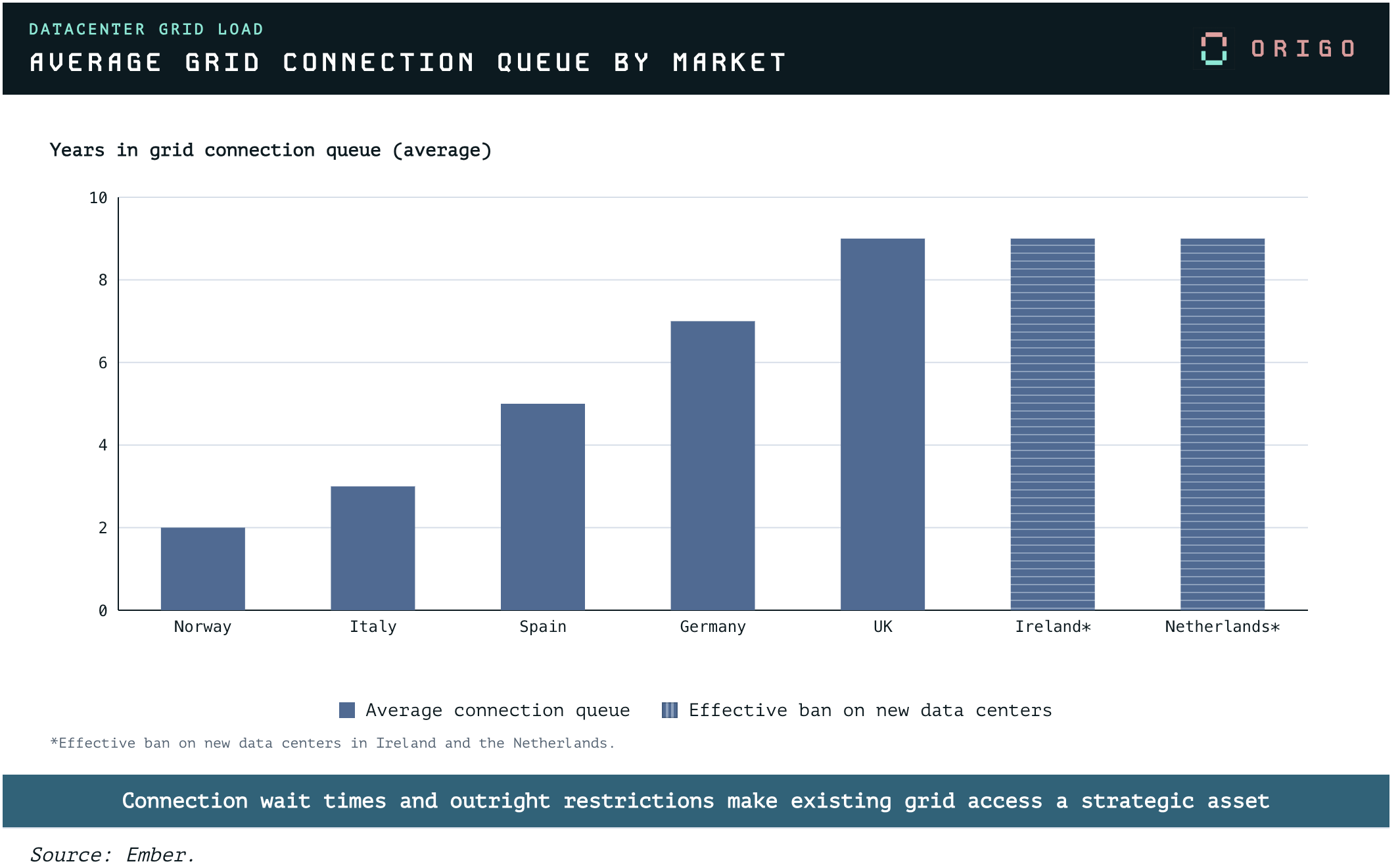

Not all markets in Europe are created equal. As we saw earlier, the first mover markets are now completely saturated to the point where Ireland has imposed a de facto moratorium on new datacenters in Dublin until 2028, while the Netherlands and Frankfurt have effectively banned new connections until at least 2030.

The ability to obtain accelerated access over the coming years has tremendous value and we would expect upward PPA price pressure as incremental load ramps-up. In the rest of this write-up we will discuss how we are playing this.