Weekly | Kimchi, Burgers and Planes

ADR Arb vs. Merger Arb

Free money?

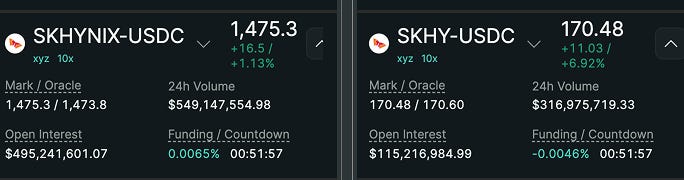

On Friday morning, Sk Hynix 000660.KS closed at KRW 2,180,000, or a USD equivalent price of $1,454.

Later that day, its long awaited ADR got listed. With King Leopold leading the charge, SKHY closed at $168, stretching to $172 in the after hours — or $1,721 on an apples-to-apples basis vs. its Korean cousin at the 10:1 ADR/local ratio.

With the Korean markets closed, the apparent trade — if you could execute it — would be to buy local & sell American for an implied AH spread of 18.4%.

24 / 7 Markets

The arbitragoors on Hyperliquid jumped at the opportunity to front run the suits ahead of the Korean market open. Early birds that went long SKHYNIX / short SKHY perps got rewarded: at the time of writing, the spread sits at 15.6% on Hyperliquid, implying a decent 280bps compression in less then 24h, even on a funding-adjusted basis. Is it just that easy?

ADR Arbitrage Mechanics

In a free conversion setting the idea is straightforward:

Buy cheap local shares in Seoul

Deliver them to the depositary bank

Get ADRs issued in the US (or reverse: cancel ADRs → get local)

The premium ultimately collapses to fees + FX + some lag linked to implied volatility.

Except in this case, we are dealing with constrained conversion rules including the following key restriction:

Depositary must get company prior consent for deposits of outstanding shares if total shares in ADS form would exceed the number initially deposited for the offering (the ~17.79M new shares / ~2.5% float), unless the company consents to more / files what’s required in Korea.

In other words, the gateway from Seoul to New York is closed (but you are more than welcome to cancel your American shares at a haircut).

This creates a structural premium for the ADRs, provided there is demand. With the ADRs >6x oversubscribed, suffice to say there is plenty!

The “issue” is further exacerbated by the limited ADR issuance as a % of float: only 2.5%. One of the reasons for this is due to rules we had previously highlighted around SK Square, the holding company: ownership cannot fall below 20% hence the dilution had to be managed.

So what is the “correct” spread?

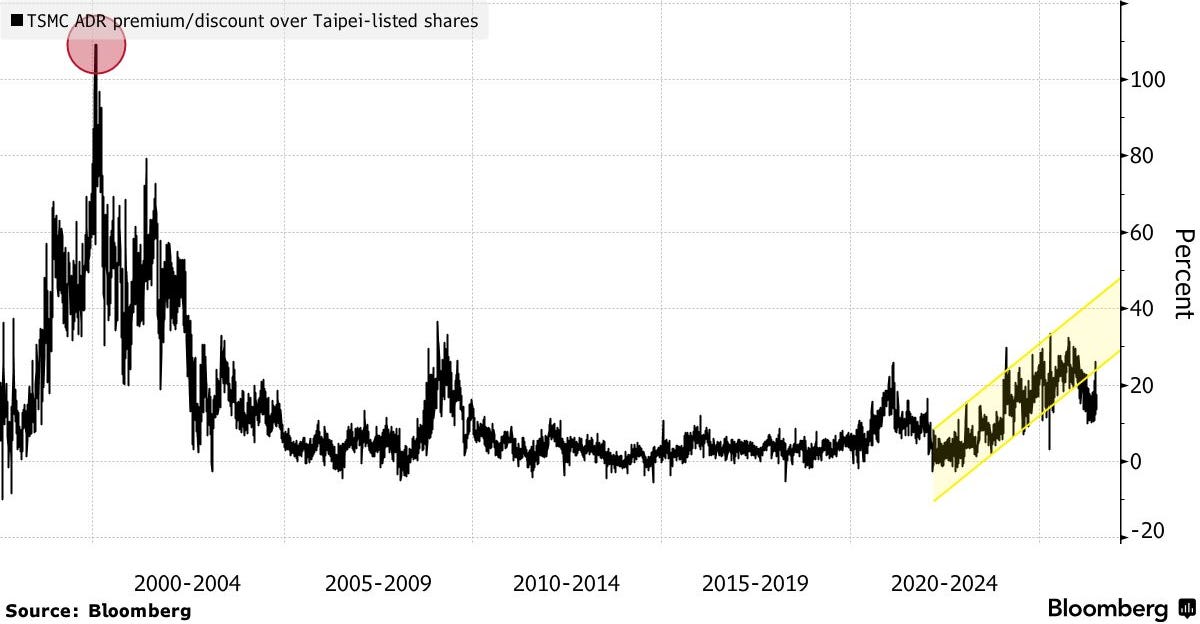

The TSMC benchmark

The only real “comp” in the market is TSMC, which has a multi-decade history we can refer to and largely reflects the same dynamics at hand:

Mega cap Asian semi with tight conversion rules (one-way)

Same buyer pool (global AI/semi capital preferring a USD wrapper)

Large USD float (i.e. premium is real and not distorted)

At Friday close, the ADR premium was 15.4% (almost exactly in line with SK Hynix at close and the HL market currently). Looking back over the past few months, the premium has been volatile but fairly sustained in the mid to high-teens.

How SK Hynix compares

So what are the key variables that matter in establishing fair value and how does SK Hynix compare to TSMC on those metrics? While there is a theoretical path to a more relaxed two-way convertibility regime for SK Hynix, our guess is that it is very unlikely in the short to medium-term (clear edge here for anyone able to develop a strong view).

The question then becomes a simple supply-demand problem. The Hynix float is significantly smaller, both in % terms as well as in $ terms. We are also starting from zero in terms of a passive, index/ETF driven bid.

On top of this, SK Hynix is incredibly volatile and the Korean Won has been depreciating in a straight line, increasing the friction costs typically associated with a higher, structural/perma-spread.

In summary — we see limited arguments as to why the spread should be much tighter vs. TSMC and would put the fair value range in the 12-17% range (certainly not under 10%). We would not be surprised if it even widens further in the short-term — at least as long as the memory mania continues.

We would love to hear your views as to whether there should be a strong reason for the spread to compress further in the near term.

When Mr. Market is Bad at Probabilities

We started covering easyJet in early June ever since Castlelake announced its intention to take the airline private. Shares were trading in the 440-460p range back then and despite the still depressed levels vs. NAV, Mr. Market seemed to attach little value to any significant value unlock materialising.

Even after the 5th bid at 690p which garnered Board level support, the shares were languishing at under 610p, an implied merger arb spread of over 13%. We discussed in detail why we thought the execution risk was mispriced and shared our calculator earlier this week when easyJet traded down to 588p and the spread widened to 17%:

Fast forward to Friday, and our interloper case came through: Apollo entered the fray toppling Castlelake with a bid at 715p / share:

The interesting lesson here is that there were three distinct trades to be had along the way, each offering a compelling risk-reward profile under different frameworks:

SoH crisis: largest MoS (>70% discount to metal) and a call option on SoH reopening. Trade-off = timeline.

Castlelake announcement (stock gaps up): decent discount to NAV still, with added bonus of new catalyst

Castlelake 690p offer recommended by board: merger spread of up to 22% (mispriced execution risk)

We were not smart or attentive enough to be there for the first leg, but the circumstances at “decision node 2” are worth highlighting:

Most thought everything was "priced in" after the announcement, as if the catalyst had already taken place. Our view was that this was just the beginning: the asset was now “in play” and the announcement had triggered a new catalyst, with a clear path to value under the UK takeover code (all while trading at a discount to asset value and pre-SoH levels).

Investing is a game of underwriting mispriced rate-of-change. Downside protection, probabilities, timeline are all part of the equation in optimising IRR.

Don't assume the market has it all figured out already and constantly re-underwrite new information at each decision node.

Catch-up

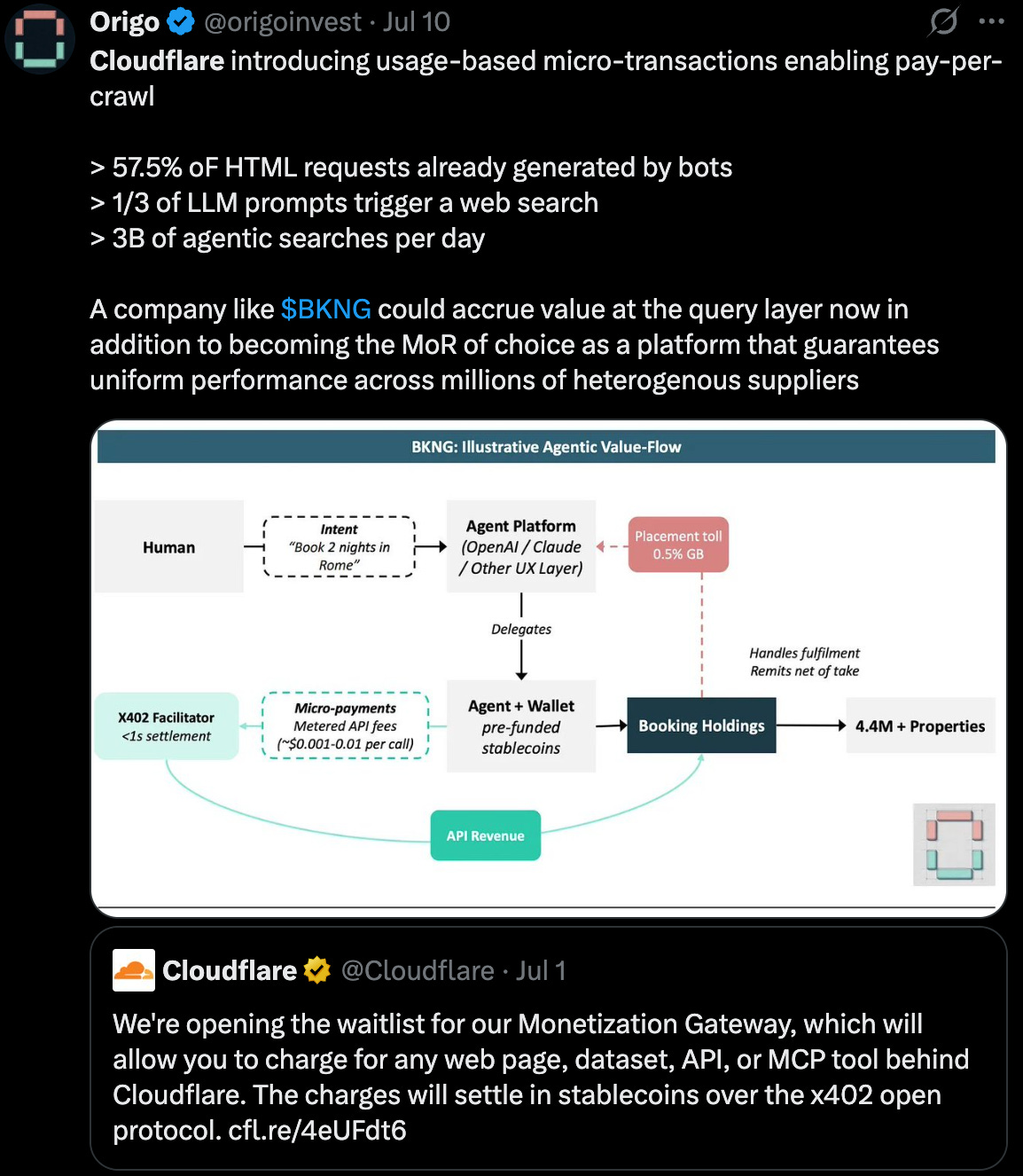

Cloudflare powers over 20% of the internet and we thought their announcement earlier this week around Monetisation Gateway was particularly interesting. The basic gist is that we are fast moving towards a world where agent-to-agent interactions will reshape the plumbing of the online economy, enabling new and destroying old business models in the process.

We did a first deep dive on the topic exploring how the switch to agentic workflows might impact a company like Booking Holdings (as one of the largest paid search advertisers globally) — we highly recommend you give it a read as this will be a big topic in the months and years to come.

As always, thank you for your support.

If you enjoy reading our research, please consider sharing with your network!