Flash | easyJet Board Recommends 690p Offer, Merger Arb Spread Sits at 13%. Too Wide?

Castlelake put forward a (fifth) offer at 690p / share which finally garnered enough support for the Board to recommend. The revised price represents a 23% improvement over their initial offer and a >70% premium to the unaffected price.

Castlelake’s initial statement of intent was met with scepticism (including from a large part of the Street, who put forward a litany of regulatory and shareholder related reasons as to why a transaction was unrealistic).

Our strong conviction was that the commercial rational was compelling enough for Castlelake to underwrite a significantly higher offer, and — as is usually the case in these situations — when there is a price there is a way.

Scepticism still seems to prevail however. At Monday’s closing price of 610p, the market is currently offering a merger arb spread of 13%.

While there is still theoretical bid-launch risk, our initial reaction is that the implied execution risk is mispriced and we wanted to share with you our quick take on execution risk, timeline and overall R/R from here.

Execution Risk & Timeline

1) Non-binding nature: the agreement remains non-binding and subject to due diligence. A Rule 2.7 Offer is due by August 3rd.

We view this as being low risk. Castlelake is primarily underwriting the metal. Outside of refining their maintenance adjustment analysis on a bottom-up basis, they will be intimately familiar with the assets already with a fleshed out strategy around repositioning, operating or parting-out segments of the fleet.

There will be some corporate / operational components of course depending on how they intend to streamline the airline and maximise slot value (alongside partners), but nothing there that we would view as being headline risk.

Castlelake are hungry to deploy capital and did not raise the price 5 times just to walk away.

2) Shareholder approval: Scheme requires 75% approval.

Also low risk. (i) this is a cash offer and (ii) it is structured in a way which allows existing shareholders to rollover into the pro-forma entity.

From a price perspective we are very close to the 700p that was rumoured in the press as being a key threshold for major investors outside the Stelios family.

Yes, the family holds 15.3% but this does not constitute a blocking stake. We think there is a decent chance they choose to rollover, which would also help from a regulatory perspective.

All-in-all the Board would not be recommending the offer without some upstream consent.

3) Regulatory approval: EU ownership and control review is required.

Moderate risk, but mostly timeline related in our view. EU airline rules require an EU carrier to be majority owned and effectively controlled by EU nationals.

The workaround (used in post-Brexit structures) is to have a 51% EU sleeve held by EU nationals (in this case Peter Bellew and Mark Breen) so the BidCo is formally EU majority controlled.

There is a question of substance and effective control look-through. This will be nuanced and there is a list of tools which might be utilised to mitigate regulatory concerns (different share classes, governance undertakings, independent trustees, board quotas, ring-fenced subsidiaries). We think this is ultimately workable but as is often the case with airline mergers / takeovers the risk is on the timeline.

Finally, it is also worth mentioning that interloper upside risk is not out of the question given the strategic value of the slot portfolio. IAG would be a natural even though we think this is relatively low likelihood.

R/R on the Merger Arb Set-Up

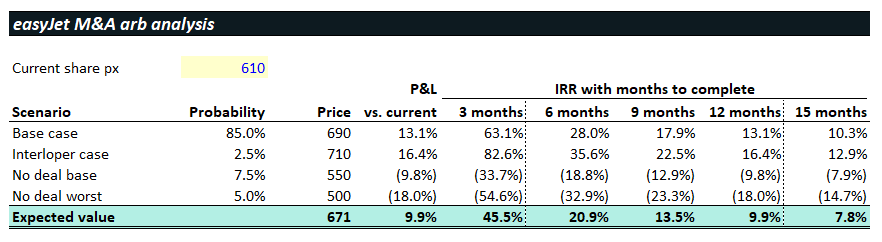

If we had to handicap the deal going through, we would assign a base case probability of 85%. Post bid-launch this probably rises to 95%.

As it stands, we view the outcome distribution as follows:

85.0% chance of a 13% spread

5.0% chance of an improved offer

7.5% chance the deal falls-through and we see 8-10% downside as we trade back to ~550p / share

5.0% chance we drop 15-18% (in-line with pre-SoH)

We would note that the downside-protected nature of the Company has been well highlighted throughout this process.

With the above assumptions we get to a probability adjusted spread of ~10%.

We would estimate the completion timeline to be in the 6-12 month range allowing for a base case underwrite of 13-28% IRR and an expected value underwrite in the 10-20% IRR range.

We can also see a 30-day spread-compression trade, capturing what is in our view the most heavily mispriced component (a Rule 2.7 Offer coming through).

Note: we are not assuming any ticking fee or break-up fee, which would help mitigate any downside and improve the above calculations.

While we are not typically drawn to the convexity of M&A arb trades, we view the R/R here as interesting, with a strong chance of being able to exit a position a few hundred basis points higher in short order without having to take on the risk of a prolonged regulatory back-and-forth.

Will keep you updated if anything material evolves in the above thought process!