Deep | BKNG: Re-routing $7B of Paid Search in the Agentic Era

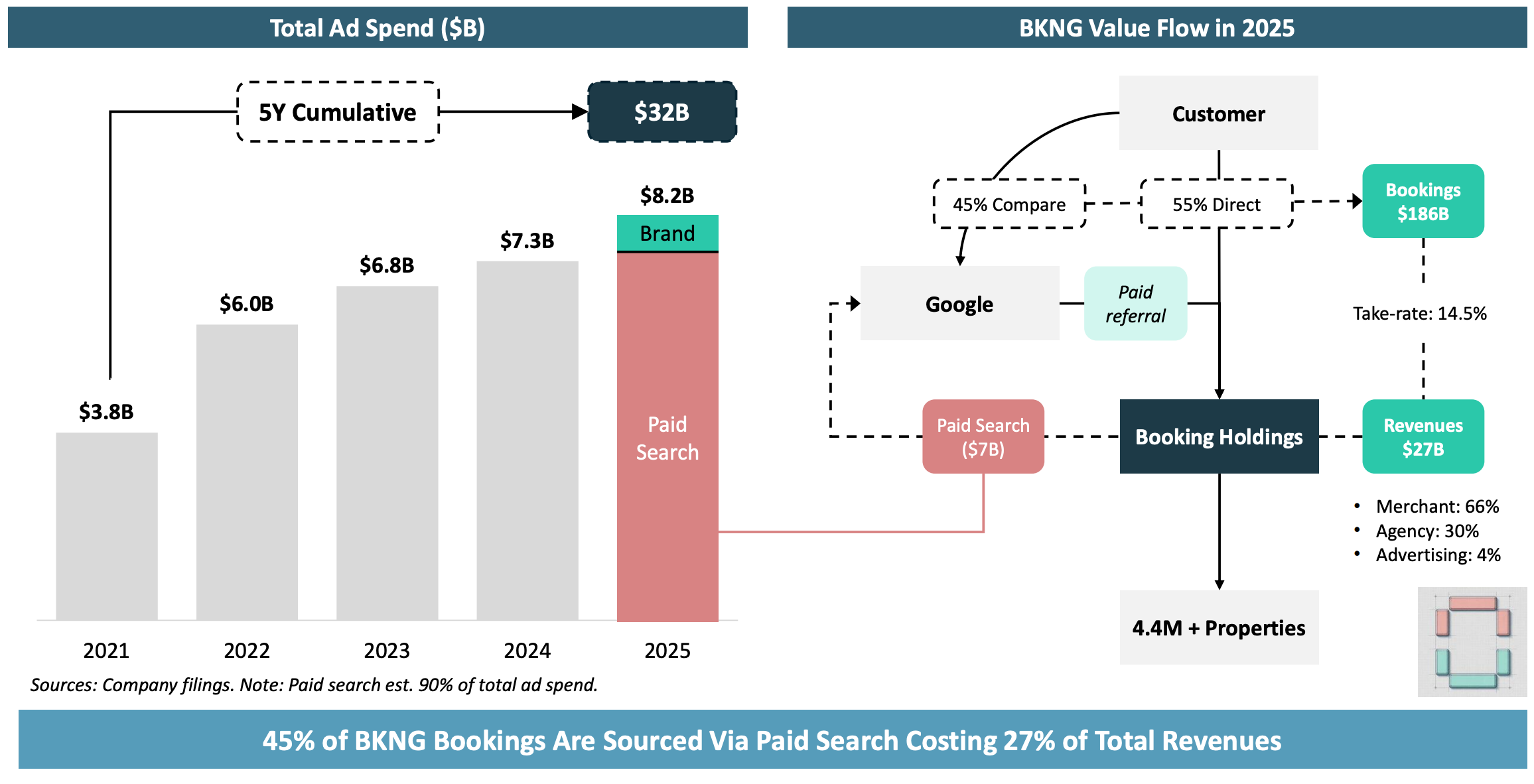

Booking Holdings spent $32B on advertising over the last 5 years.

In 2025 alone, the company spent $8.2B. The vast majority, over $7B, went towards acquiring high-intent travellers via paid search. This is how BKNG sources 40-45% of its gross bookings: a perfectly rational strategy but an acquisition channel which involves significant value transfer, mostly to Google.

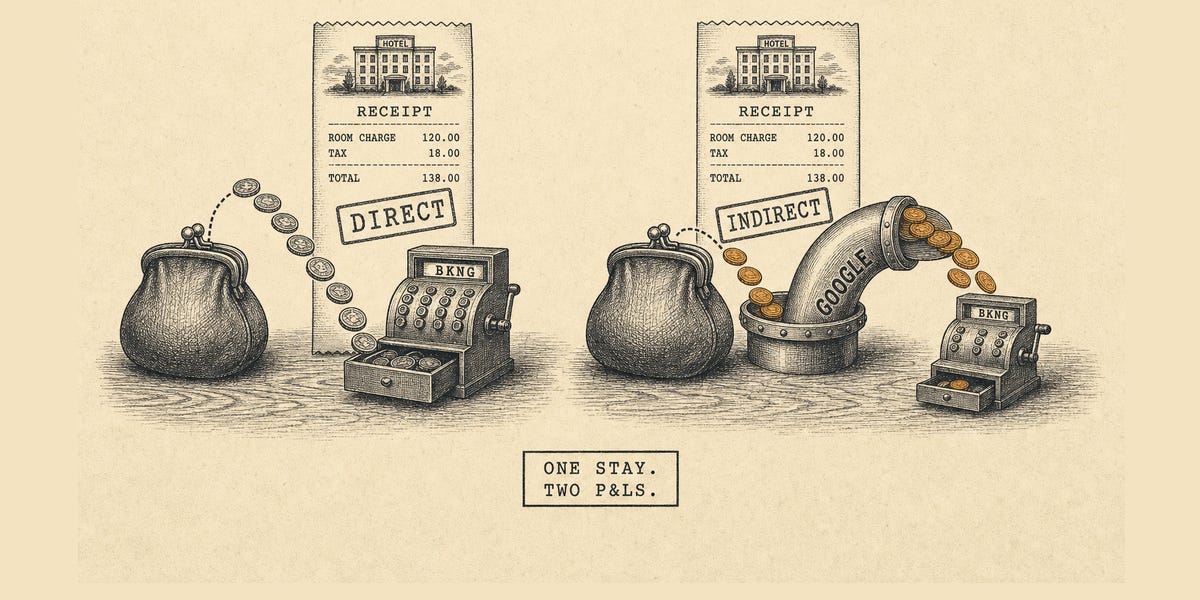

We estimate indirect bookings cost BKNG ~60c for every $1 of net revenue.

Contrast this with direct bookings (55% of room nights) and that’s a 50+ point swing in contribution margin between its most profitable customers and those at the margin. At scale and capitalised, this translates into over $100B of value which Google extracts from BKNG, whose market cap currently sits at $135B.

What happens in a world where the traditional paid search interface is rapidly being abstracted away?

Consumers will increasingly delegate discovery, comparison, and decision-making to AI agents, retaining control mostly at the intent layer.

This shift will profoundly disrupt the plumbing of the online economy. Some businesses will fall off a cliff almost overnight.

At the same time, it will create durable advantages for companies that own assets aligned with how agents make decisions: deep inventory, high-quality structured data, reliable settlement infrastructure, and operational reliability.

A multi-year long/short opportunity.

At Origo, we are in the business of identifying inflection points and underwriting rate of change. To quote Steve Mandel from Lone Pine:

“I don’t need my analyst to tell me when a 10x PE stock is cheap: I need an analyst to tell me when a 40x PE stock is cheap.”

The same can be said on the short side for expensive stocks masquerading as cheap. This is a theme which we believe will be fertile ground for material step changes, at scale, in both directions.

An initial thought experiment.

The space is fluid and rapidly evolving. As we develop our thought process, BKNG is a natural analytical starting point as one of the largest advertisers in paid search. In the note that follows, we attempt to re-underwrite its P&L in a pro-forma world dominated by agentic workflows.

Same Booking, Two Margins

BKNG booked 1.2 billion room nights in 2025. Its reported direct-channel mix was in the “mid-50s”. Additionally, we can infer from historical guidance that approximately 10% of its ad budget goes towards brand marketing, while the rest is put towards performance marketing (mostly paid search).

At a high-level, we can summarise the value flow as follows:

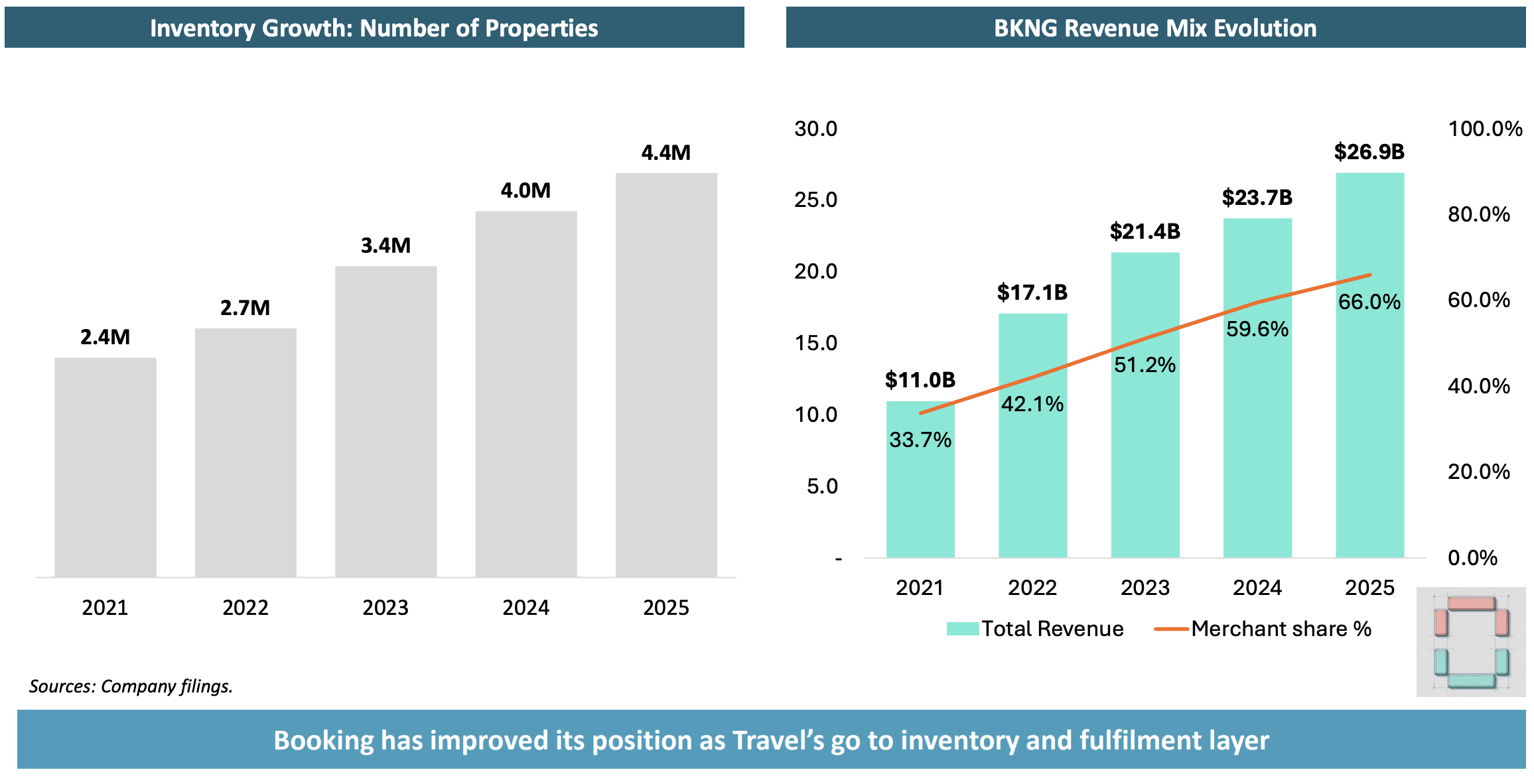

BKNG aggregates an inventory of 4.4M+ properties on its platform

The platform handles $186B in gross bookings

55% of customers book through the platform directly (= high margin)

45% are paid referrals sourced indirectly (= low margin)

BKNG nets $27B in revenue at a 14.5% blended take-rate

BKNG then pays an est. $7.4B to Google et al.

In short, Booking is routing 27% of its top-line back to Google in exchange for a steady flow of paid referrals. That number is even more stark when we attempt to isolate the margin associated with the indirect channel: for every dollar of net revenue coming in, 60c goes back to Google.

Acquiring marginal volume this way is perfectly rational business behaviour. Needless to say, the direct customer is significantly more profitable which is why the organic brand has real value: we are talking about a 50+ point swing in contribution margin between the two channels.

Which cohort will be a first adopter of agentic commerce? We would argue the lower-margin, paid search user, who by definition is a comparison shopper: query-based with limited loyalty.

And where will their agents go? Not to the highest bidder for a click, but to a counterparty that can quote, settle and reverse a stay with zero friction.

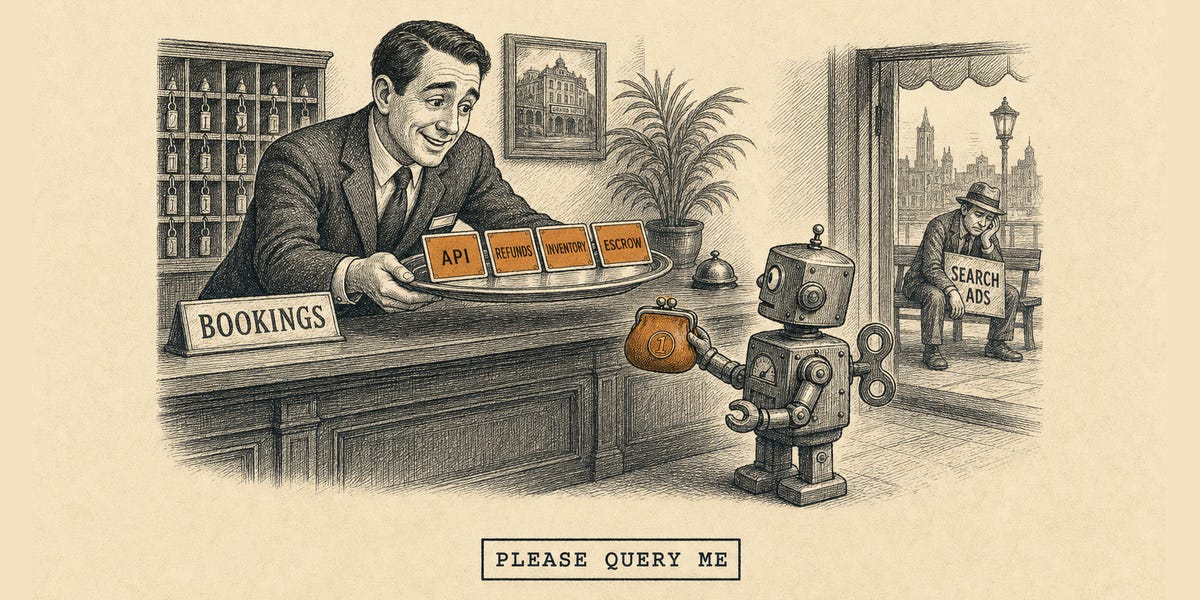

Please Query Me

Machines don’t click ads

Attention is no longer monetisable in a world where web traffic is dominated by agent-to-agent interactions. Simply put:

Humans compare hotels on Google and click ads

Agents query platforms and compare inventory through APIs

A user will provide high-level intent (“book a 4-night trip to Barcelona under $900”), and their personal agent will handle research, comparison, negotiation, and booking with minimal further input.

Paid search loses its position as the primary discovery layer as agents are motivated by a completely different set of objective incentives: they are looking for data-driven, low-friction, reliable counterparties.

What Matters at the OTA Layer

In our opinion, business models that rely purely on traffic arbitrage and re-directs will cease to exist.

Providing structured, quality data will still be relevant but the bulk of the value capture should accrue to platforms that also handle the settlement layer.

A key question is whether agents prefer to deal with aggregators or individual hotels directly.

The Preferred Merchant of Record (MoR)

A hotel booking is not a digital good. It is a promise that gets fulfilled in the future, in the physical world, often by a small business and with a non-zero failure rate. Agents optimise for an MoR that absorbs that operational risk:

Verified inventory

Machine-readable contract with uniform terms

Escrowed payment and programmatic refunds

Track record

BKNG provides exactly this at a level that most individual hotels and smaller chains cannot easily replicate on their own. Its merchant model allows it to handle complex, cross-border payments and compliance, while its massive data layer and supplier relationships create a network effect that is difficult to bypass.

Over the past 5 years, BKNG has aggressively expanded its inventory all while scaling the merchant share of its business. As such it should be well-positioned to capture agentic “footfall”.

Note: it will be interesting to see how the major hotel chains will adapt. Since they should be competitive at the settlement layer, there will be an optimisation question for agents between inventory breadth and economics. It is conceivable that agents will query BKNG first before settling with the hotel chain directly.

Survive AND Thrive?

Today, BKNG is an aggregator that guarantees performance across millions of heterogeneous suppliers and this is more valuable to a machine than to a human. Machines have zero tolerance for ambiguity in settlement and recourse.

Not only does BKNG have a shot at being the preferred MoR, it also means that its share of merchant vs. agency revenue should accelerate. This is important because merchant economics > agency economics. More control, investment float, higher take-rate, higher margin (a flywheel which in turn helps BKNG become more competitive economically vs. the major hotel chains).

What This Could Look Like

We can summarise our thoughts with three key points that could plausibly support a bull case:

Agents will interact with the platform without requiring ads

BKNG will accrue value as a query-layer (inventory)

BKNG will accrue value as a settlement layer (MoR of choice)

Note on accruing value as a query-layer: we highly recommend you read Cloudflare’s recent post announcing Monetisation Gateway. This lays the foundation for usage-based micro-transactions, enabling internet assets (web pages, datasets, APIs, MCP tools) to monetise pay-per-crawl on x402.

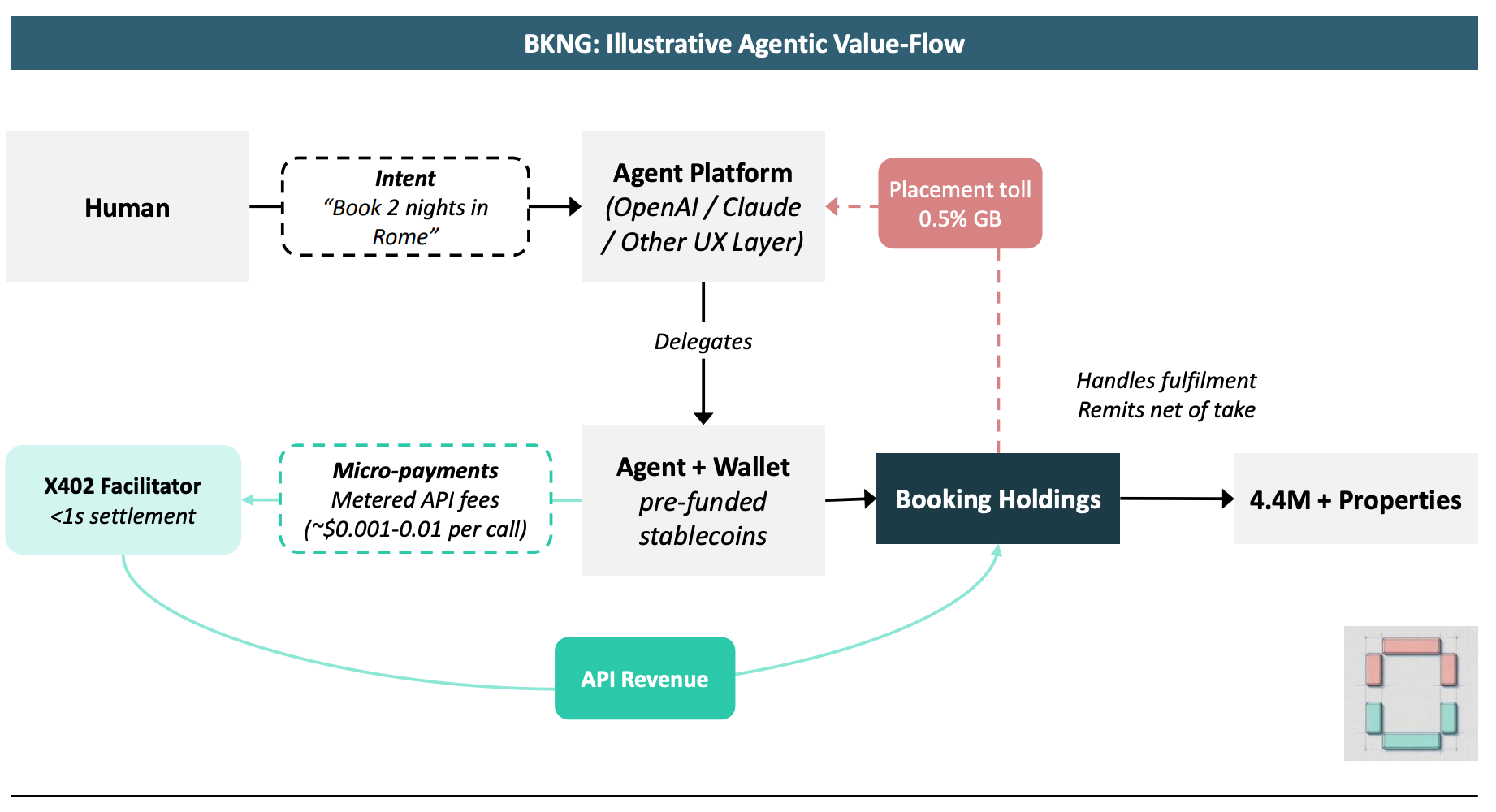

The Agentic Workflow

We take a look at an illustrative agentic flow-chart which impacts the P&L as follows:

Removes the need for paid referrals (performance marketing expense)

Introduces a new API revenue stream at the query-layer

Introduces a potential expense line back to the agent platform

We also anticipate the mix of revenue to become binary over time: agent-sourced bookings should in theory all be merchant-based (either that or BKNG is just used as a query-layer).

The “placement toll” back to the agent platform is a key variable which will very much depend on the head-to-head negotiating leverage of both parties. Unlike the current relationship with Google, BKNG offers intrinsic value in an agentic world which ultimately benefits the end-users of the agent platform. We assume some value extraction by agent platforms but reason that this should remain limited compared to the one-sided and monopolistic share currently captured by Google.

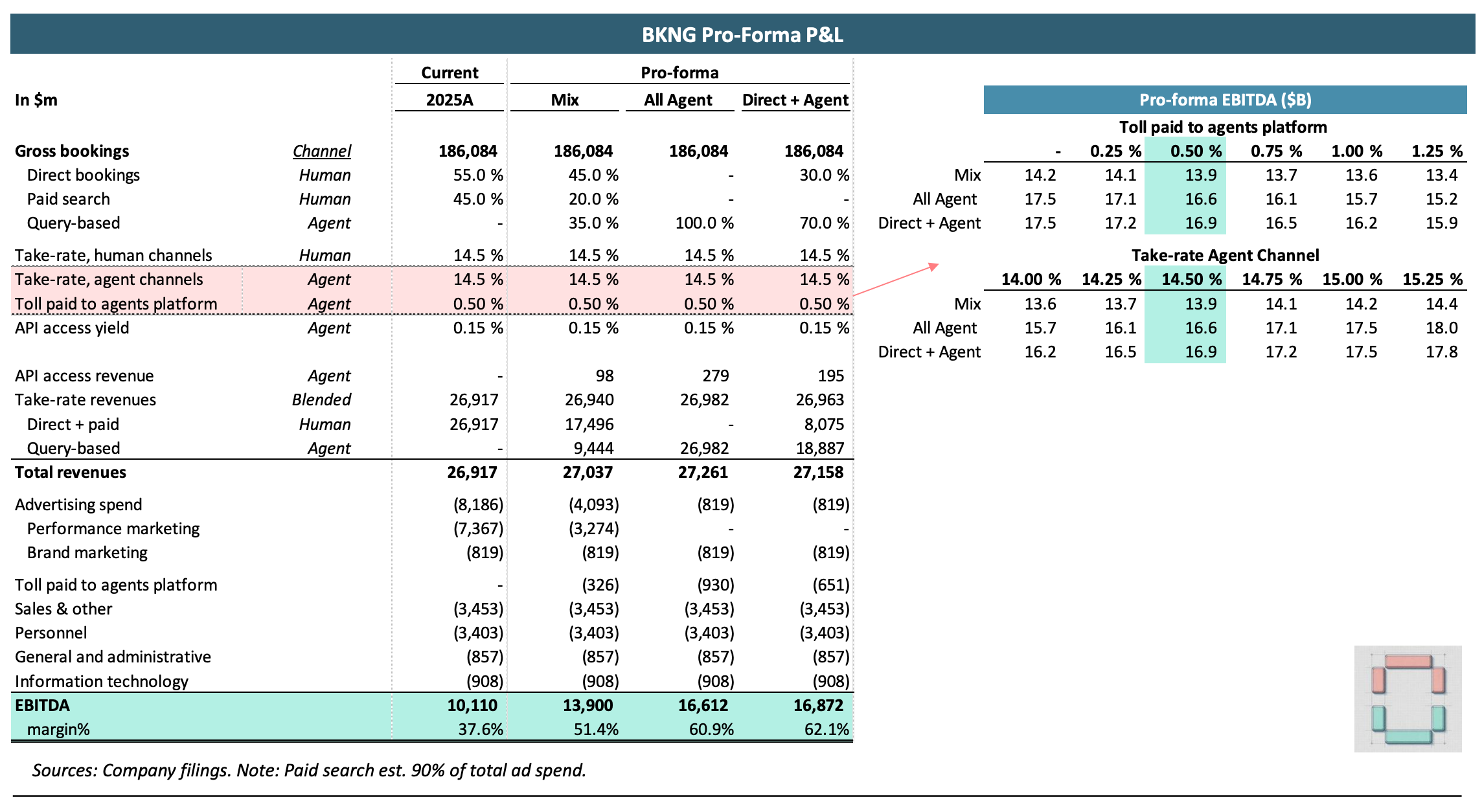

The Pro-Forma P&L

We look at a few different scenarios in terms of acquisition channel mix:

Mixed: agents capture 35% of bookings, disproportionately from paid search

All agent: longer-term hypothetical scenario where agents capture 100%

Direct + agent: all paid search converts to agent, some direct remains

The channel mix dictates performance marketing expense which we scale pro-rata to paid search bookings. In addition, we introduce the toll paid to agent platforms and introduce the API access revenue line-item. Everything else is modelled “as-is”.

Under these assumptions, BKNG’s EBITDA would increase by 40-60%.

We would also highlight the following factors for consideration:

Brand marketing: assumed flat, arguably less necessary in an agentic world

Take-rate: agent-channel take-rate should be higher if 100% merchant

Volume of bookings: in a bull case BKNG actually gains market share

API yield: based on actual bookings (query volume should be much higher)

Cost structure: efficiencies should emerge over time here as well

Final Thoughts

Investing is a game of identifying underpriced probabilistic outcomes.

There are clearly many moving parts involved here, and while our initial hunch is that BKNG could emerge as a big winner, we could end up being completely wrong as the technology evolves.

We do not hold any position (yet) but at ~14x EBITDA today we view the name favourably. Our goal, over time, is to build a long/short basket within this theme as we develop our conviction levels on the direction of travel.

Thank you for reading up to here. At a minimum, we hope you found this case study thought-provoking!