Weekly | Alt GPs – bottom is in?

+ SK Square: how much juice left in a post-IBKR world

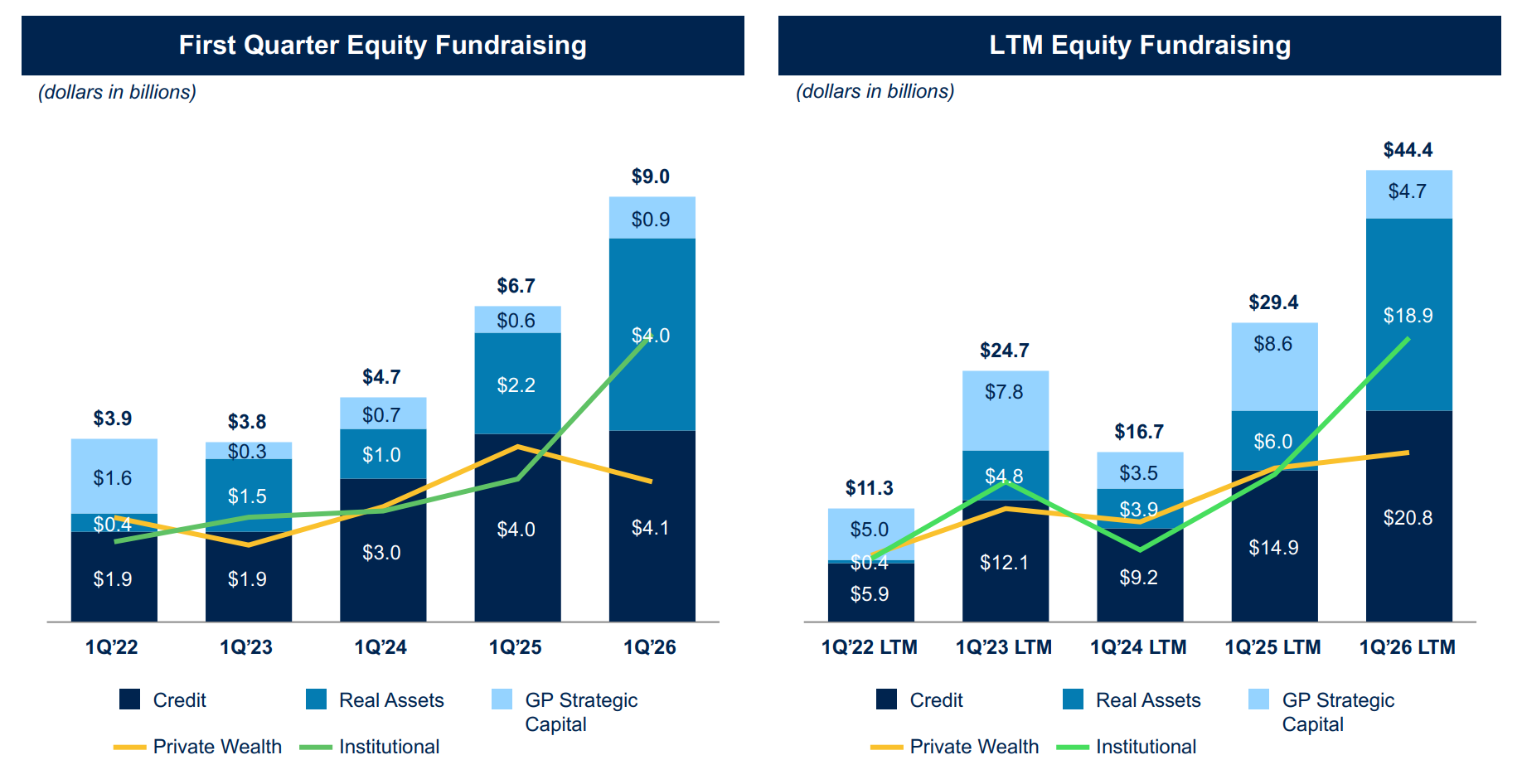

Alt GPs: incoming narrative violation

In early March we wrote extensively about how fears of a Private Credit-induced systemic shock had sparked an indiscriminate sell-off in financials across the board. Our view was that private markets are not going anywhere and we had reached a point where the market was conflating Alt GPs, BDCs, Banks and everything in between. Alt GPs hit local lows 50-70% off ATHs later that month.

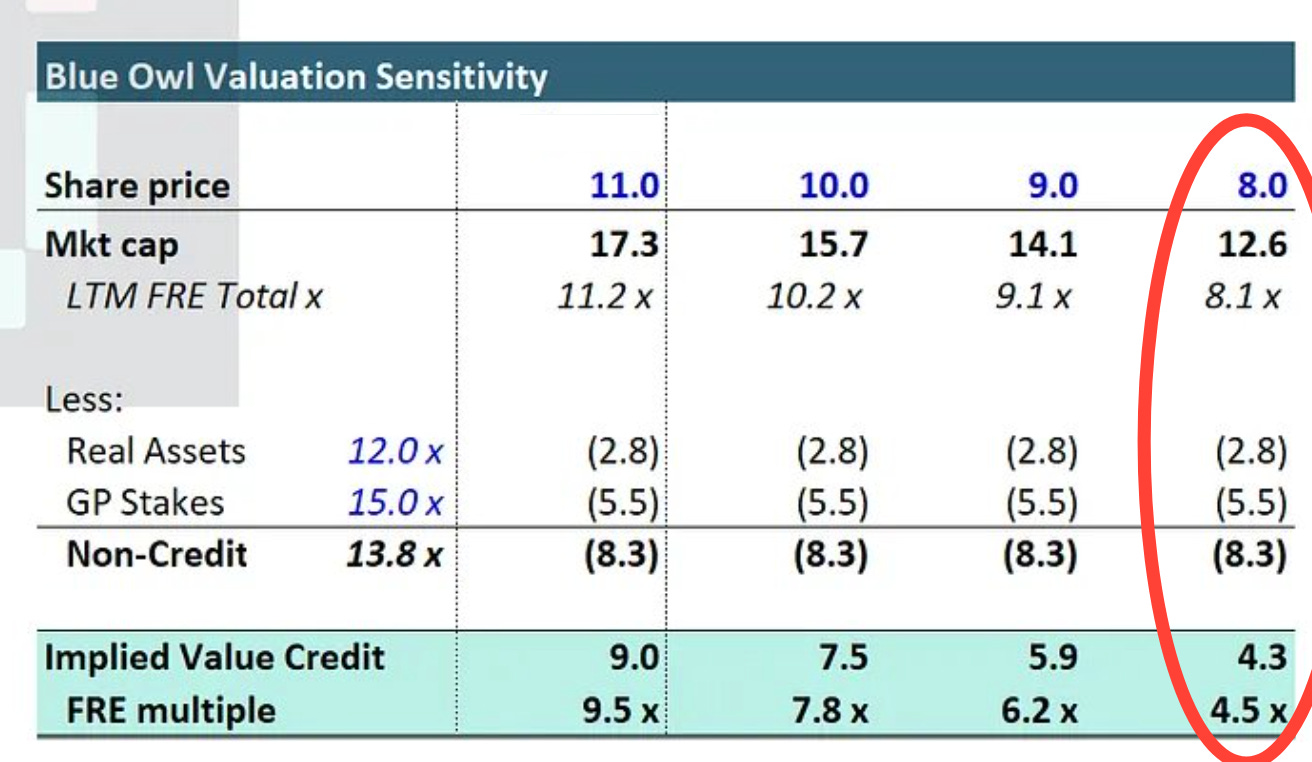

While a breather was warranted after an incredible 3-5 year run, with valid concerns over market saturation and retail penetration, implied multiples in some instances looked too cheap even on a run-off basis.

We also reached peak divergence between what insiders were saying and what was being propagated in the media – the cynical view being most entertaining.

Finally, there is a prevailing assumption that a potential late-stage credit cycle is unconditionally negative for AUM growth. While it may certainly affect some channels at the margin, sophisticated LPs will over allocate to vintages with a spread-widening backdrop. In a recession, credit always gets bid first prior to equities recovering. We also saw in our Apollo & Athene deep-dive how in the case of Athene AUM growth can be completely detached from the credit cycle.

The impending Private Credit doom has been an incredible driver of clicks – but narrative eventually needs facts to follow-through – and early Q1 signs are pointing towards uncomfortable truths for the bears, with a decent chance that the bottom is in.

Q1 read-through: Ares and Blue Owl

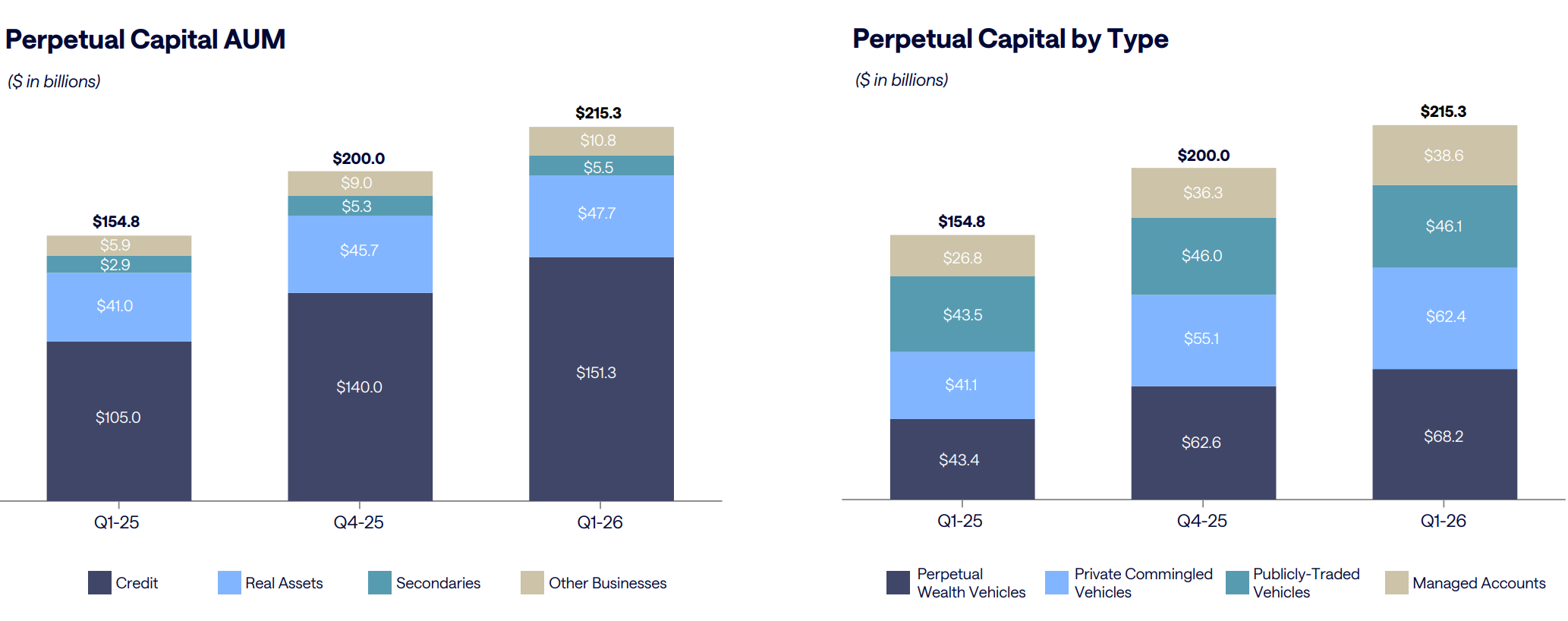

Blue Owl and Ares released Q1 earnings this week. Whilst not everything was perfect, the main focus point – AUM growth – has largely surprised to the upside.

In fact whist I expected moderate growth (particularly in closed-end fundraising) I was positively surprised to see Ares record large net credit inflows (+$11B) in their Perpetual Capital segment (primarily BDCs / open-ended funds).

In the case of Blue Owl, which at ~$8 / share was being priced as if their credit business would suffer net quarterly outflows at (or even in excess of) the redemption cap, numbers were significantly ahead of consensus – albeit while they emphasised YoY numbers in their presentation, sequential QoQ figures were moderate to flat-ish.

Blue Owl has been the poster child for all that is wrong with Private Credit – and the whiff of a Q1 earnings driven narrative violation was enough to spark a short squeeze, propelling its shares up +10%. We will also note that the shares held by its founders – Doug Ostrover and Marc Lipschultz – are no longer pledged, removing an important overhang on the stock and likely marking the bottom.

Early innings of a trend reversal

Since Blue Owl (right or wrong) is widely perceived to be in the bottom quartile of GPs, its results have created positive anticipation for the rest of the sector due to report over the coming weeks.