Weekly | Alts in Focus

+ Korea discount and portfolio updates (when to buy/sell)

Private markets: not going anywhere

The fear of a Private Credit induced systemic risk has sparked indiscriminate sell-off in financials across the board: Banks, BDCs and Alternative Asset Managers.

We’ve already touched upon in previous posts why we believe Alts do not belong in the same boat as Banks / BDCs. These are asset-light, high margin, fee-based businesses. Moreover the largest franchises today have effectively insulated themselves from any single point of failure through product and funding source diversification. Speak to large institutional LPs and they remain for the most part very positive on allocations to privates. These are multi-year decisions that do not get rebalanced overnight as a function of media sentiment.

It is not our job to argue with the market though and we will happily take what it offers. Some highlights:

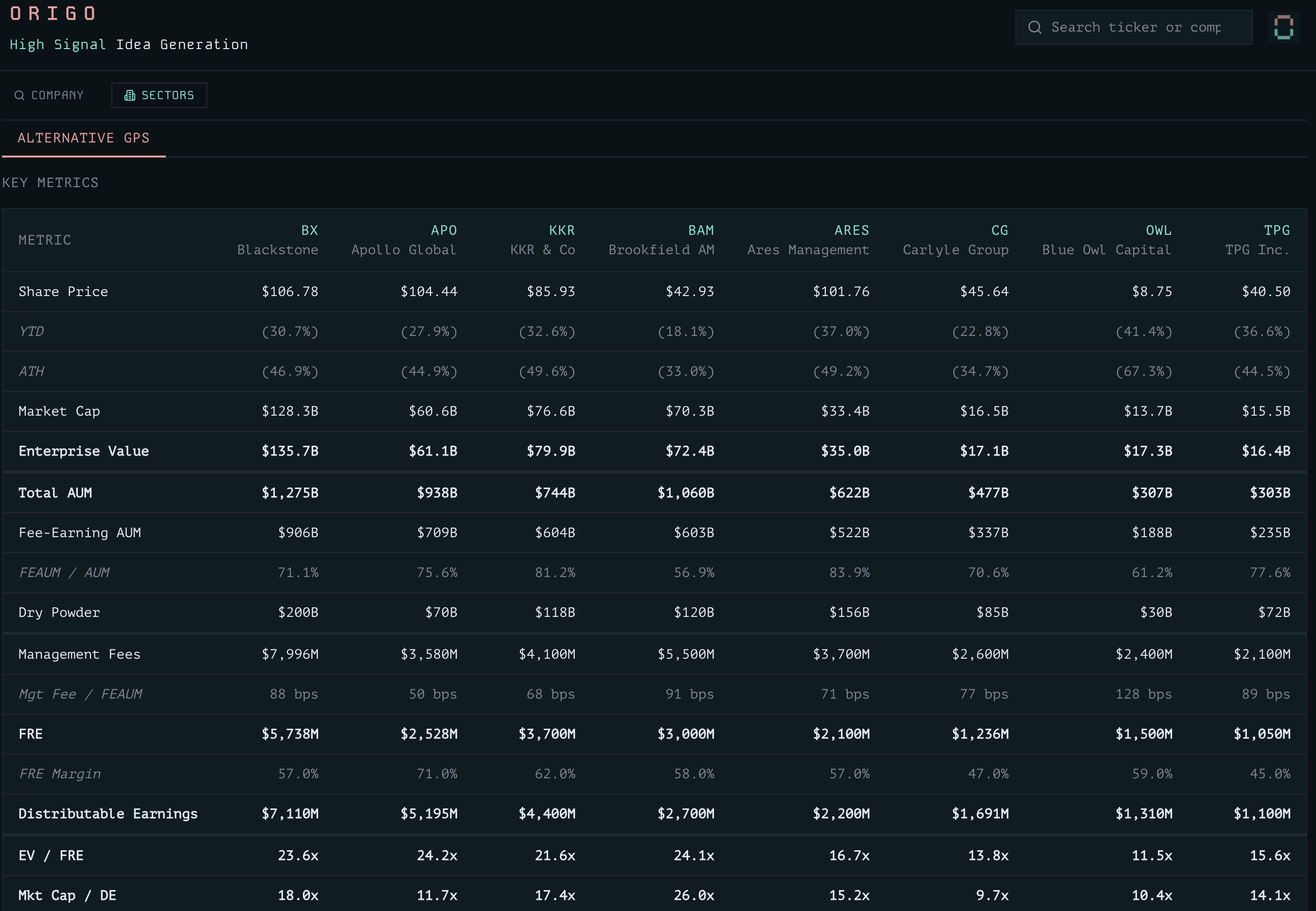

Blackstone: down 31% YTD and 47% off ATH

Apollo: down 28% YTD and 45% off ATH

KKR: down 33% YTD and 50% off ATH

While Alts are coming off arguably elevated levels, we are entering interesting territory relative to where these businesses have historically traded in terms of FRE multiples.

The debate when evaluating an appropriate multiple and differentiating between managers boils down to (and these are all correlated):

Growth prospects

Fee-stream stickiness and soft factors (reputation, process, goodwill)

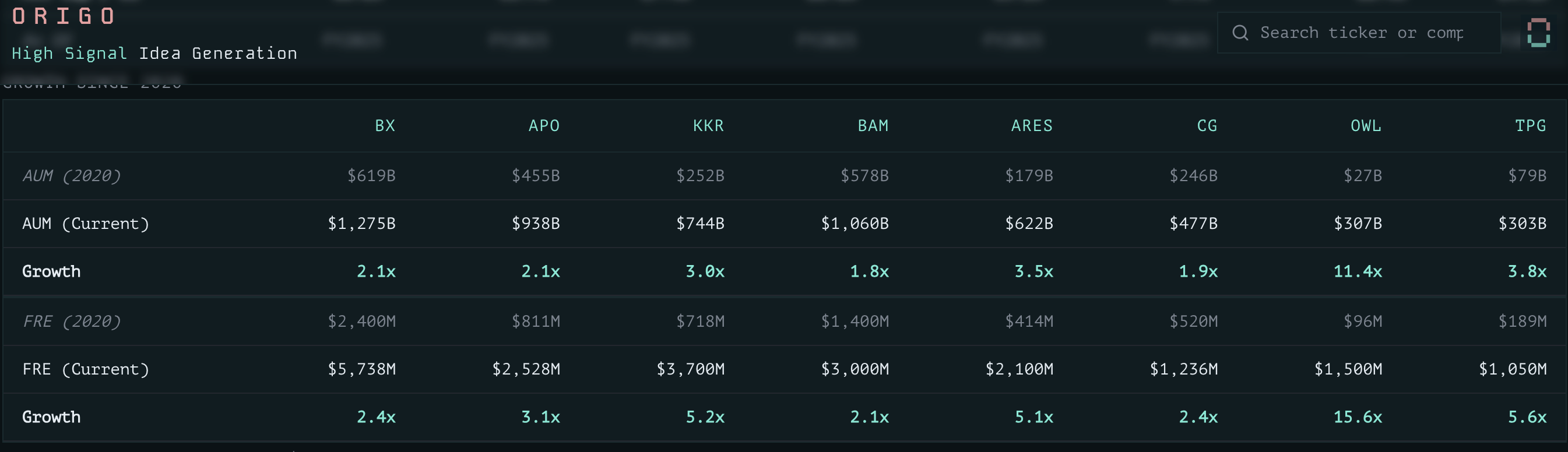

Growth

Over the past 5 years the top franchises have experienced tremendous growth as the industry consolidated and the largest players disproportionally benefited from increasingly concentrated allocations from LPs.

Over that period AUM has grown >2x and which has turbo-charged FRE 2-5x. Worth noting that the mix of FRE has also “improved” in the sense that it has become predominantly weighted towards base management fees.

This is in contrast to their Private Equity origins (when performance fees were the main profit driver) but a necessary transformation as they became public entities (with higher multiples being assigned to predictable, long-term revenue streams).