[Weekly] Can You Still be a Stock Market Genius? Grading the Spin-Off Class of H1 2026

Welcome back!

It has been a busy week in spin-off land with both the HON→HONA and SPGI→MBGL transactions taking place. This brings us to a total of 11 spin-offs in H1’26, well on pace to exceed the 13 we saw in 2025.

We’ve covered names like Honeywell in idiosyncratic detail. Today we wanted to take a step back and take a look at the empirical data more broadly.

How have recent SpinCos performed? Do RemainCos get overlooked? Let’s dig into the numbers and see whether Greenblatt’s wisdom still holds true.

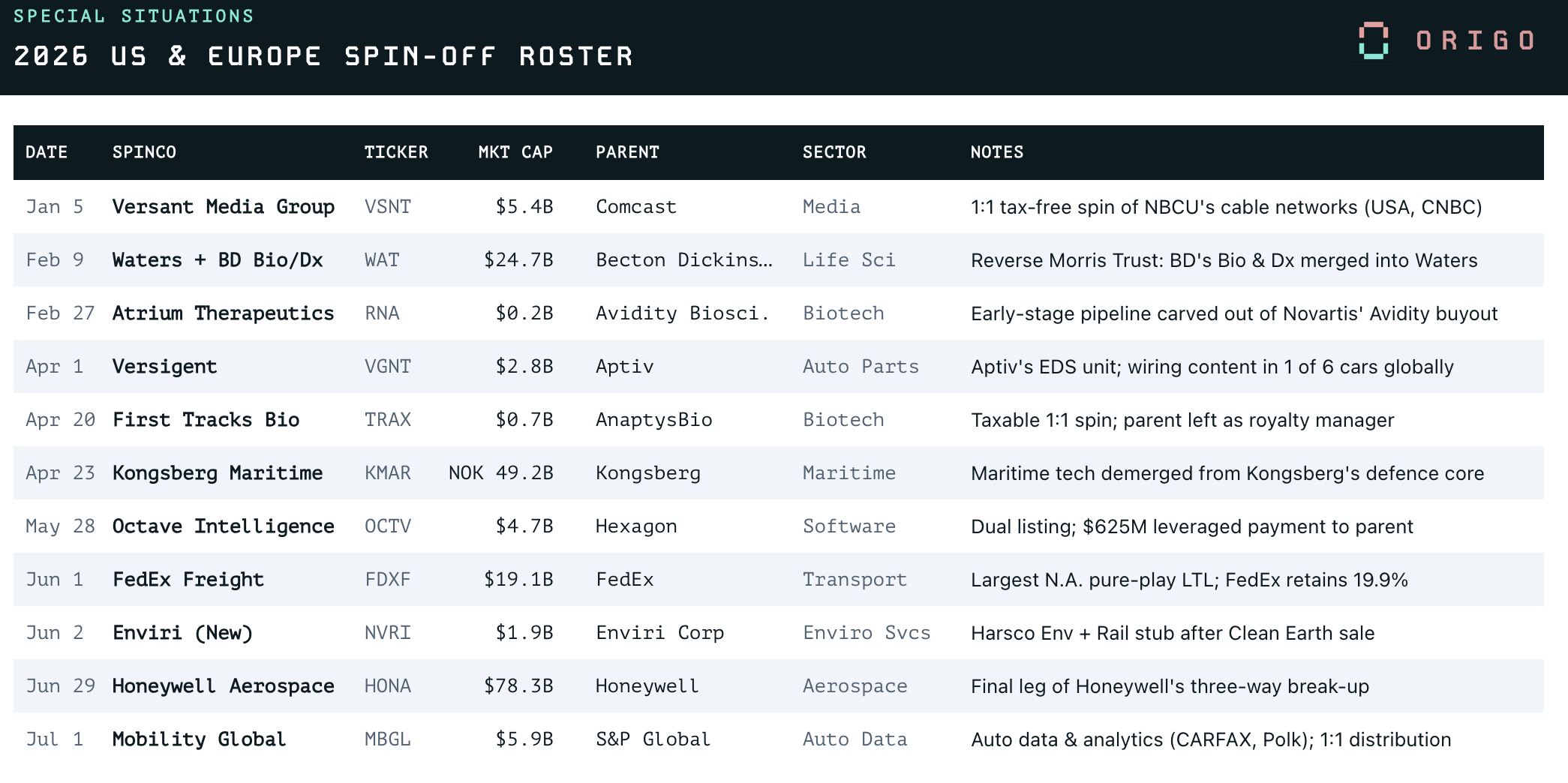

Class of 2026 (So Far)

We have seen a eclectic mix of names. The sector spread runs from aerospace (Honeywell Aerospace), freight (FedEx Freight) and auto parts (Active’s Versigent) to cable media (Comcast’s Versant), industrial software (Hexagon’s Octave), maritime tech (Kongsberg Maritime), environmental services, auto data and a pair of biotech carve-outs:

Some of these were classic “shed the declining asset” spins (Comcast→VSNT) while others involved the crown-jewel (Honeywell→HONA). In between we had a reverse Morris Trust (BD’s Biosciences unit merged into Waters), a taxable 1:1 spin that leaves the parent as a royalty manager (AnaptysBio), a dual-listed carve-out that sent $625M back to the parent (Octave), a 19.9% retained stake (FedEx), and a pipeline spun out so Novartis could buy the rest (Avidity’s Atrium).

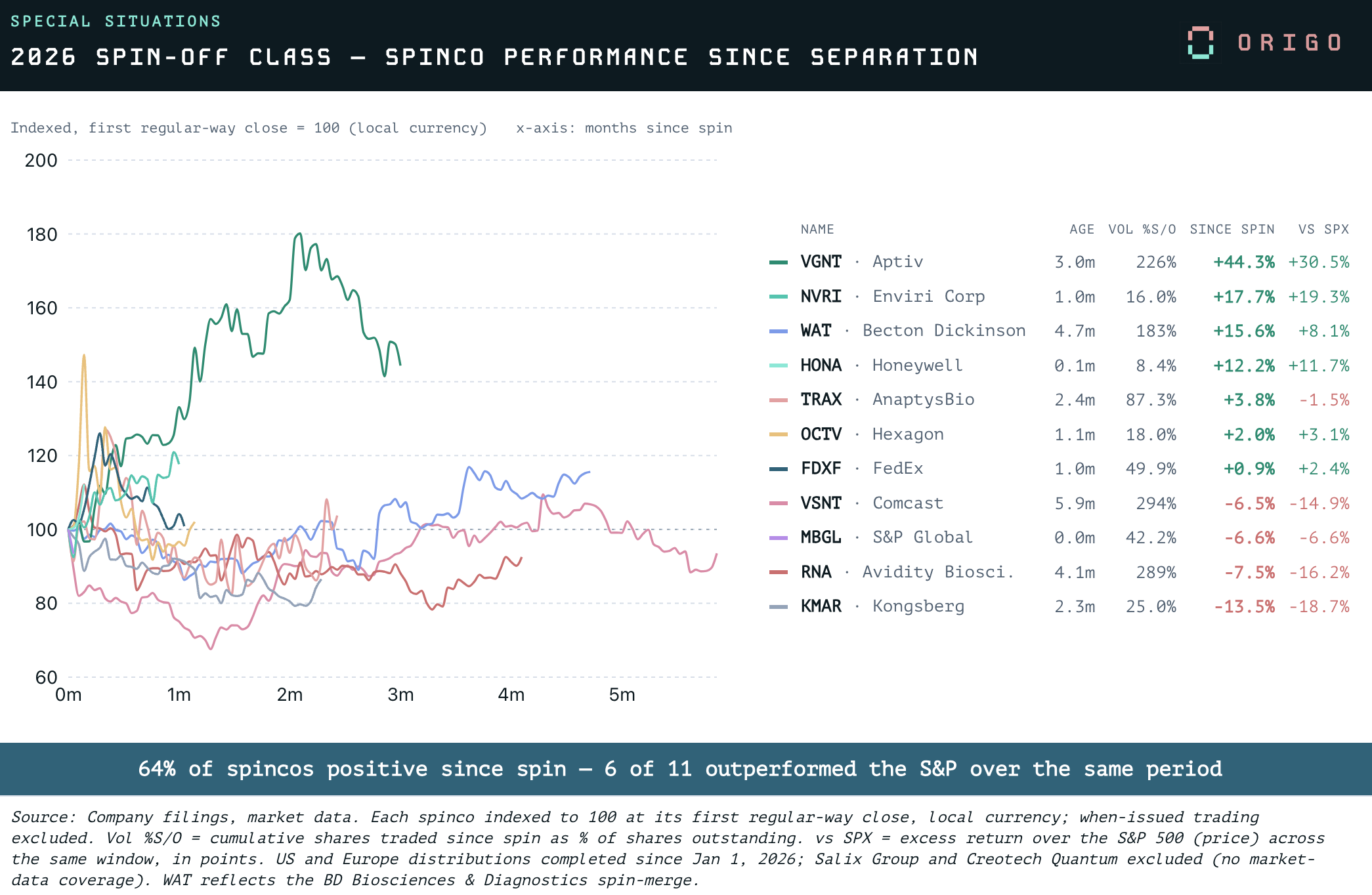

64% of these have had positive performance from their first regular-way and close and 6 of 11 outperformed the S&P over the same period.

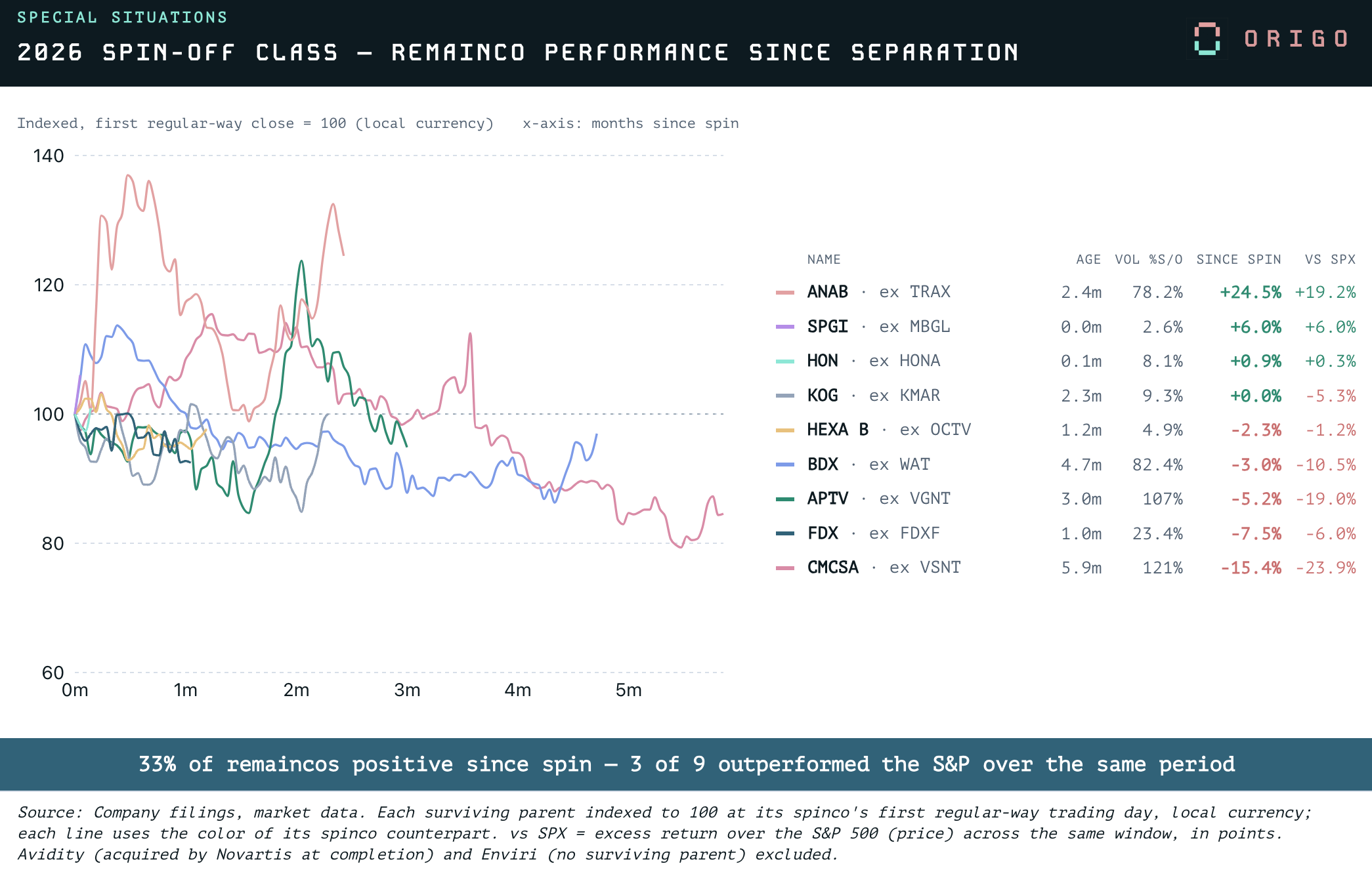

This stands in contrast to RemainCo where only a third outpaced the S&P. In both cases, we did not not any particular correlation between volume (% traded since spin) and performance.

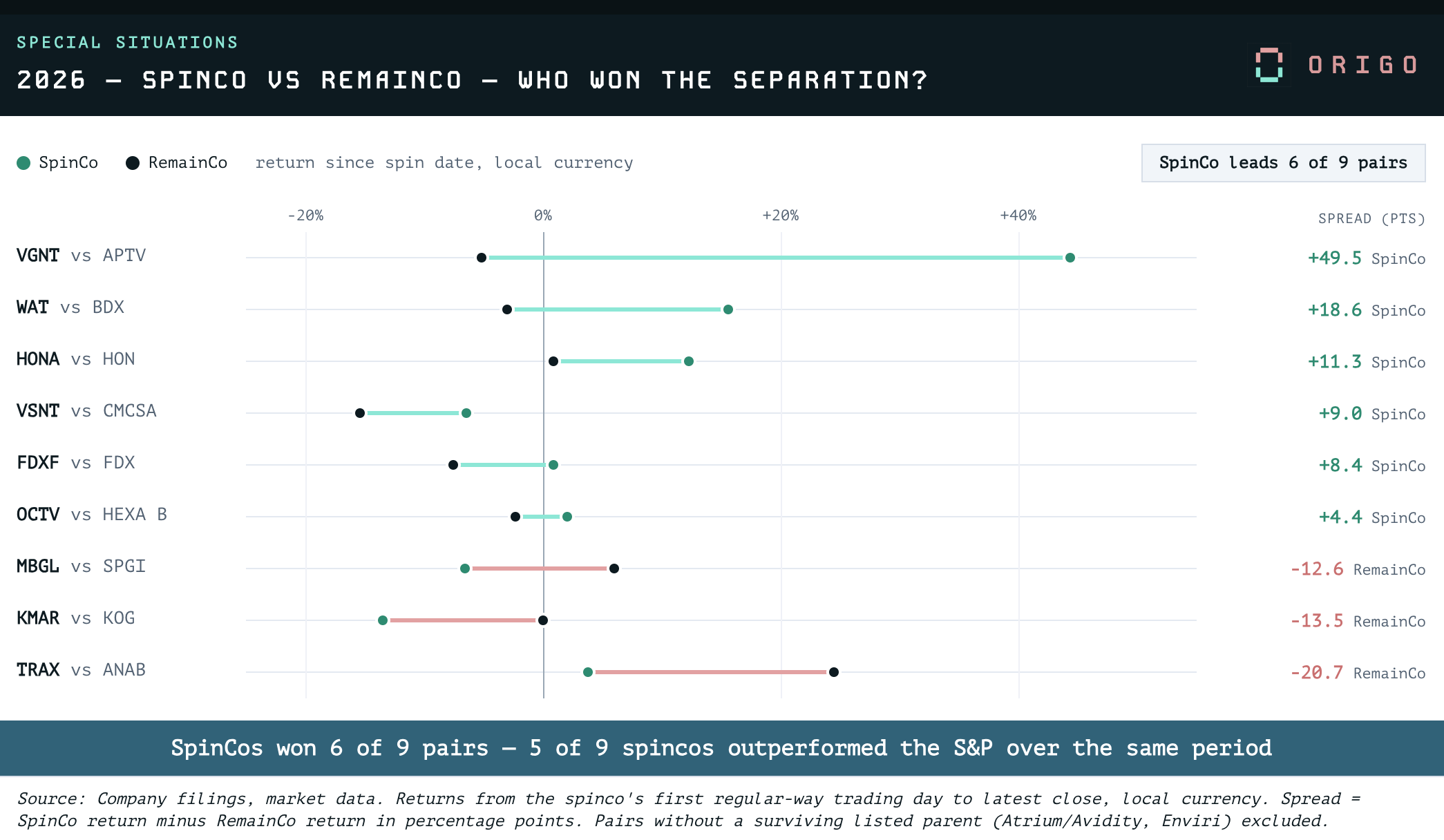

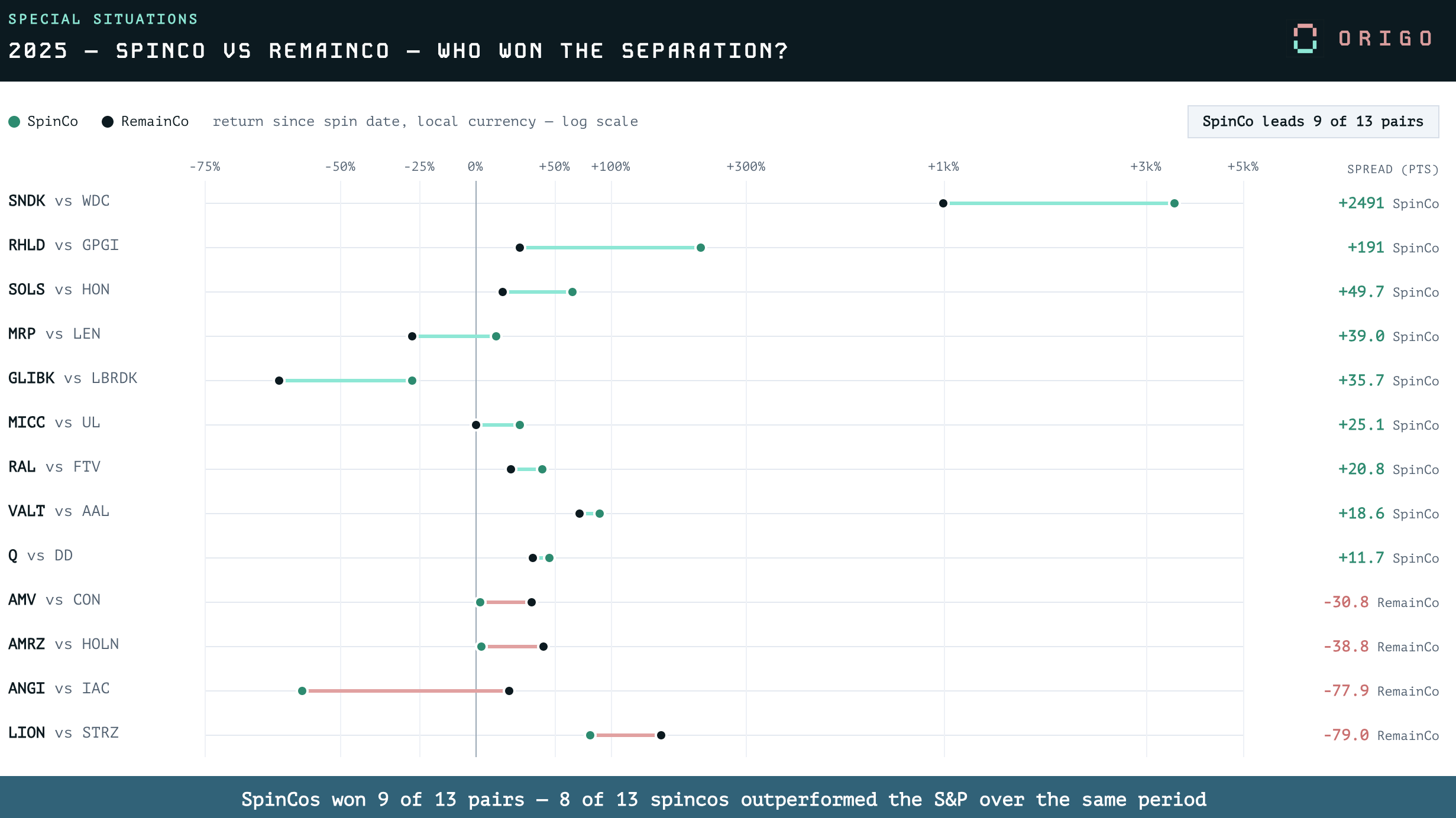

We can illustrate the head to head battle between RemainCo and SpinCo in the below chart (note that this excludes the pairs without a surviving listed Parent).

Here, we can see that SpinCo leads 6 of 9 pairs with only ANAB, KOG and SPGI coming out on top of the RemainCo side.

Overall, it is still early days with 7 SpinCos having less than 3 months of trading history. Out of curiosity, we ran the same analysis on the Class of 2025 and the results were even more convincing.

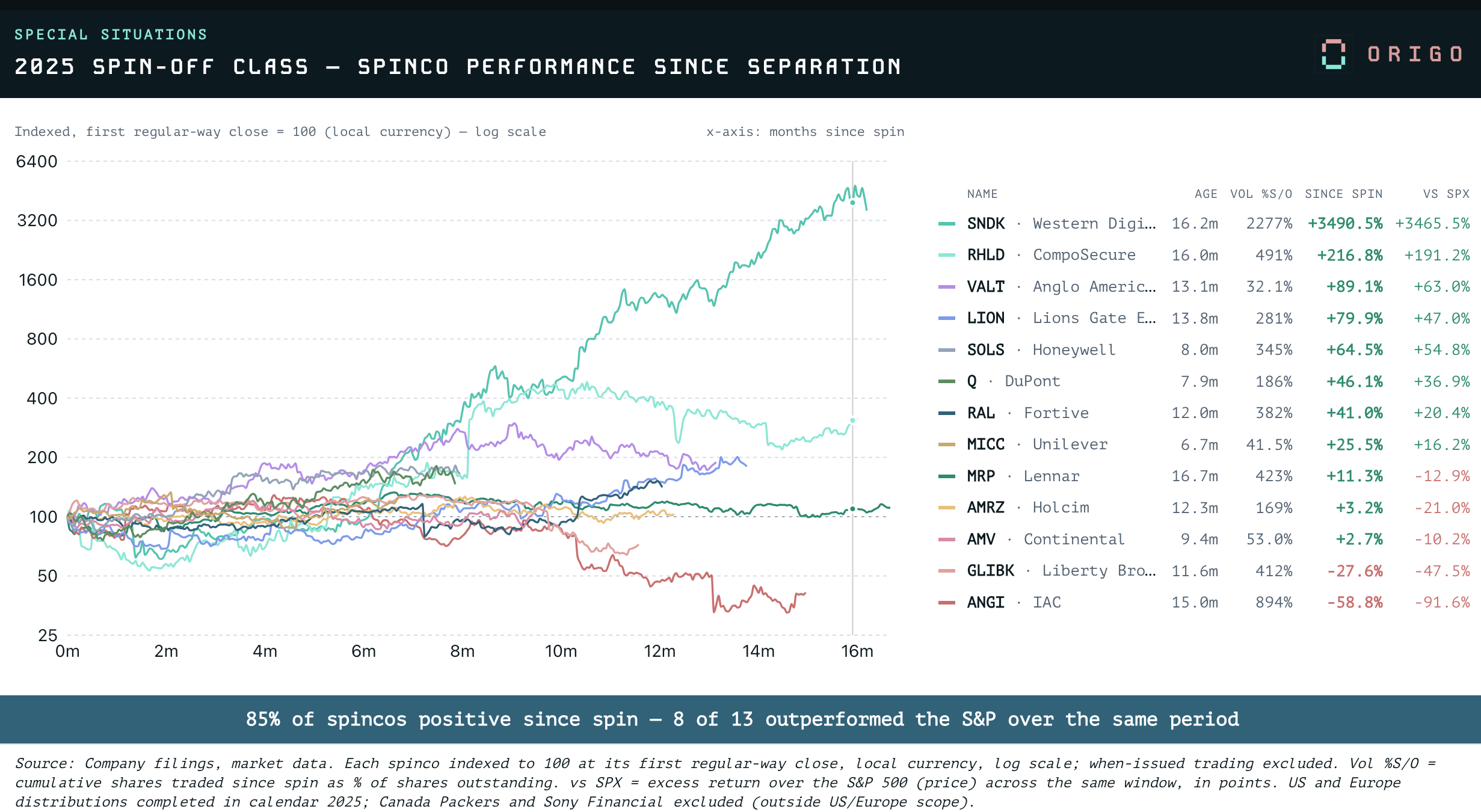

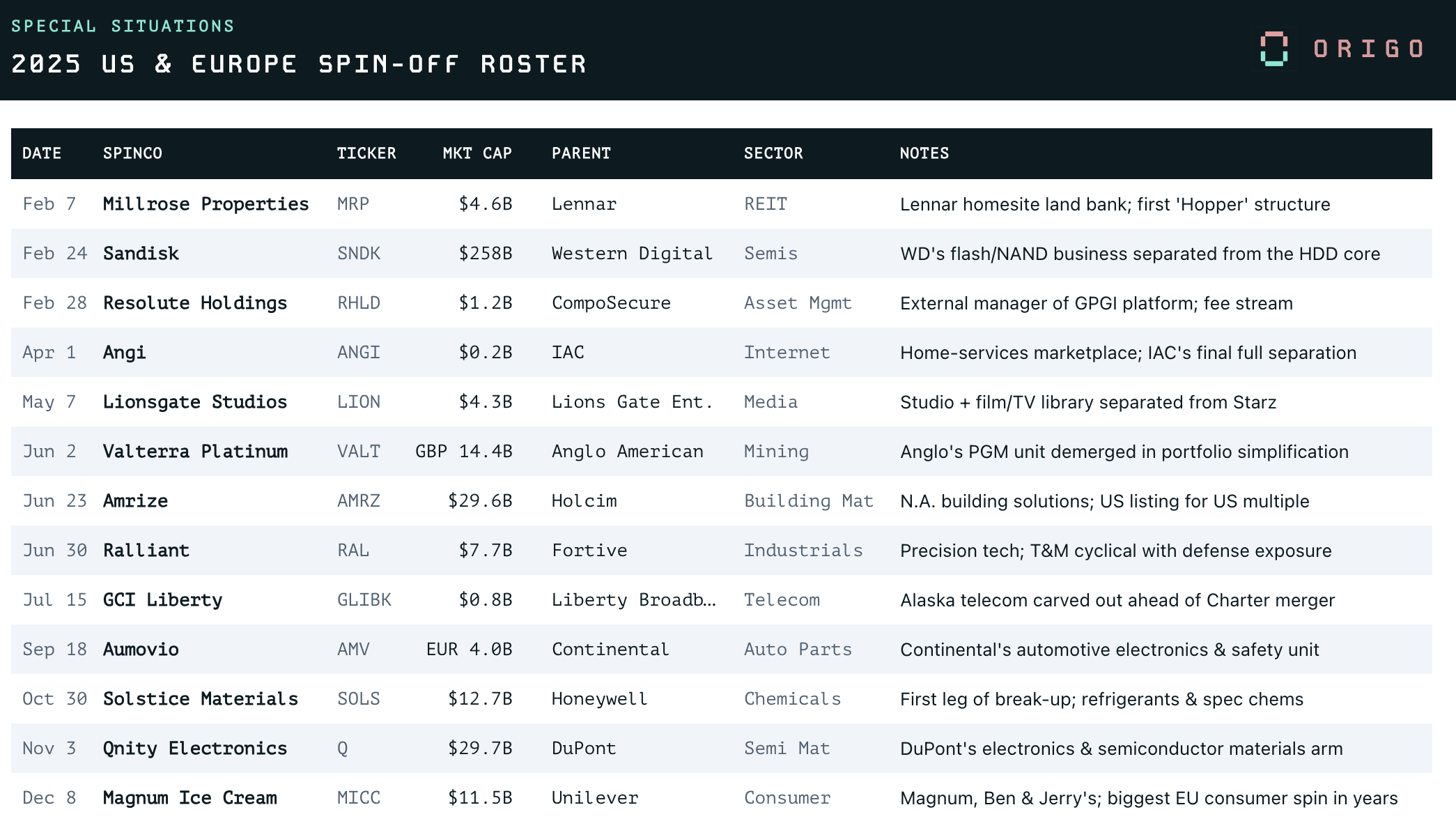

Class of 2025: An Outstanding Vintage

For this class where the “youngest” spin is MICC (~7 months), we found the following:

85% of SpinCos have displayed positive performance and 8 of 13 outperformed the S&P over the same period

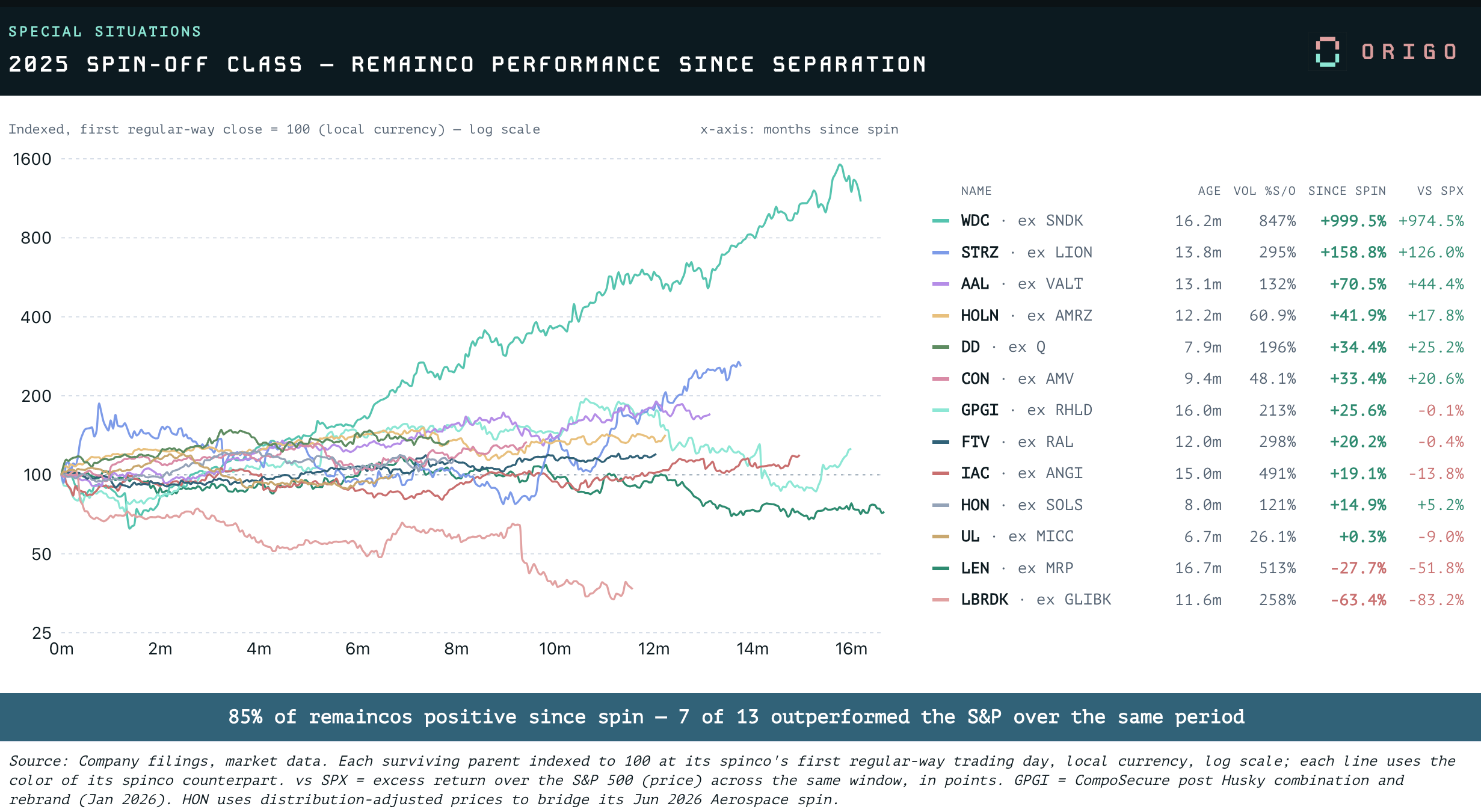

The RemainCo performance was not as bad with a majority (7 of 13) also outperforming the S&P

SpinCos still trounced RemainCos, leading 9 out of 13 pairs in the head to head

SNDK was the clear standout, and its performance alone would have made holding the entire spin-off basket worthwhile over the past 18 months.

Will we ever see anything like it again?

Greenblatt, 30 Years On

You Can Still Be a Stock Market Genius made its spin-off case in 1997 on three legs:

Forced selling (index funds and mandate-constrained holders dumping shares they never asked for)

Neglect (no coverage, no roadshow, no natural buyer on day one)

Incentives (management finally paid on their own stock, with option strikes set at the post-spin lows)

While market structures have certainly evolved (HONA integrating the S&P Index on first print, more flexible mandates) and pure undercovered neglect is rare, it remains true that spin-offs crystallise decision nodes, require analysis and create volatility. They remain a constant source of opportunity but there is no magic trick: you still need to do the work.

As we went through this analysis, one name in the 2026 batch caught our attention which we will write to you about over the coming days.

As always, thank you for your support!

Catch-up on our reports from this week:

Solaria: Valuing this Powered Land Bank Platform in a Grid-Constrained Europe