[Flash] Quick Thoughts on Honeywell Valuation Post Spin-Off

Yesterday Honeywell HON 0.00%↑ completed the spin-off of its Aero Technologies division trading under the new ticker $HONA.

As a reminder the spin-off distributed 1 share of HONA for every 2 shares of HON held at the record date (June 15th). HON simultaneously effected a 1-for-2 reverse stock split.

Yesterday’s closing prices ($220.2 for HONA and 227.8 for HON) equate to a share price of $224 for Honeywell on an ex-ante basis, a slight premium to our purchases in the $208-210 range.

We discussed previously how we did not necessarily expect HONA to initially underperform HON per “traditional” Greenblatt spin-off dynamics and that RemainCo could end up being the more interesting relative opportunity. Interestingly, both tickers sold-off and HON underperformed HONA going into the close.

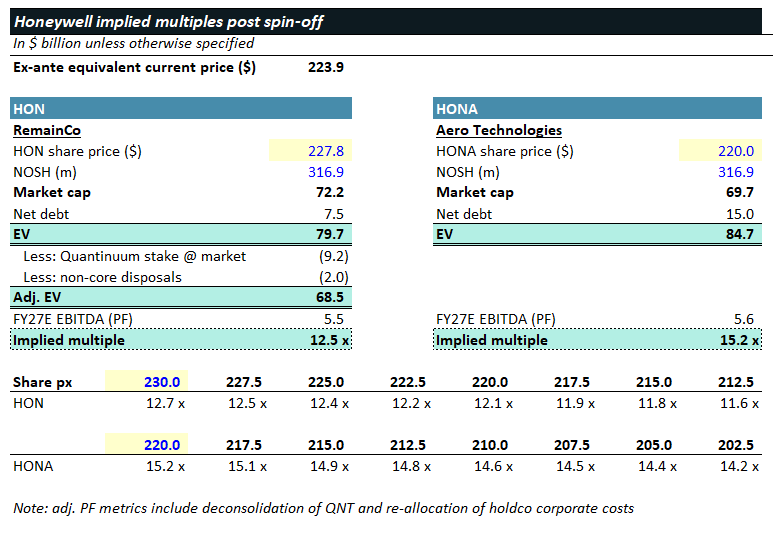

Relative Valuation

We take a look at the implied 27E EBITDA multiples for both HON/HONA post spin-off. This includes adjustments for the deconsolidation of Quantinuum post IPO and re-allocation of Holdco costs.

Based on our numbers, RemainCo is trading at an implied 12.5x 27E EBITDA once you strip out the QNT stake at market (+ non-core disposals) while HONA is trading at an implied 15.2x 27E EBITDA.

We’ve included some sensitivities so that you can monitor the relative attractiveness as the shares trade over the next couple of days. We will post some further thoughts but our initial take is that we would be happy owning both businesses at the current implied valuations and we will be monitoring both HON and HONA for potential incremental buys over the coming days / weeks.