Weekly | HON RemainCo, SPCX on Hyperliquid, New Themes

HON RemainCo

The HONA spin-off is fast approaching (expected June 29th) with investor days lined up on June 3rd (Aero) and June 11th (Automation).

We are curious to observe how HONA and HON will trade relative to each other. While we initiated a position in the consolidated entity ahead of the events, we are keeping powder dry to take advantage of any dislocation.

The classic Greenblatt take would be to assume increased sell-pressure on SpinCo. We think there is a chance it goes the other way:

Institutional mandate constraints have changed

Aero is widely viewed as the crown jewel

As a result it wouldn’t be surprising to see existing holders swap out their RemainCo exposure in addition to sidelined investors bidding up HONA.

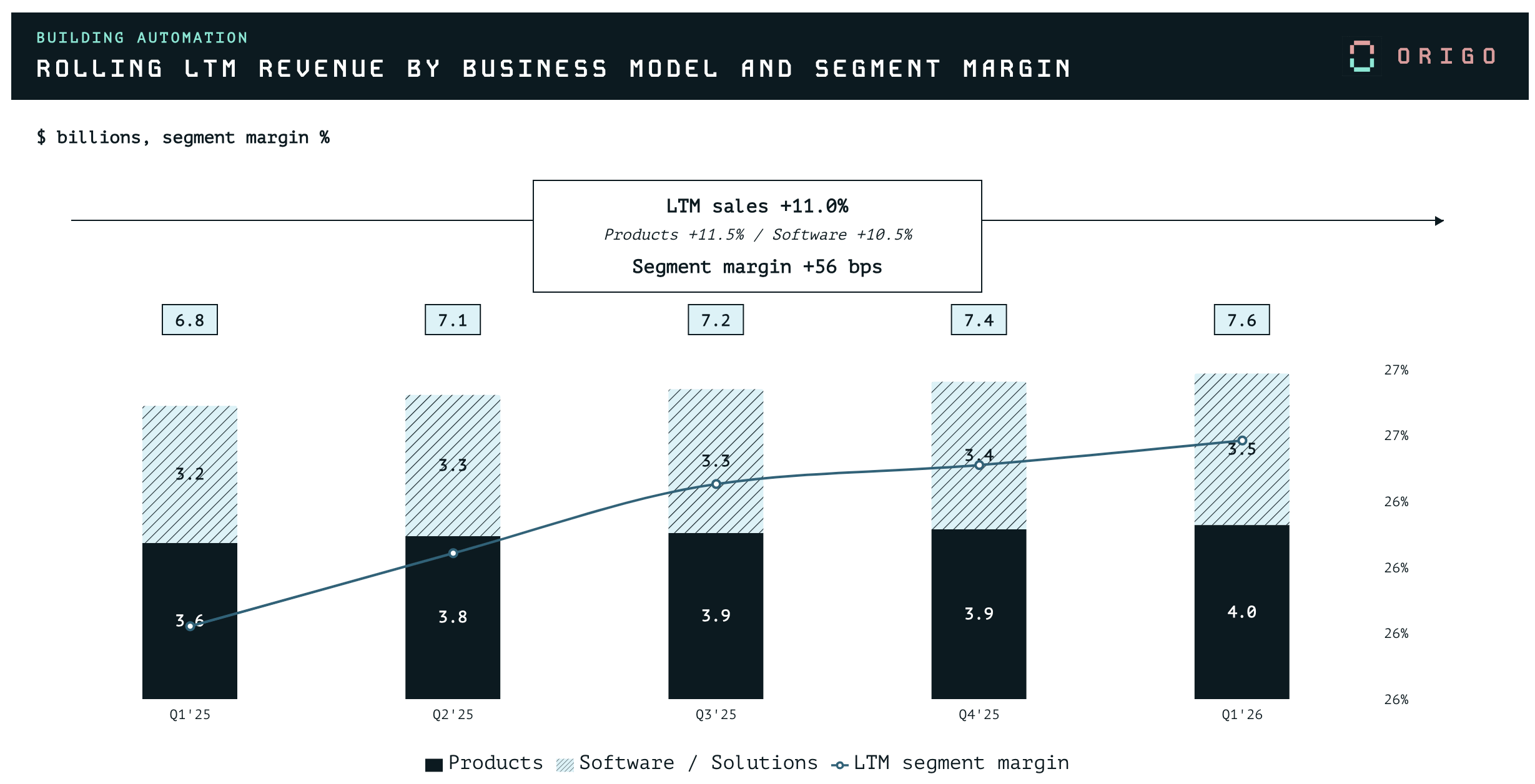

Automation

We think the Automation segment is currently under appreciated relative to the multi-year capex budgets underway in a number of its end-markets and the opportunity for a step-up in installed base / high margin recurring revenue streams.

The most obvious one is in datacenters which is an incrementally growing driver for its Building Automation segment. While this was called out by management as a recent performance driver, information remains limited.

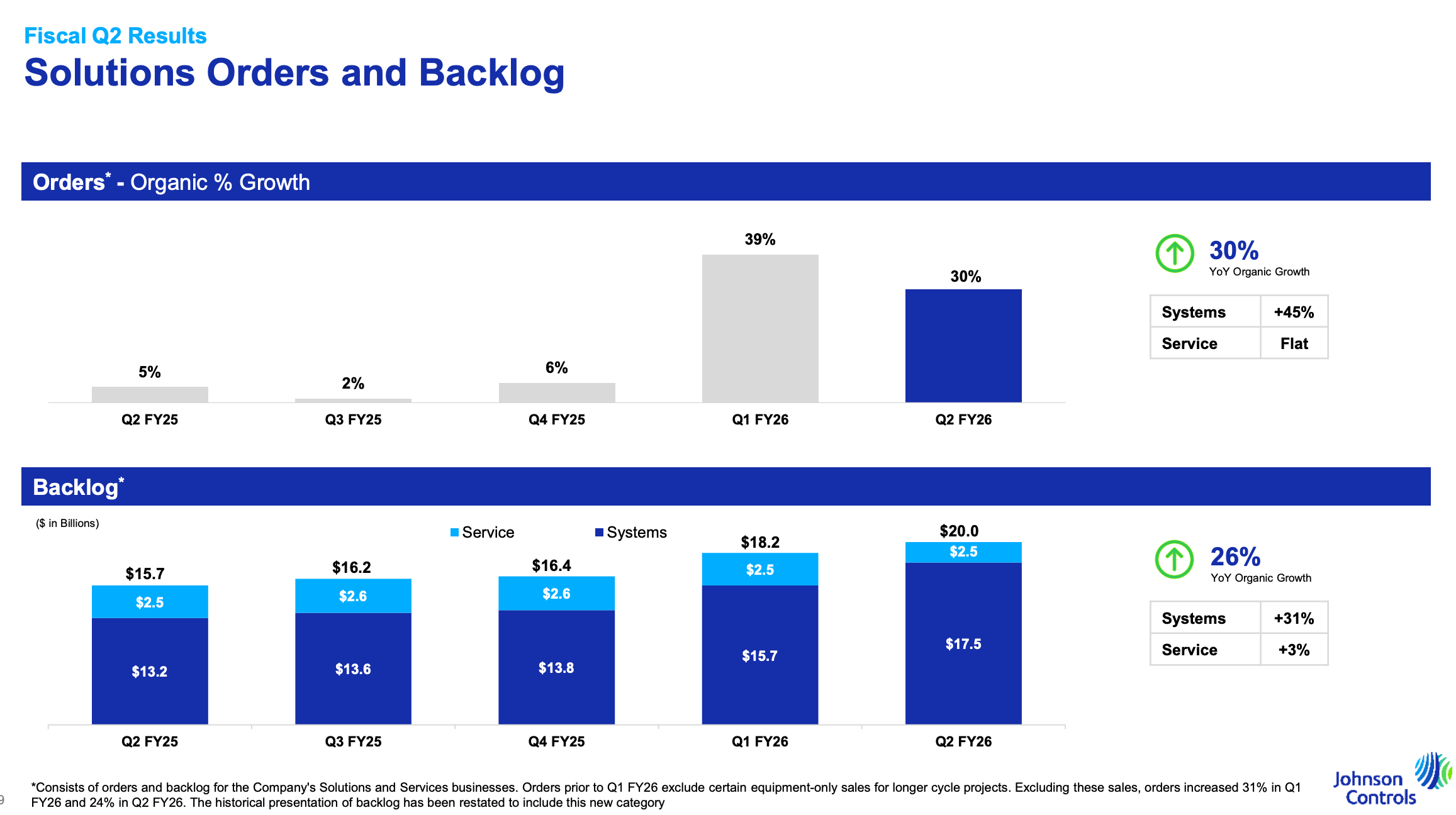

HON should be well positioned to gain incremental market share in the space as power management systems become more complex (hybrid off/on grid solutions, BESS systems, thermal cooling solutions). While not a direct comp (as they also participate in the hardware/cooling stack), Johnson Controls offers an interesting read across with organic orders (+30%) / backlog (+26%) seemingly reaching a major inflection point in its last two quarters.

In addition there are a number of other capex trends which should benefit HON, including its PA&T segment which was temporarily weakened in Q1 due to supply chain / conflict issues (we would note that orders were still up +6%). To cite a few:

$46B of energy infrastructure spend to fix conflict related damages alone, most of which is downstream / LNG related (Rystad)

Energy security: Morgan Stanley estimates Asia will need to spend $5.5T in capex through 2030

Grid / power: close to $6T of grid-related capex required through 2035 (UBS)

Quantinuum

Quantum was in the news this week following the funding grants announcements. We don’t have too much to say here other than an Italian spaghetti sounding company (Rigetti) is +48% of the week and trading at a market cap of $8.8B.

If that’s the case, where should the technological leader in the space be trading?

We will be paying close to attention to the Automation investor day in particular and would be interested buyers of RemainCo on any weakness.

We also uploaded our SOTP this week for paid subs wishing to play around with the assumptions.