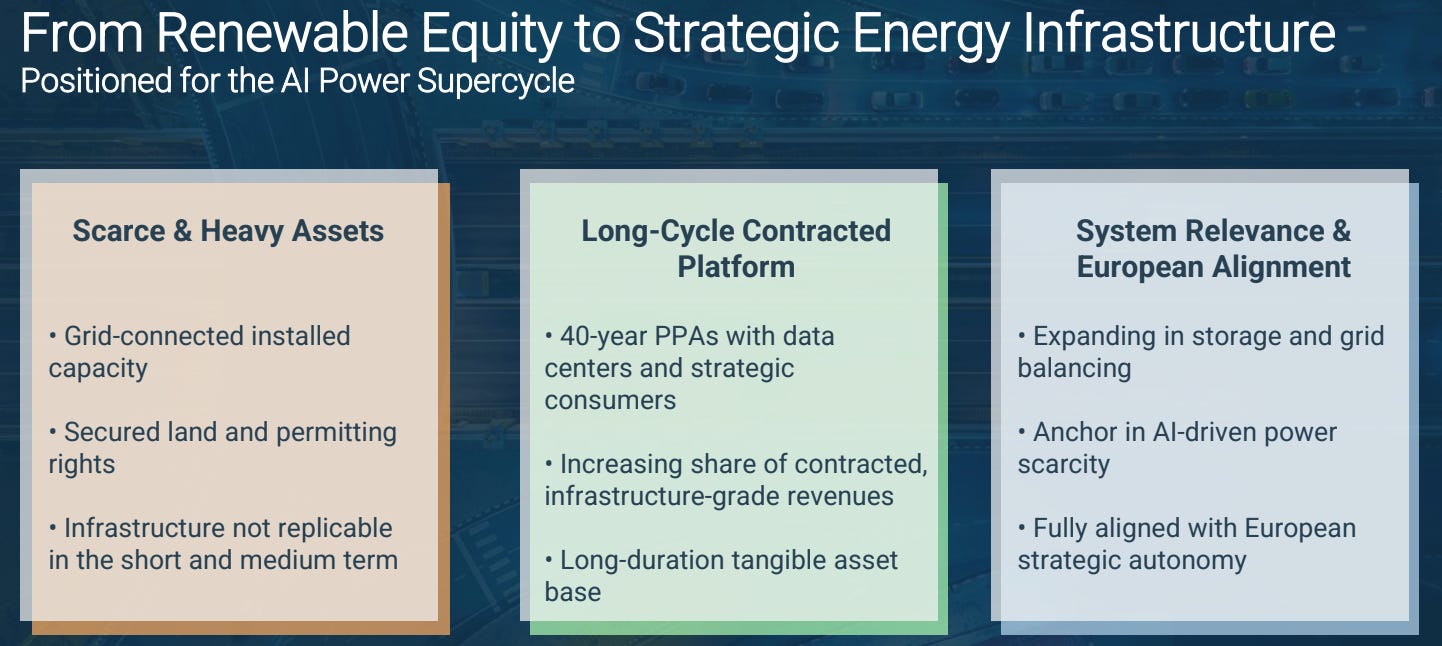

Solaria: Valuing this Powered Land Bank Platform in a Grid-Constrained Europe

Breaking down the valuation drivers as Solaria transitions from price-taking solar developer to energy infrastructure platform selling time-to-power

Start here for background context on Solaria: Grid Wars: License to Connect

With Solaria’s recent pullback, this is an excellent time to revisit our thesis, refine our valuation approach and highlight the key factors we are monitoring.

Solaria continues to transition from a paradigm of weakening solar generation capture prices to a holistic “plug-and-play” DC infrastructure model anchored by improving PPA terms and adjacent high margin income streams.

This creates an interesting push/pull dynamic between the pace of execution on the new strategy vs. negative legacy trends which could be source of recent weakness (we note that spot solar capture prices are particularly weak YTD).

At €19.9/share, Solaria is currently trading at a 17% discount to the April rights issue which was >6x oversubscribed. An interesting spot to consider adding ahead of what should be a catalyst heavy Q3/Q4.

We detail our thought process at the end of the article after walking through all the key valuation drivers and swing factors.

Before getting into the weeds, let’s recap the big picture thesis here:

Spain is emerging as a prime DC hub

FLAP-D markets are grid connection constrained (8 year + queues)

Spain has world class solar resources, cheap land and low population density

Strategically located with subsea cables landing in Spain (low latency gateway between the Americas, and Latin America)

Confirmation: Amazon, Microsoft and others investing heavily in the region

Solaria offers a fully de-risked value proposition to hyperscalers

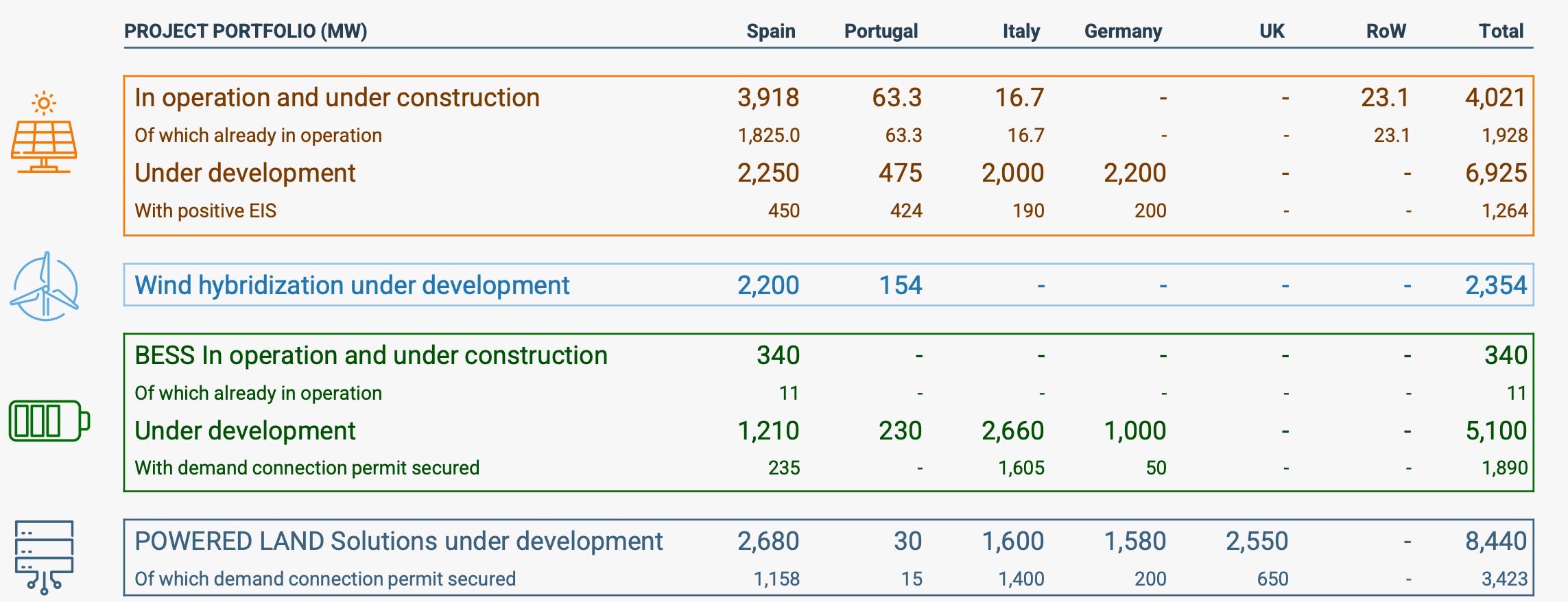

In Spain, Solaria sits on >1 GW of “true” full-service powered land

Existing grid demand connection access as a prime beneficiary of Article 6.9

Land and electrical infrastructure access (1,000 km of private power lines and 100 substations directly adjacent to generation assets)

Ability to bundle long-term renewable energy supply through Solar PPAs

Hybrid BESS for optimised self-consumption + grid fallback

Material savings in distribution charges / electricity tariffs

This bet partially hinges on the management team’s ability to execute on a transformative business plan and we appreciate the fact that we are dealing with an ambitious owner operator with significant skin in the game.

This article is for informational purposes only and does not constitute financial advice. Origo Research may hold positions in the securities discussed.

The Transition Story

Solaria is at an inflection point with an ambitious €2.5B capex program. Management’s goal is to re-rate the business model away from one-dimensional solar generation player → diversified energy infrastructure platform with a higher quality mix of income streams.

This entails leveraging its existing infrastructure both as a monetisation vehicle (selling grid access rights) and as a means to negotiate improved economics.

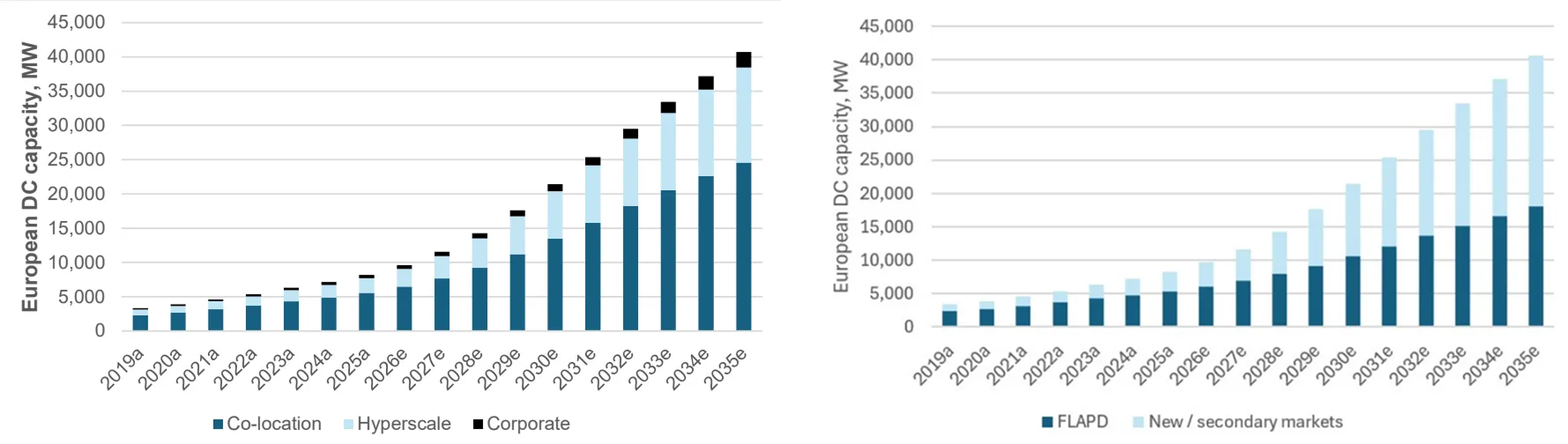

The Pull Factor: Spanish Datacenter Story Taking Shape

Solaria’s capacity straddles both the Madrid region as well as Northern Spain, which Morgan Stanley recently highlighted as a key growth market:

“Northern Spain has emerged as perhaps the most exciting secondary DC market in Europe (along with the North of France).

AWS, Microsoft, Blackstone/QTS and Vantage have all announced large-scale projects in the region […] In terms of our core forecasts for Spain:

Spanish DC capacity (Madrid, North of Spain, other areas) will increase 11x, from ~400 MW (Dec-25) to 4,300 MW (by 2035e)

Our 2035 forecasts for Spain rise by +55%, from 2.8 GW to 4.3 GW;

We believe that the North of Spain can ultimately reach 3 GW of capacity”

While Europe is largely a co-location market today (~75%), Hyperscaler capacity is set to accelerate (notably as they pursue their “Made in Europe” credentials) with new / secondary markets set to disproportionally benefit – chief among them Spain as evidenced by Amazon’s recent €40B commitment to the region:

For Solaria, proof of concept has already been established with the Merlin 1 (225MW) and Merlin 2 (213 MW) deals. Importantly Solaria is selling grid access in conjunction with Solar and BESS PPA terms that are above market.

Merlin is the leading REIT in Iberia and their own DC lease-up performance provides positive read-across to Solaria. Solaria maintains significant optionality with its uncontracted capacity and is in ongoing negotiations with multiple hyperscalers and PropCo platforms.

One question for Solaria is whether they seek to go up the value chain: core & shell or even full-fit. The JVs they have set-up with Stonepeak (Generia LandCo JV) and Stoneshield (Gravyx BESS JV) are indicative of management thinking through the gamut of funding channels and we wouldn’t be surprised to see some differences in how they structure the remaining capacity.

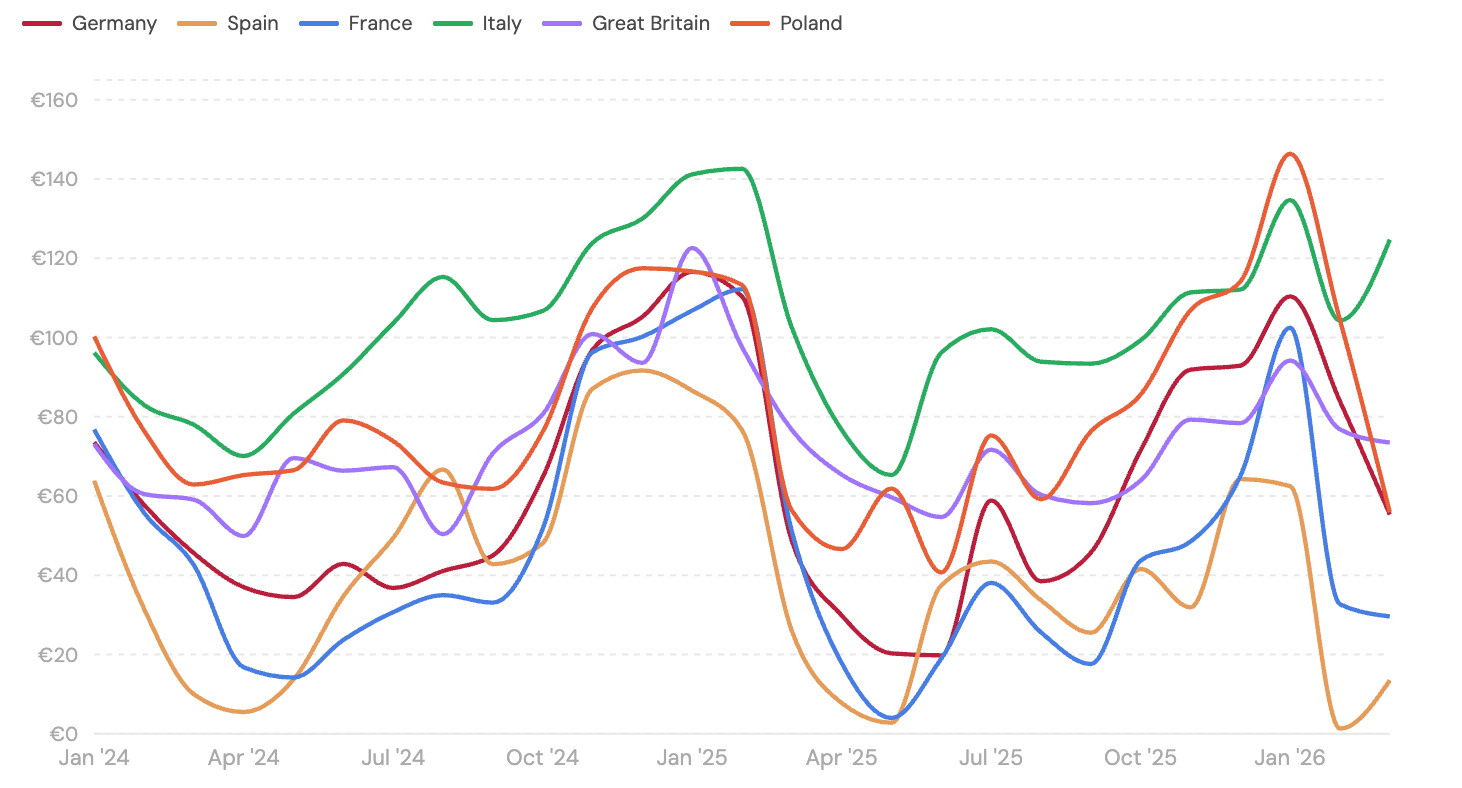

Push Factor: Persistently Weak Solar Capture Prices

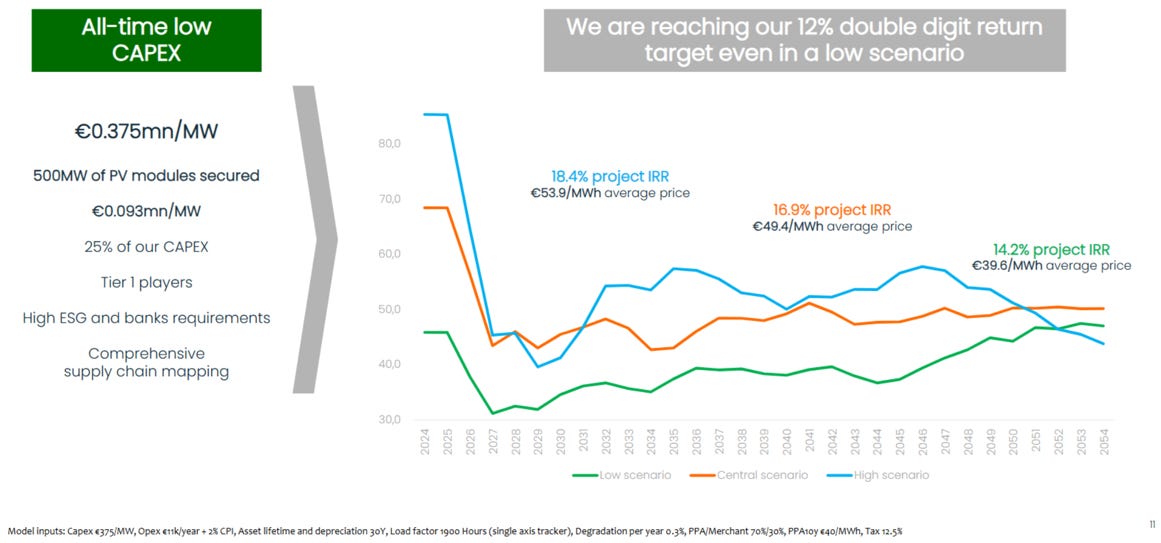

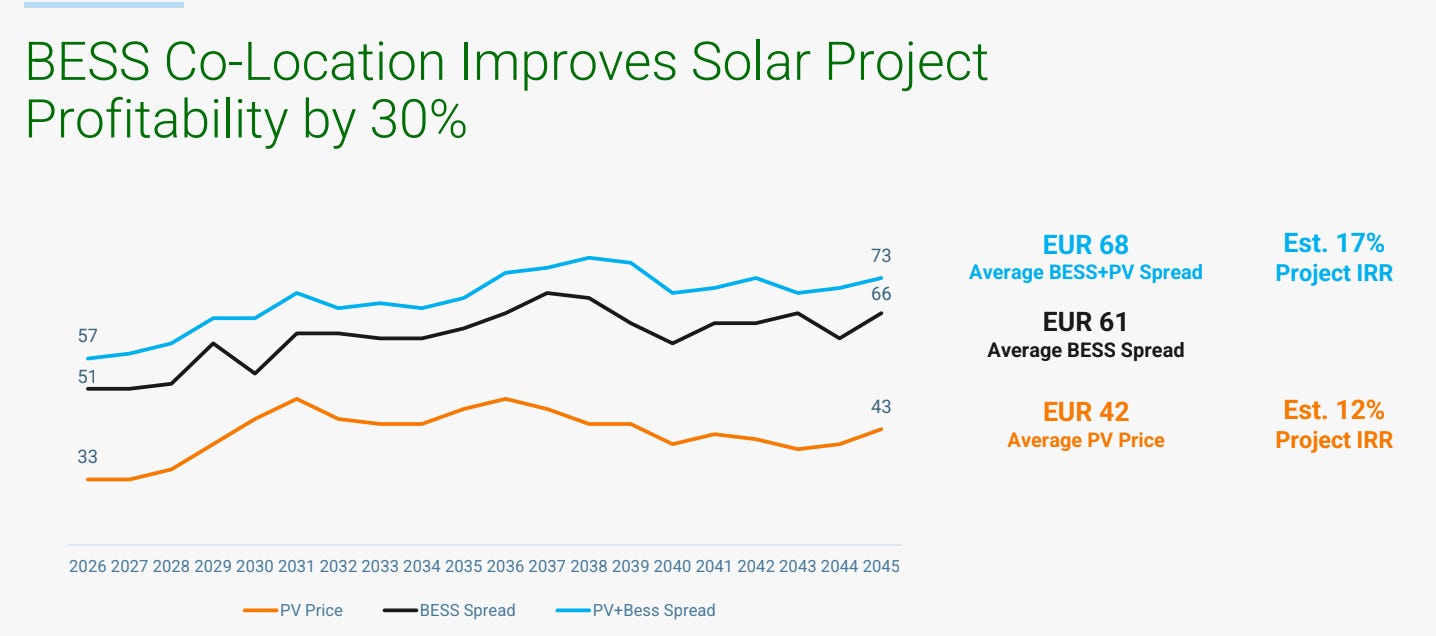

Spanish power prices remain subdued, and solar capture rates continue to decline as the number of negative price hours rises. Unlike in Italy, where the marginal price is set by gas, Spanish solar project economics depend heavily on securing fixed-price PPAs (typically 60–70% of volumes) to limit merchant exposure. Project returns are further supported by falling capex per MW and the increasing use of battery storage (BESS).

In today’s environment, management expects projects to deliver ~14% IRR in a low price scenario with ~250bps impact up or down for every €10/MWh delta. Still reasonable but nothing to write home about.

BESS in Spain is emerging as a potential mitigating factor. The intra-day arbitrage opportunity is particularly pronounced and management is claiming ~3 year paybacks on early BESS installations, with up to 500 bps IRR uplift in project economics:

Overtime, electrification, datacenter demand, hydrogen and improving BESS technology should help stabilise the market. In the meanwhile, the standalone Solar story in Spain remains a hard sell given price and curtailment volatility. This is the key argument for bears but also a source of tension which creates opportunity in the name (as we are perhaps seeing now).

While low capture prices are certainly a drag on in-place capacity, 70% of Solaria’s production remains under long-term contracts.

As management further looks to minimise the exposure we note the following:

Incremental Solar additions in Spain are DC-linked (pricing power)

Solaria is pioneering large-scale BESS including hybrid PPAs

Company is diversifying into wind (better economics) + additional geographies (notably Italy) + JVs across the value chain

Paradoxically low prices only serves Spain’s competitive position as a DC hub. In the US, DC demand was its own catalyst for significantly higher PPA prices – not something we are underwriting at all (nor is it required for the story to work as we will see) but worth keeping in mind.

Solaria Valuation Building Blocks

We can think of Solaria’s value drivers as follows:

Legacy solar generation

Existing + secured capacity coming online

Mix of contracted (regulated or PPA) and merchant cashflow streams (65/35% split)

Remaining useful life: 25-30 years (most capacity was added post 2019)

Powered land bank

Monetisation of land, grid connection capacity and electrical infrastructure

Payment per MW spread over 4-5 years (what we can infer from mgmt.)

Growth strategy

Hybrid BESS / Solar + Wind across multiple geographies

Solar dedicated capacity for datacenters with better PPA terms

€2.5B capex plan funded out of debt (~65%) and equity (€300M rights issue + asset rotation + cashflow)

In the following sections, we break each of these down in detail. We establish a valuation framework that includes base, downside, and upside cases. This allows us to frame the R/R profile from current levels and outline our thinking ahead of potential upcoming catalysts.