Flash | SK Hynix Cubed – Yes, there is another layer

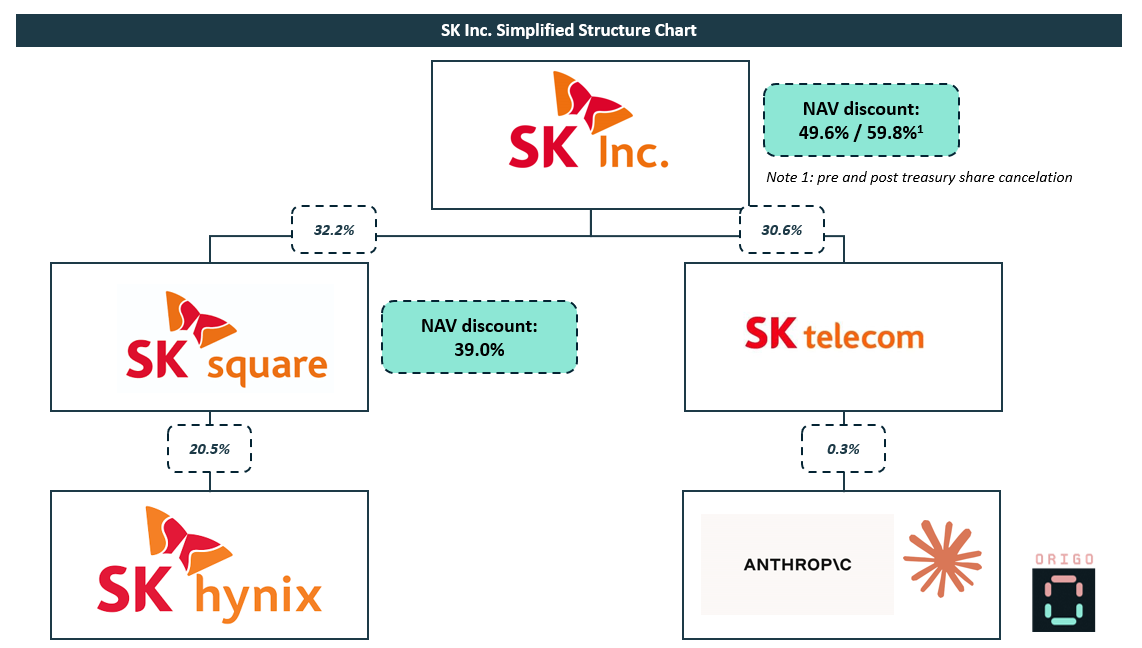

With all the hype currently surrounding SK Square, sharing some quick thoughts alongside the NAV discount breakdown for SK Inc. which is the ultimate holding company with a 32.2% stake in SK Square. (If you are unfamiliar with the thesis on SK Square, you can check-out our original write-up here.)

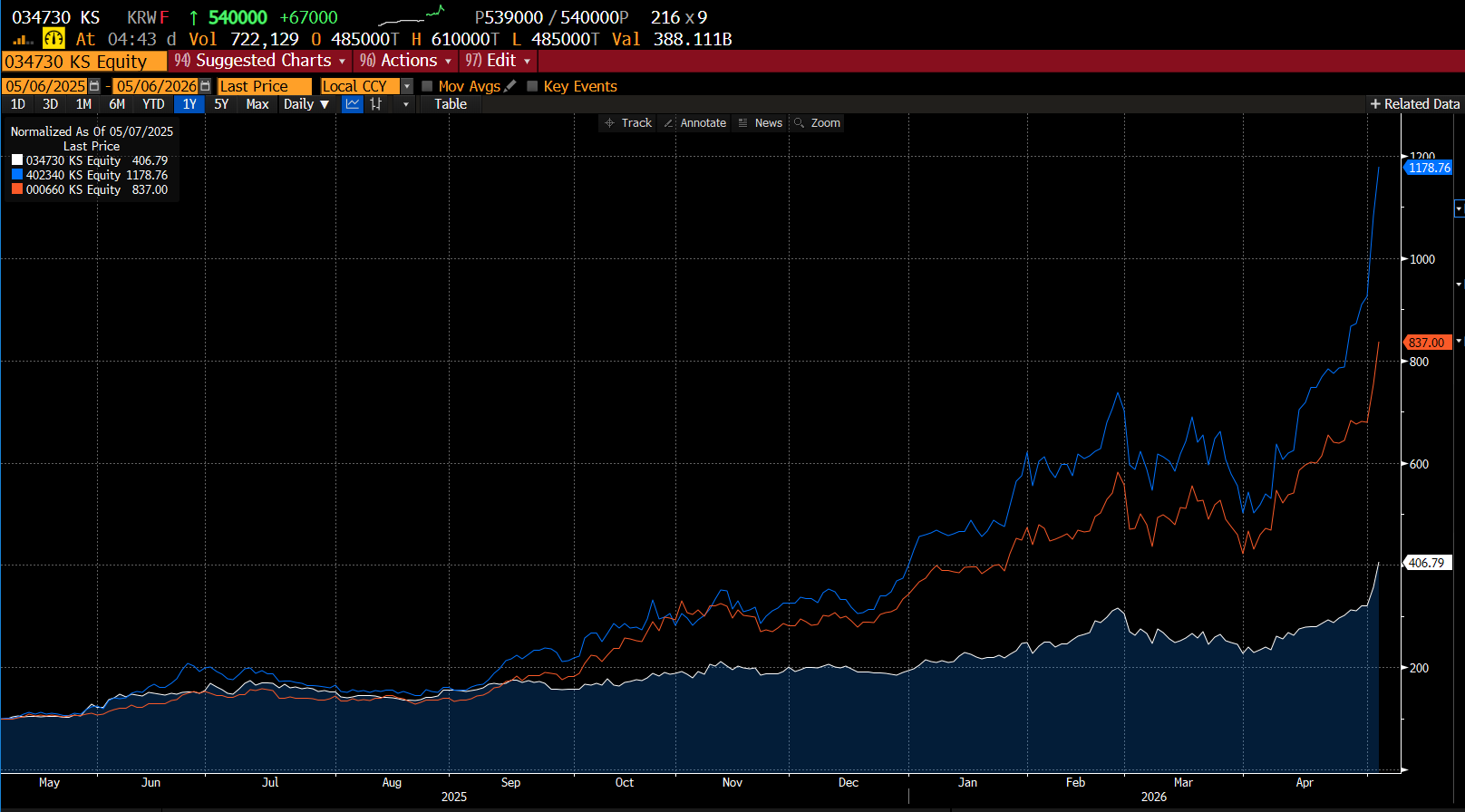

While SK Square has outperformed SK Hynix over the past year, SK Inc. has considerably underperformed (a paltry 4x).

One of the main reasons for this is that SK Square is a quasi-pure play on SK Hynix, since the shares it holds represent 98% of its NAV.

SK Inc is much more diversified: it holds a number of listed stakes, as well as other private subsidiaries and operating companies.

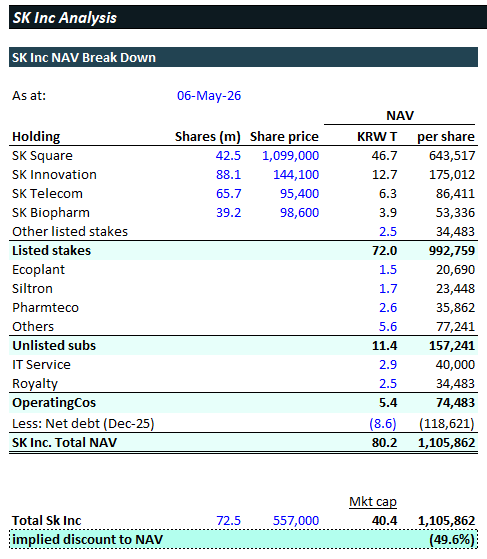

As a result, SK Square only represents 53% of SK Inc’s NAV. Note that this has been steadily increasing, in part due to the rise in share price but also thanks to divestments / streamlining the Board has been engaging in as part of its “value-up” initiatives.

Since the discount to NAV for SK Inc is now much wider than that of SK Square and currently sits at 49.6% (vs. 39.0% for SK Square at the time of writing) it is reasonable to ask whether a catch-up trade is in order.

Here is the full NAV breakdown and portfolio composition of SK Inc:

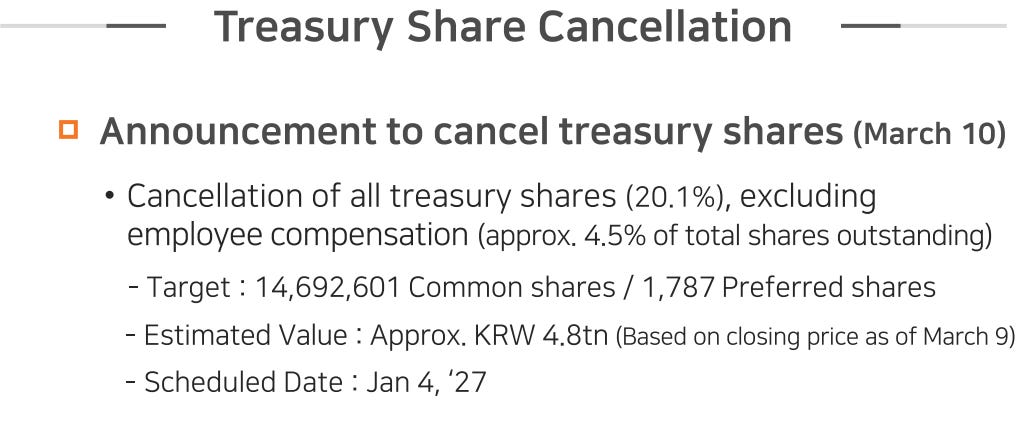

Note that this calculation is on the basis of the current shares outstanding. SK Inc has already announced that they will be cancelling all the treasury shares (~20%), which once effected further increases the discount to 60%.

While the NAV discount is clearly attractive, the analysis is a bit more complex since it also requires a view on the remaining 47% of NAV composition.

One point of note is that SK Inc. indirectly owns a stake in Anthropic via its 30.6% holding in SK Telecom who invested $100m back in 2023 in the $5B valuation round.

Additionally, its second largest holding SK Innovation is currently benefiting form an uptick in crack spreads and refining margins as a result of the Iran Crisis – although the medium to longer term outlook on the overall business here is more uncertain.

We will be writing a follow-up post with more detailed thoughts on the rest of the portfolio and how we might be thinking about this name going forward.

I've been doing a bit of digging on these Korean HoldCo situations. I think one big variable that is missing from the analysis is tax. The tax rate on cap gains is ~26% apparently. With SK Square, they purchased their stake in SK Hynix back in 2012 I think. So that has a huge unrealized loss that would lead to a sizable tax bill if they ever sold and monetized their investment.

Even if you don't think they will sell the stake imminently, I still think it makes sense to include some deduction for the associated tax liability. I just don't think investors are going to ignore the tax, so they will never bid this to 0% discount when they can just buy SK Hynix on the open market with no associated tax liability.