Flash | PayPal 3.25% 2050s: Put Option in Play

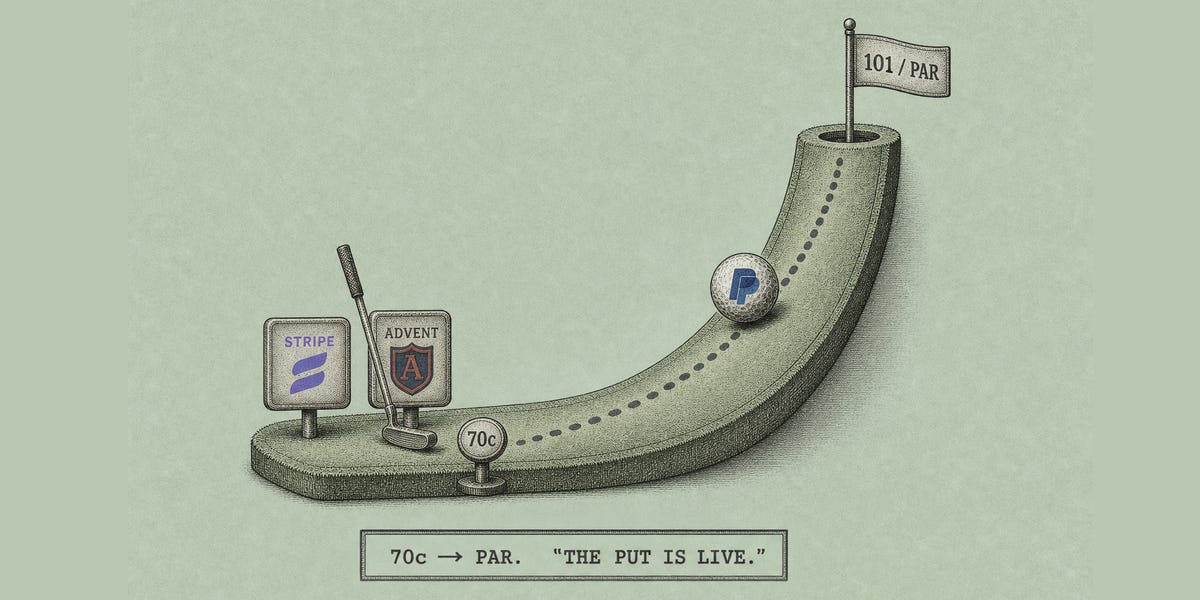

Advent and Stripe made an offer to acquire PayPal. Will the CoC put get triggered and could bondholders even end up outperforming the common?

Asymmetry through credit set-ups are some of our favourite trades.

Back in February we wrote a piece titled: Equity-like returns on a A- rated bond?

The idea was to see if we could build a basket of IG bonds with a splash of upside convexity: park cash at >6% YTM with the added optionality of a 50% move.

For this, we were specifically screening through ZIRP era bonds with the following characteristics:

Long-duration and low coupon = low dollar price (<75c)

CoC (change of control) put triggers (obligation for sponsor to buyback at par)

M&A activity was picking up, and we had just witnessed the largest LBO take-private in history (Electronic Arts) signifying (i) a potential uptick of additional CoC clauses getting triggered in the short to medium-term and (ii) an expanded target universe, where >$30B market caps were no longer off the table.

In the case of EA, despite the defeasance shenanigans, the 2051s re-priced from 60c to 80c (with an extended interim period at 95c).

Two names jumped out to us in our screen: the eBay 2051s and the PayPal 2050s.

We already discussed eBay in detail during the GME saga.

Yesterday, it was reported that PE firm Advent, along with Stripe, had made an offer to acquire PayPal. This sparked an 8pt move in the 2050 bonds:

Despite cooling-off since1, the possibility of a par take-out is very much in play, and we wanted to share some preliminary thoughts on the situation.

A game of probabilities with nuance around execution risk, pro-forma capital structures, incentives and indenture language — let’s take a look.

Note 1: 67c unlikely real price, latest runs we have seen closer to 70.4 / 71.4