Weekly | Got Tankers? (Iran Edition)

+ Updates on EchoStar and Nordic Semiconductor

Tankers: asymmetry playing out

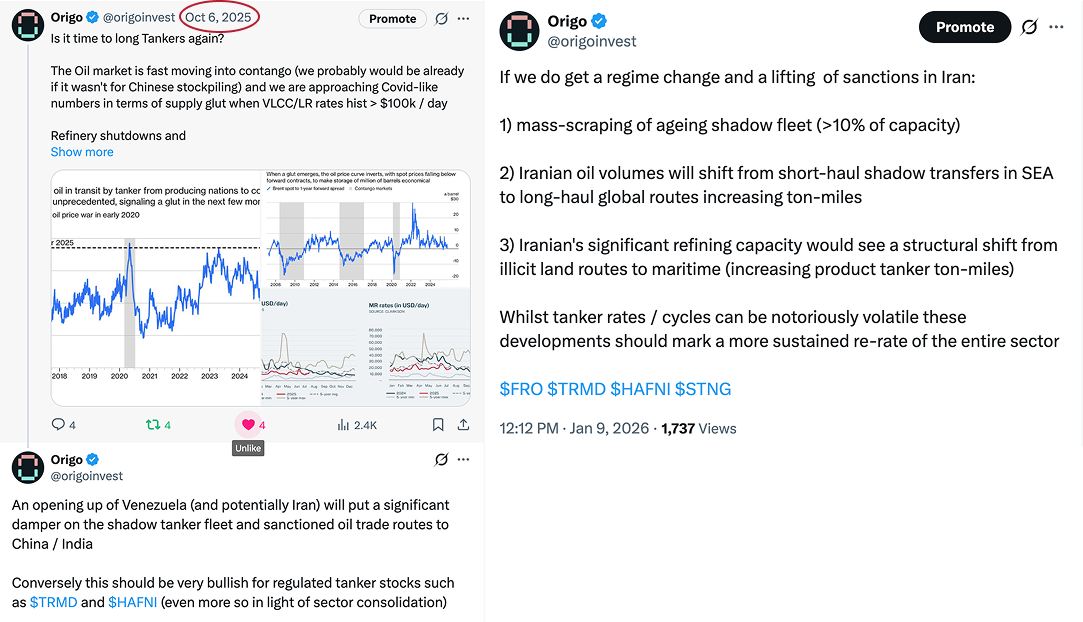

If you follow us on X you will know that we have advocated being long tankers since around October last year. Our thesis was anchored in improving fundamentals with the added asymmetric overlay that the sector stood to be a major beneficiary of continued geopolitical tension (and in particular ongoing developments in Venezuela / Iran).

Shipping is notoriously volatile and prone to boom and bust capital cycles due to (i) a primarily spot-based charter market and (ii) fragmented supply (shipyards) with a delayed 2-3 year newbuild cycle.

The two key drivers to look out for in the space are:

Ton-miles (distance covered)

Fleet supply (newbuild orderbook vs. scrapping)

The past decade has seen an increase in ton-miles for both crude carriers and product tankers as a result of rising long-haul flows and refinery closures. More recently concerns over a near-term oil glut has also helped shift the oil curve into contango thus incentivising demand from floating storage.

On the supply-side we are coming off a historically weak orderbook which has been offset by the development of the shadow fleet. These are non-compliant tankers being operated past their useful life of ~20 years and transporting sanctioned crude and refined products. The shadow fleet represents a very significant ~20% of the total fleet and the recent crackdown over the past few months has helped accelerate scrapping of these older vessels.

Prior to the Iran news, these developments have been playing out nicely. VLCC rates have skyrocketed past $100k / day and in 2026 we are so far operating at levels 2-4x the historical average over the past decade (!)

The names we have been tracking (Frontline, Scorpio Tankers, Hafnia, Torm) are all up 30-70% since October as at Friday close.

We impatiently wait for the Monday open to see the market reaction to the news. Whilst we believe a closure of the Strait of Hormuz (>30% of oil throughput) remains unlikely, the Iran news is unequivocally positive for the sector.

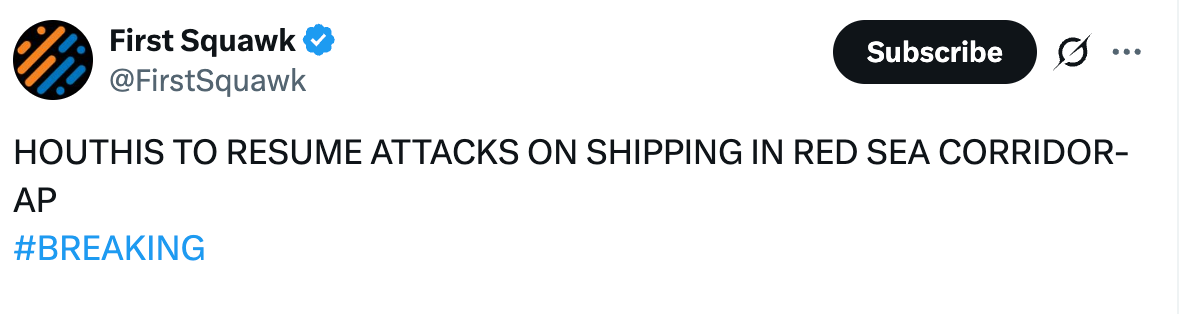

In the immediate term we will see re-routing, insurance premiums rise (or straight out cancelled) and perhaps an increase long-term charters as operators seek to secure supply. The Houthis have already resumed attacks on the Red Sea corridor which will drive product tanker rates higher as well.

In the medium term any regime-change will accelerate mass-scrapping of the shadow fleet and we will see further structural shifts in long-haul routes and refinery flows.

If the Strait of Hormuz were to be compromised even temporarily the spike in rates would be absolutely unprecedented

What do we do from here? We think an Iranian regime change does warrant a fundamental re-rate of the sector. We are also aware that current charter rates are planting the seeds for increased overbooks and will become increasingly cautious as things pick-up.

If you have been involved in this trade over the past 2-3 months, congrats.

We think trimming up to 50% into next weeks price action depending on the strength of the move is justified.

EchoStar ramping up

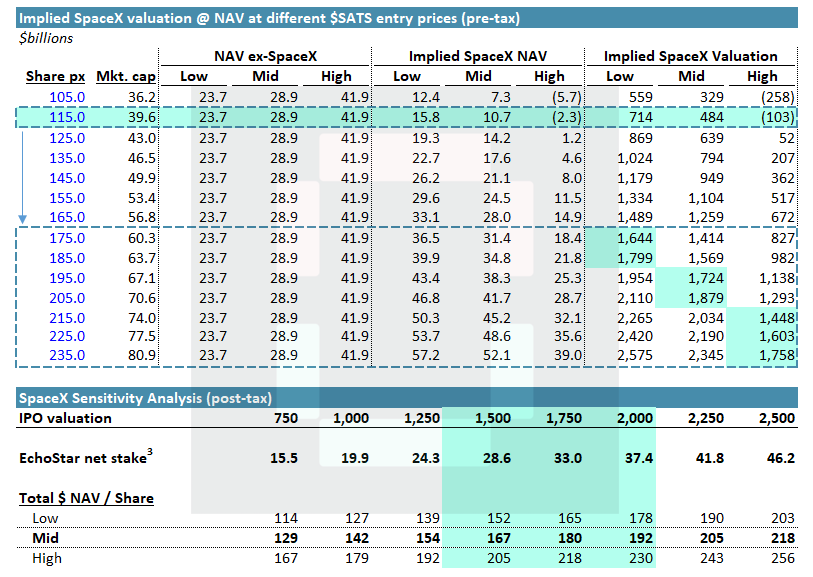

Bloomberg reported on Friday that SpaceX is looking to file for an IPO in the coming weeks, which keeps them on track for a June listing. Very much looking forward to getting our hands on the S-1! On a red day in the market SATS delivered a +10% intraday reversal on the news. Hopefully some of you managed to accumulate under $110 / share beforehand.

Bloomberg also reported a valuation target of $1.75T and we’ve updated the tables below to show what that that would look like.

We thing a $175-230/share range should be in play over the coming months.

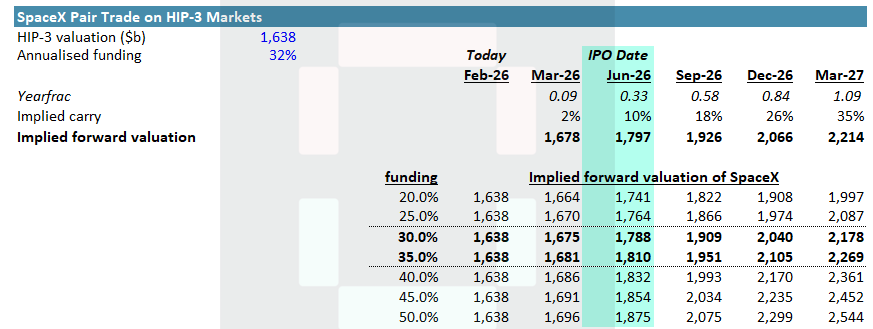

As a point of reference SpaceX is now trading at a $1.64T valuation on Hyperliquid HIP-3 markets with annualised funding hovering around ~32% (in other words an implied forward valuation of ~$1.8T on a June IPO.

EchoStar will also be reporting earnings this coming week and we will be posting on our updated NAV ex-SpaceX views if there is anything material.

Nordic Semiconductor: the long game

Some anecdotal evidence over the past 1-2 weeks confirming to us that Nordic’s nRF9151 chip is well positioned to be the leading player in long-range low power IoT.

Firstly, Deutsche Telekom just launched the world's first multi-orbit IOT roaming (seamless coverage across cellular, LEO and GEO) using Nordic Semiconductor’s nRF9151 chip. As a reminder this is the first 3GPP-compliant cellular IoT module to support terrestrial NB-IoT/LTE-M as well as NB-NTN over GEO and LEO.

Additionally there was panel with META sparking speculation that Nordic’s long-range cellular solutions will have a role in future AI glasses architecture.

Nordic Semiconductor is a long-term hold for us. Its long-range segment only represents <10% of Nordic Semiconductor’s business today and we expect the stock to re-rate as their TAM within the space-enabled economy becomes clearer to everybody.

In the meantime, we continue to take downside protection comfort from the recent M&A of their closest competitor at levels implying a 3x from Nordic’s current share price.

Can you speak more to the structure of the SATS deal with SpaceX? I understand that the actual closing of the sale and transfer of the majority of the SpaceX shares to SATS won't happen until November 2027. I assume SATS can't actually recognize the shares on its book until that happens. How are you discounting that, if at all?

🫡