Weekly | The $MSTR Layer Cake, $SATS Spectrum Auction 113 Read-Across

Michael Saylor went on record this week talking about how he designed STRC using AI. We can picture the prompt:

“Help me structure an instrument that can be widely marketed to retail. Like, high passive income but also liquid and redeemable at par anytime. Very important though: no obligations for Strategy. In fact, we never want to be in a situation where we are forced to make any payment. Perpetual sounds good. I also like the idea of adjustable and deferrable dividends. Make no mistakes.”

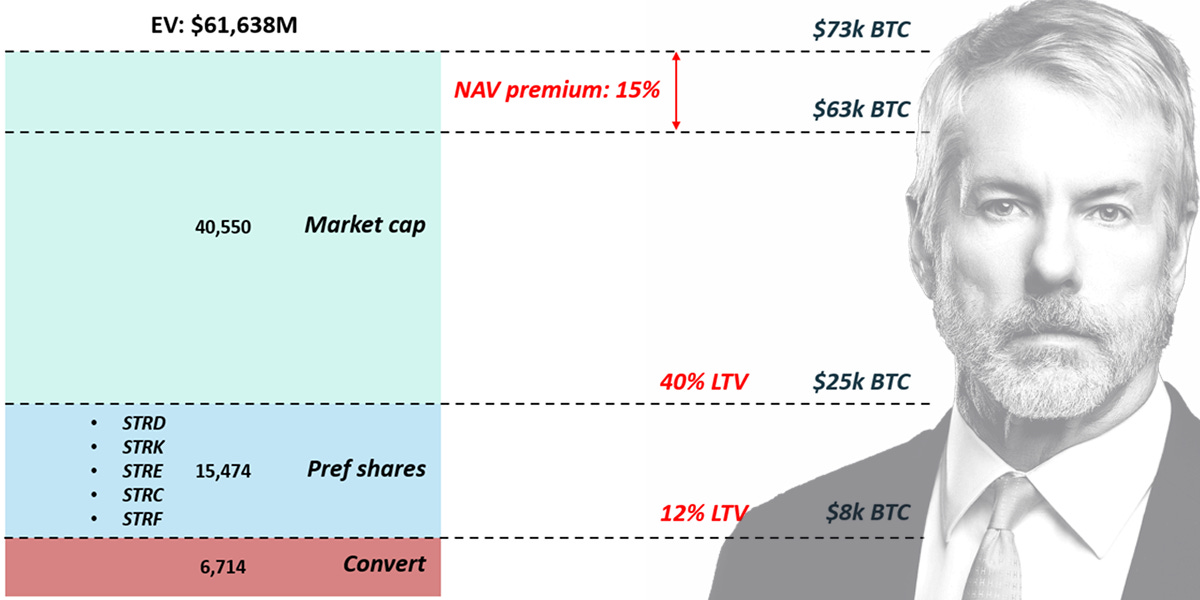

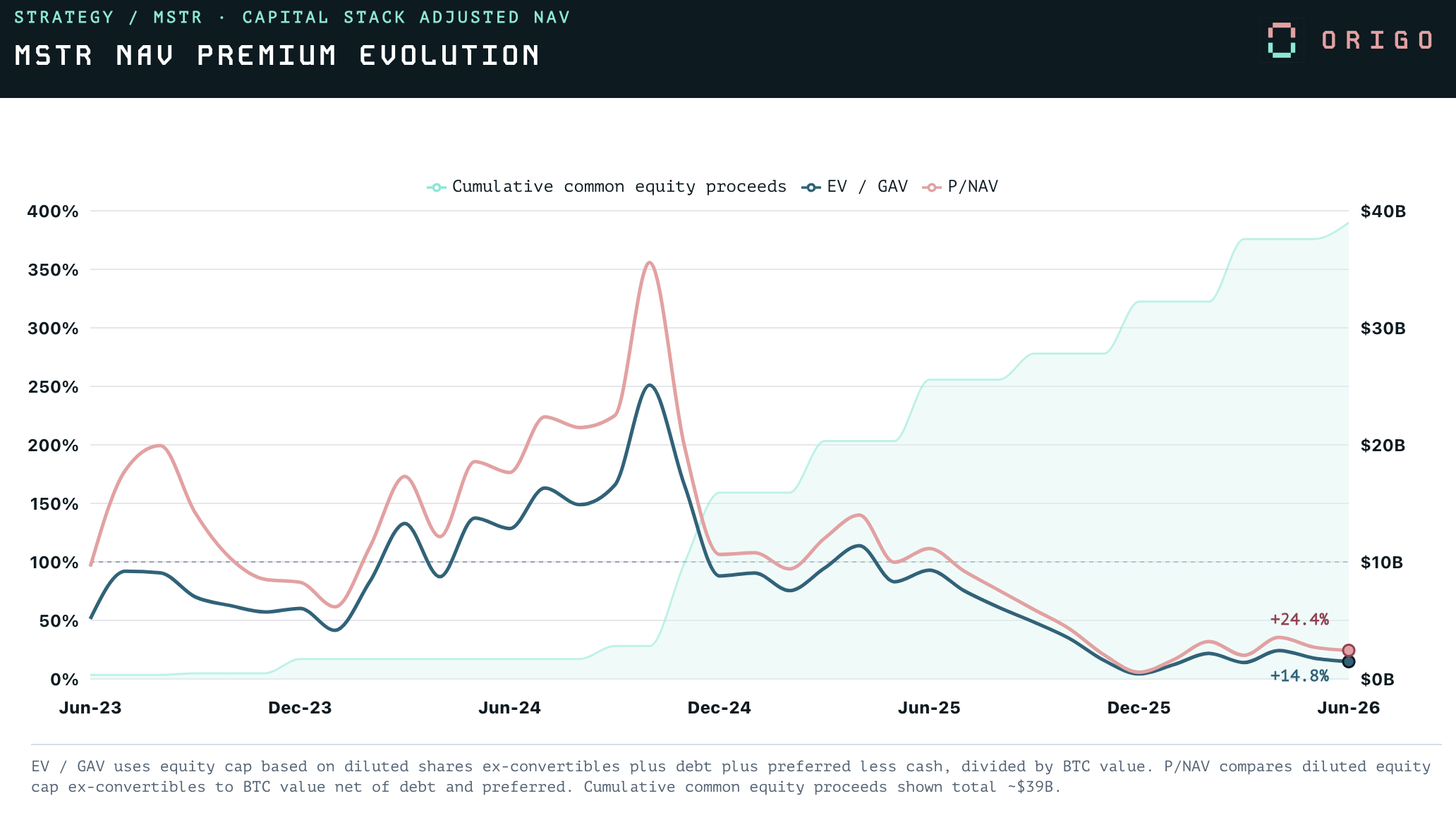

Strategy has been on a $60B bitcoin buying spree over the past 3 years funded through common stock ATM offerings (exploiting the NAV premium) and turbocharged by a layer cake of structured instruments.

This started out in the convertible debt space, servicing hedge fund arb desks. As realised volatility compressed and inflows diminished, Saylor needed a more consistent source of demand – retail being the obvious white space which he sought to entice with elevated headline dividends.

Strategy has now issued $15B in pref shares. This truly accelerated with the creation of STRC and the concept of a pref share being “pegged to par” through a variable rate adjustment mechanism.

The STRC chart took an interesting turn this week:

Saylor has no brakes. He will raise as much capital as the market will give him.

The more proceeds raised through STRC, the riskier STRC becomes in a downside scenario.

Saylor was probably counting on sparking a bitcoin rally through positive reflexivity as traders sought to front-run elevated STRC demand.

For a short while this looked like it might work. Now, BTC has dropped back down to $63k.

Where does this leave Strategy today?

In our view, the STRC “de-peg” is a red-herring and is only relevant in the sense that it temporarily closes access to this funding channel.

If BTC recovers within the next 1-3 years, then no issues.

If BTC goes sideways / trends lower, Strategy has a real funding gap to deal with which may be exacerbated through negative reflexivity.

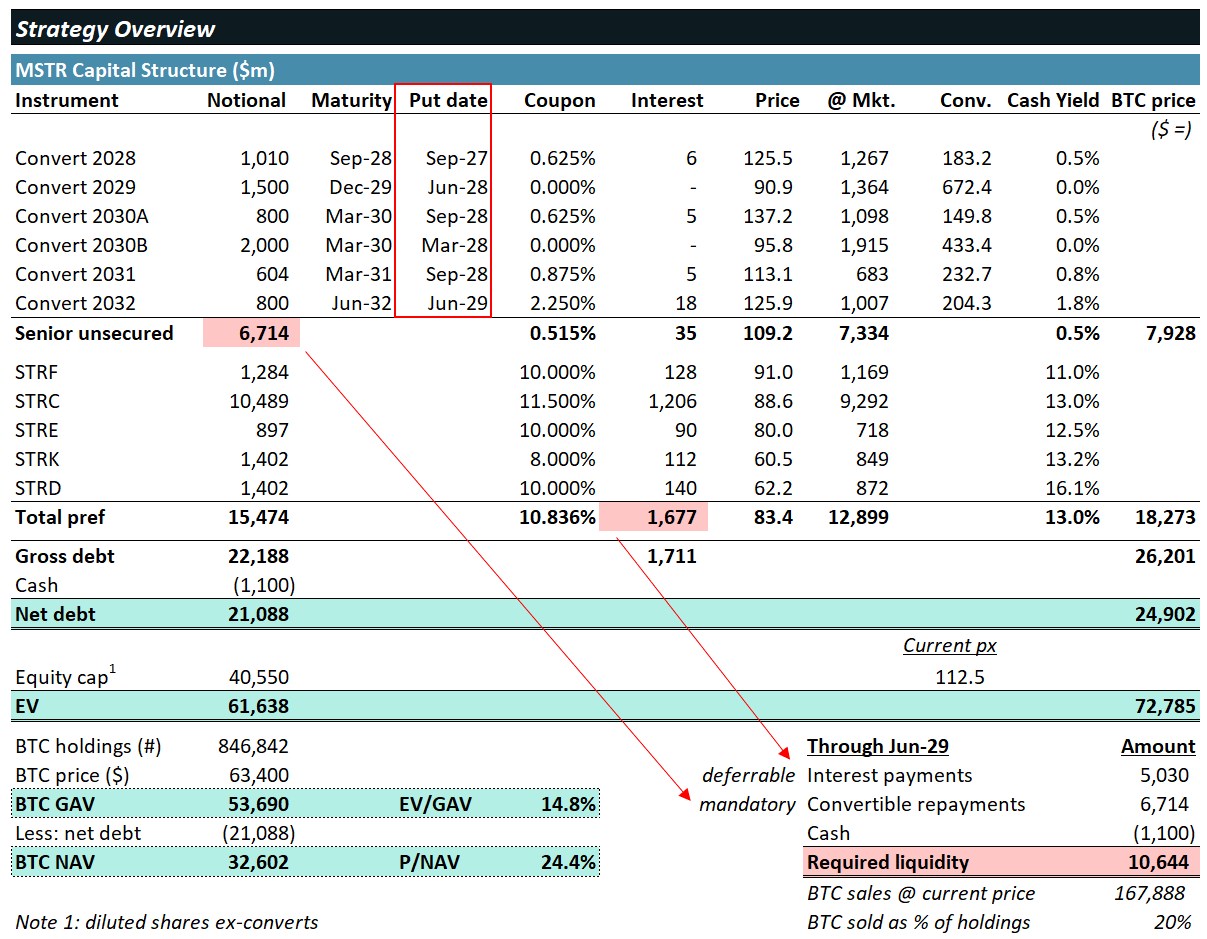

Strategy’s $11B Funding Gap

Saylor has a $11B liquidity shortfall to address over the coming 36 months.

At current Bitcoin prices, the $6.7B convertible debt stack is deeply OTM. These are all puttable through June 2029.

Strategy also has to fund $5.0B in preferred dividends over that timeframe (assuming they don’t decide to play hardball, which is an option).

On the asset side, the Company holds 847k BTC and $1.1B of cash reserves. The FCF from the software business is now insignificant.

Strategy Capital Structure:

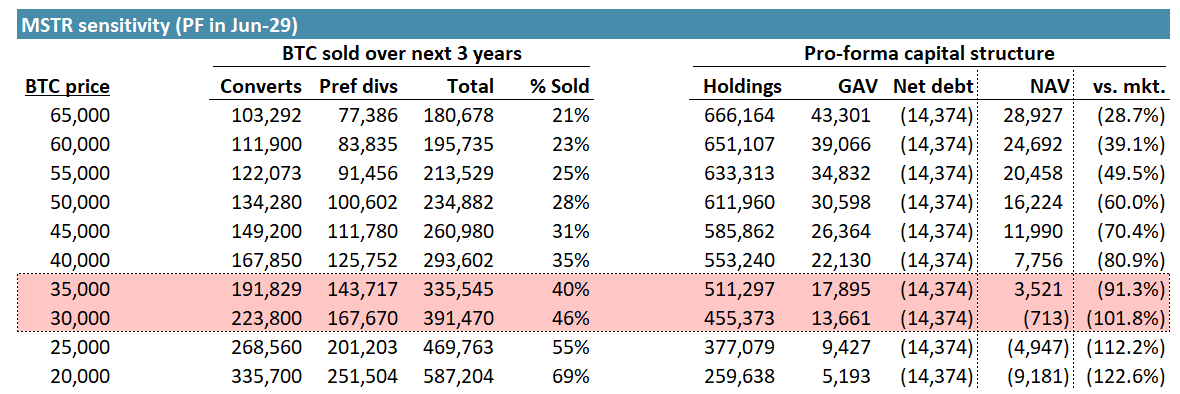

$11B equals 20% of its BTC stack at current levels. Of course, the lower BTC goes the higher % he has to sell to meet the same $ requirement:

28% @ $50k

35% @ $40k

46% @ $30k

While $25k per BTC is the level at which equity NAV is a zero today, that level widens if they are forced to selldown BTC at lower levels.

Pro-Forma Capital Structure: 3 years from now

We can take a look at what the pro-forma capital structure looks like in 3 years time assuming the BTC price trends lower and stays there:

if BTC remains at the $30-35k mark for an extended period of time this would destroy almost all equity value.

Of course, this is a worst case scenario where (i) BTC stays in a prolonged downturn and (ii) Saylor does nothing about it.

Let’s remember – Saylor’s incentives are aligned to the MSTR common. MSTR first, BTC second, STRC a distant third.

Michael Saylor’s Options:

Firstly, the most obvious source of funding would be through continued ATM common offerings. This is becoming a more dilutive proposition by the day however as the NAV premium compresses:

Secondly, Saylor could decide to play hardball with the pref stack. The Board has discretion to gradually lower the dividend (SOFR floor) and indefinitely defer any payment. He could do this until BTC recovers and / or use this leverage to renegotiate better terms. There are many permutations here:

Any dividend deferral would tank the STRC price

Could seek to crystallise the discount (open market or exchange offering)

Implement a BTC linked dividend and / or swap for equity upside share

Thirdly, Saylor has options to push back the convertible debt payments and further extend his runway. Currently, the debt stack is unsecured with weak protections. Even if BTC were to hit $40k he should be able to raise secured debt to refinance out the $6.7B of converts (~20% LTV). This would heavily compromise Strategy’s flexibility going forward however and would likely only be a measure of last resort.

In Summary:

Saylor has enough tools in the toolkit to withstand a cycle downturn and avoid being a “forced seller”

While a liquidation-style scenario is not on the cards, MSTR equity value could easily decline 50-80% from here if NAV premium evaporates and BTC flatlines at $50k

Dilution and compromises would limit any future flexibility

Perhaps the most important takeaway is that it will be difficult for Saylor to raise capital beyond the current funding gap for incremental BTC purchases.

This means that the $60B of buying pressure we had from Strategy over the past 3 years will no longer be there – which increases the probability of a downside case (???)

FCC 113 AWS-3 Spectrum Auction + Implications for SATS

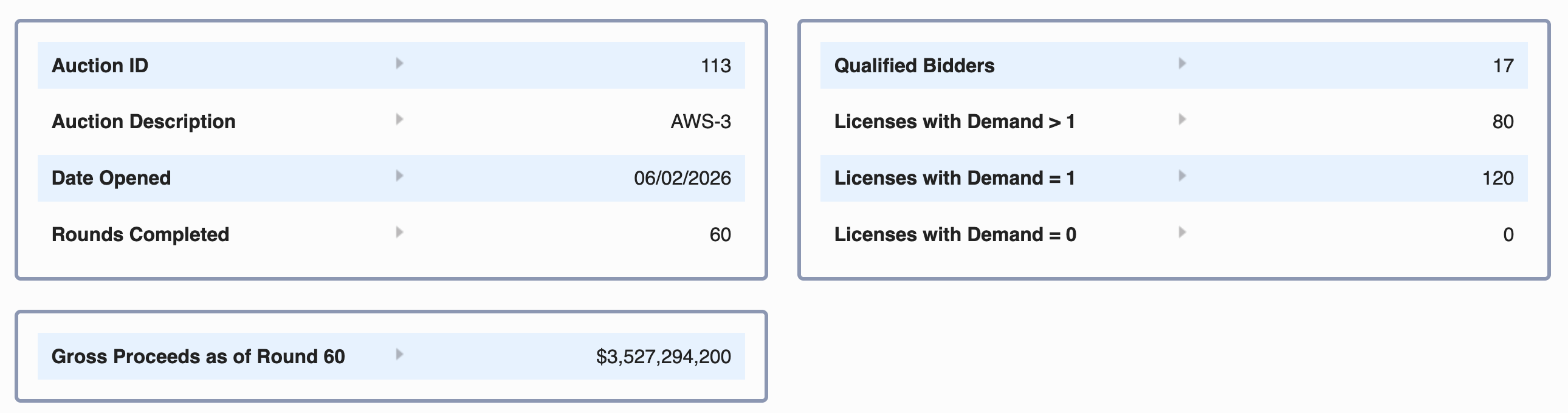

This week we reached Round 60 in the FCC’s re-auction of AWS-3 spectrum (originally won by EchoStar related entities in 2014) which began on June 2.

Auction 113 involves 200 licenses in the 1695-1710 MHz, 1755-1780 MHz, and 2155-2180 MHz bands and uses an ascending clock format, with one license available in each market/category combination.

There are two reasons why this is important to SATS:

EchoStar is subject to a contingent liability if the auction does not clear $2.9B

EchoStar has remaining unsold spectrum on balance sheet (including comparable / higher value paired AWS-3 licenses)

As it stands, the auction has already cleared $3.5B in gross proceeds:

while bidding for 80 licenses is still ongoing, we are nearing the end ($3.35B of value across 120 stopped licenses, including all the major markets).

If the auction were to stop here, this would already mean that EchoStar is no longer subject to any contingent liability.

In addition, we think the current $2.49 MHz-pop result puts a floor on the value of EchoStar’s remaining unsold spectrum and that the $8.6B of remaining value we have been assuming is conservative.

While the remaining AWS-3 spectrum is G-heavy, it forms part of a larger contiguous portfolio (rather than disconnected items) and there are very few near-term opportunities to buy licensed mid-band at scale. Verizon is the natural buyer here and have been rumoured $2-3B higher vs. our current assumptions. We also likely overly conservative on the 700 MHz lower-band as well and would expect to be surprised to the upside.

While all the attention on SATS is as a proxy to SPCX, we increasingly believe near-term catalysts will come from SATS simply outperforming incredibly low-expectations on the non-SPCX related portion of its NAV.

From Origo on Twitter:

"Michael Saylor's incentives are pretty clear?

• Owns 19.6m shares of $MSTR common worth $2.2B

• Personally holds 17.8k BTC worth $1.2B

• Zero $STRC

Maintaining funding channels and capital markets optionality has value but if push comes to shove his allegiance is obvious.

This includes deferring the $STRC interest, tanking the $ price and forcing a coercive exchange to crystallise the discount for the benefit of the common."

I have seen a few of these takes, but I don't follow the logic?

Right now he can issue 3-5% of market cap and provide cash runway for interest+divs into 2028. This is a very modest cost to keep everything on track and buy time for a crypto recovery.

Instead of this path, you think he will tank the prefs, and close off MSTR from capital markets? He might do this, but it seems super risky for his ability to control MSTR.

I think you are right that the prefs would initially tank given the poorly informed, largely retail holder base. But doesn't that churn the holder base from unorganized retail into organized distressed debt hedge funds who start getting Board seats after 4 missed pmts? Surely credit funds would be attracted to >20% yields for prefs at 5%-20% LTV (assuming the prefs tank). And once you get credit hedge funds on the board, potentially representing 33%-50% of directors, it's really hard to predict how it will go for Saylor himself. I think he will avoid that path.

Do you see echostar settling their $2B in converts with cash, stock or combination of both later this month?