Klarna: Inflection Point?

Down 62% since IPO. Hated sector. A two-sided 118m customer network turning the corner with misunderstood potential for a real narrative shift.

KLAR 0.00%↑ was up +20% on Thursday following its first Q1 beat as a public company before coming off a few points with the broader market on Friday. At $5.7B market cap vs. $15B at IPO, is the rally just getting started?

Be water

We were a vocal critic of KLAR 0.00%↑ at the time of its IPO back in September 2025. The market was frothy (with better sector breadth than today) and it seemed clear that their bankers were looking to maximise valuation by inviting “fast money” accounts in order to drive oversubscription.

Employees also had the unusual right to sell stock from Day 1. Add to this the large VC overhang with unlocks around the corner and you had a recipe for challenged near term technicals.

In parallel, broader macro concerns and an increased scrutiny around Private Credit did not help the equity story. Surely, if there are systemic credit issues, consumer lending must be cooked?

Directionally, yes, we were absolutely correct. Admittedly though, we had spent less than 10 minutes understanding the business.

For us it was a clear case of bad technicals + bad narrative. Irrespective of fundamentals, as an equity investor, you just never want to get in front of that.

Turning the corner

Its important to always keep an open mind – after all, we are here to make money. Oversold stocks are generally worth a look and we were now past the lock-up expiry sitting at a <$5B market cap and net cash, which big picture started to sound cheap given they had spent decades building this two-sided network and were clearly tapping into evolving consumer habits.

Given our initial bias, we knew many other investors probably thought the same as us initially: Klarna is an asset heavy, cyclically exposed consumer finance business with capped upside.

Question was: is this a mere dead cat bounce opportunity or something more? Our interest was piqued when we started seeing forward flow agreements on consumer receivables, the growth of Klarna card and delinquency figures that were contained and at levels well below anything subprime.

Situations where market participants are heavily anchored to preconceived notions NOT backed by research are interesting because they offer the opportunity for an early non-consensus view to those who do the work

Variant perception

As we dug in, it was clear that on top a botched IPO and poor technicals, Klarna had been plagued with growing pains as a recently listed Company in a nascent sector – including disclosures that have lacked granularity and management shooting themselves in the foot with guidance – muddying the true trajectory of the business.

We will walk through why we think the market misunderstands both the balance sheet risk profile as well as the growth/profitability runway of the business.

A ~2x from here does not require heroic assumptions beyond a maturation of the existing business.

We also think that there is the opportunity for a much larger re-rate as the market realises that Klarna is:

A difficult to replicate two-sided network, with 119m active customers and 1m merchants, compounding at >25%

A capital efficient credit origination platform

A profitable BNPL business that also acts as a trojan horse towards higher margin, recurring revenue streams

This article is for informational purposes only and does not constitute financial advice. Origo Research may hold positions in securities discussed.

Part 1: Klarna as a BNPL business

The cynical take on Klarna is that they have been growing through aggressive underwriting and over exposing its balance sheet.

The implication being: (i) a saturated market in which Klarna is pursuing the marginal customer with limited edge and (ii) a Damocles sword of credit losses over its head.

Let’s examine that.

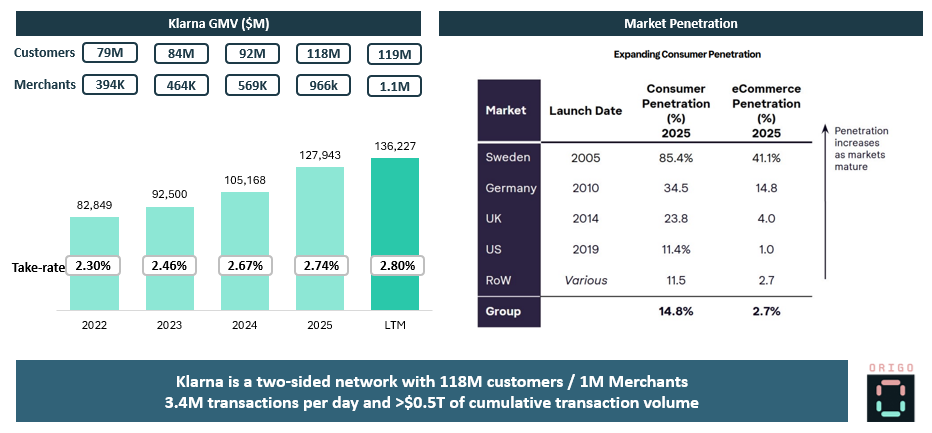

Klarna has grown into a two-sided network comprising 119M customers and >1M merchants, facilitating $136B of GMV globally (21% US / 79% non-US).

The network exists for two main reasons:

up to 20% increase in check-out conversion for merchants

Trusted brand for consumers: flexible payments with no hidden fees

Over the years Klarna has partnered with all the major PSPs (Worldpay, Stripe etc.). It is integrated with Google & Apple Pay and is increasingly a default option at check-out. In Europe, Klarna has dominant market share and brand recognition (particularly in the Nordics and DACH region) while in the US consumer habits are transitioning fast. These are compounding network effects that are difficult to replicate.

Importantly, Klarna’s penetration (and BNPL in general) remains low. Even in its most mature mature market, Sweden, where 85% of adults used Klarna in 2025, the share of wallet was only <7%. There is a very long runway in both consumer adoption (particularly in the US) as well as increased wallet share.

Through March LTM, Klarna GMV grew 29.5% yoy while its revenue grew 33.1% as take-rate increased to 2.8%. Without even getting into additional revenue levers (more on that later), we believe BNPL is a structural growth story and that accelerated US adoption is only a matter of time.

Looking at the balance sheet

While investors generally associate Klarna with an over-extended consumer, the actual risk profile tends to be misunderstood.

Let’s break down the product offering and what it means for Klarna.

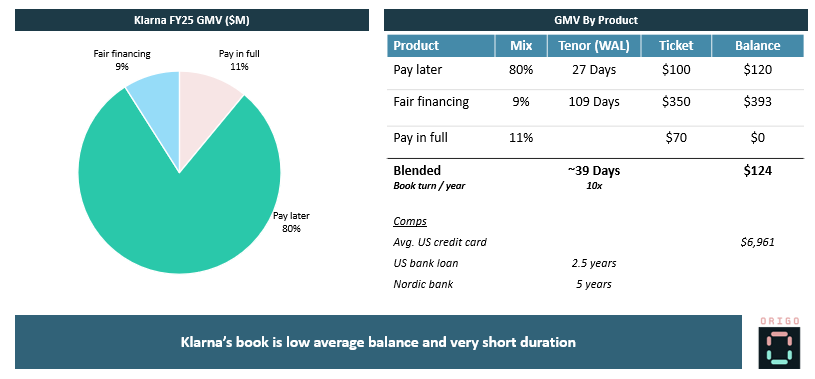

Klarna offers 3 types of products:

Pay later (80% of GMV): this is your charge card equivalent. The customer pays in full within weeks if approved. Klarna pays the merchant at the time of sale with an embedded fee that crystallises on customer repayment (e.g Klarna pays the merchant $97.5 for a $100 ticket)

Fair financing (9% of GMV): customer pays over an extended period (109 days WAL) with a fixed payment date (no rollover or compounding balance). Klarna books both interest income on top of the merchant fee. Klarna only ramps this segment-up based on Pay Later track record.

Pay in full (11% of GMV): customer pays in full at time of sale, Klarna books a merchant fee

Klarna’s model is built on high-frequency, short-duration lending. The average balance per customer is $124. The average duration is 39 days and the book turns over 10x per year. This is very different from a revolving credit card balance (typically ~$7k) or the multi-year tenors associated with bank loans.

From an underwriting perspective:

Klarna has a very fast feedback loop of <60 days to modify standards

The churn amounts to 3.4m transactions / day and $0.5T of cumulative underwritten volume on which to draw from

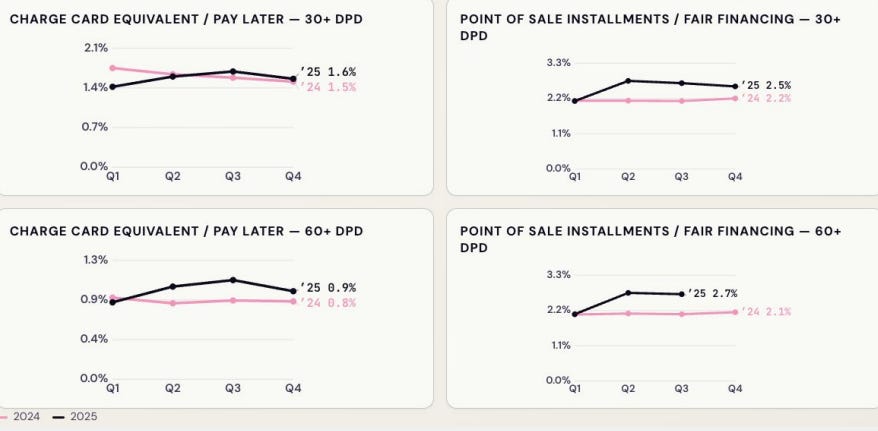

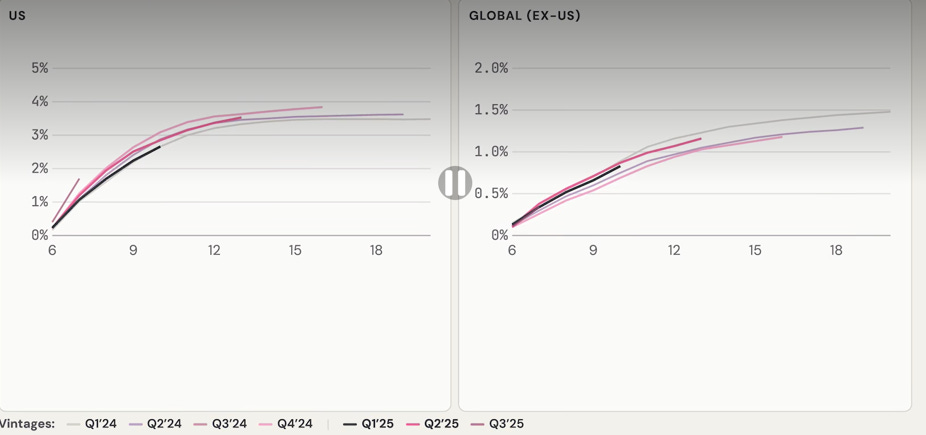

Klarna leans on 30/60 day DPD (as a % of originated volume) as a leading indicator. Pay later 60+ DPDs have remained <1% in Pay Later and <2.7% for fair financing. Note that the numbers below are on a global, blended basis and so there are some mix effects at play.

Because of the longer duration, fair financing is the key segment to watch here.

Net charge-off rates have been stable but what is important to note is that the US carries a different economic profile vs. Global ex-US. Net charge-off rates tend to be <4% whereas Global ex-US is much lower at ~1.5%. This works because the US comes with much higher take-rates. As we will see later, given the growing mix towards both US and fair financing, the blended effects have been source of (unwarranted) confusion and concern for the market, particularly given the lack of geographical disclosure data which only improved as of Thursday this week (Q1 results).

Capital efficiency

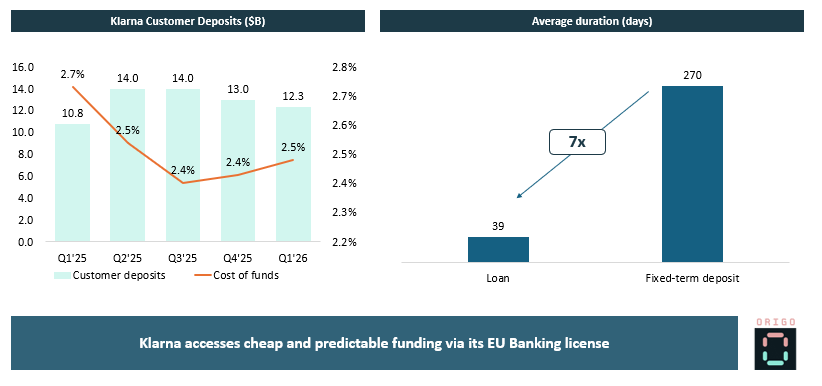

Klarna has an EU banking license and a deposit funded balance sheet:

$12.3B deposits

2.48% cost of funds

Fixed-term deposits: 270 average duration (vs. ~39 day loan duration)

This compares with gross receivables as at Mar-26 stand at $9.6B or $9.2B net of allowance (43% being fair financing).

Additionally, Klarna engages both in forward flow transactions on its US fair financing business as well as SRT or other back-book receivable sales transactions in order to manage its balance sheet.

It recently completed a $1.7B SRT (in Europe) with Varde and has facilities in place with Nelnet and Elliot to scale forward flow sales on its US fair financing business.

The US forward flow business is very new having completed a first transaction in Q4’25 ($1.6B) and a second in Q1’26 ($1.2B).

Klarna’s main US competitor Affirm (who predominantly underwrites longer duration loans) has also successfully tapped in to the ABS market at very tight spreads and this could be an option for Klarna as well down the line.

Klarna is a relative newcomer to public markets and we believe its runway and balance sheet management to be under appreciated if not misunderstood.

This has been exacerbated by accelerated growth in new products / market with the resulting mix masking the profitability profile and longer-term trajectory of the business.

In the rest of this article we go through Klarna’s masked profitability profile, valuation considerations and why we think there is significant re-rate potential.