Gambling Man: Inside Masa's Playground (SoftBank Series Part 1)

Peeling the onion on SoftBank's NAV

“You guys have to listen to me because I am president of this company. In five years, profits have to be 10 billion yen, then in ten years 50 billion. Eventually I want to count profit in trillions of yen!”

– Masayoshi Son in 1981 to his only two (part-time) employees

As a barometer of financial markets, SoftBank’s $370B capital structure spanning equity, CDS, $/€/¥ bonds and hybrids is well worth knowing.

In Part 1 of this series, we peel the onion on SBG’s NAV composition to understand its key drivers. Part 2 will take a closer look at how we think about the various instruments in the capital structure, including potential trade set-ups to express either idiosyncratic views on SBG’s NAV components such as Arm/OpenAI or as a vehicle for broader macro takes through the cycle.

Rolling the dice

Masa has always had a penchant for “running it up.” He makes big, bold bets fuelled by a 50-year personal plan he drafted as a student. Perhaps as a tribute to his Korean ethnicity, Masa only cares about making investments that have the potential to truly move the needle.

Leverage + technological change

Masa realised early on that his best chance for exponential gains was to ride the technological waves of disruption. He also quickly developed an appetite for leveraging OPM (Other People’s Money), getting a first taste for financial engineering when he was an undergraduate student at UC Berkeley importing used arcade machines from Japan funded with supplier financing.

“Masa saw things differently. If you are born in a slum with nothing, losing everything is relative. You just go back to square one. Then, like the Korean slum dwellers in Tosu, you build back up.”

Gambling Man: The Wild Ride of Japan’s Masayoshi Son (Lionel Barber)

In the multiverse of timelines where his bets might have flamed out, we are living in the one where he knocked it out of the part – not once, but multiple times. His early internet plays with Yahoo/Yahoo Japan compounded by his legendary $20m investment in Alibaba (which rescued SoftBank after the Dotcom crash wiped out 99% of its value) laid the foundation for his empire.

Masa’s appetite for size and willingness to embrace volatility has often led the public to label him as halfway between genius and crazy. When he raised the first Vision Fund in 2017 at $100B (again, leveraging OPM through Saudi Arabia’s PIF), some Silicon Valley elites would even refer to him as “dumb money” behind closed doors, blaming (or thanking) him for inflating valuations of late-stage companies.

It looked like everything would come crashing down for him during the COVID-crisis – the poster child for market excess, amplified by misplaced bets in WeWork and others. Not one to lack confidence though as SoftBank’s NAV suffered a 50% drawdown, he published this legendary slide about unicorns jumping over the “Valley of Coronavirus”.

While many counted him out or even mocked him, just like the Dotcom bubble, he did in fact make it out on the other side having successfully recycled his capital base. Despite selling NVIDIA too early (his stake would be worth close to the current market cap of SBG), his NAV today sits close to ATH with levered bets on chipmaker Arm as well as OpenAI.

With his new bets in play, are we in store for the next growth spurt in Masa’s Empire? Or will we see yet another 50% drawdown on his path to glory?

Infinite outcomes

What makes SoftBank so fascinating is its wide range of potential outcomes.

SoftBank Group’s share price was up 16% this week and is +40% YTD, in reach of its ATH. In seemingly contradictory fashion, SoftBank’s 5Y CDS has widened to 342 bps implying a non-trivial probability of default.

This may not be so counterintuitive since a barbell approach may make sense when both right and left tail events are in play (more on this in Part 2).

For now, let’s take a look at what sits inside SoftBank and what makes it so swingy as we look to establish a lower and upper bound range on its NAV.

Inside SBG: unpacking the black box

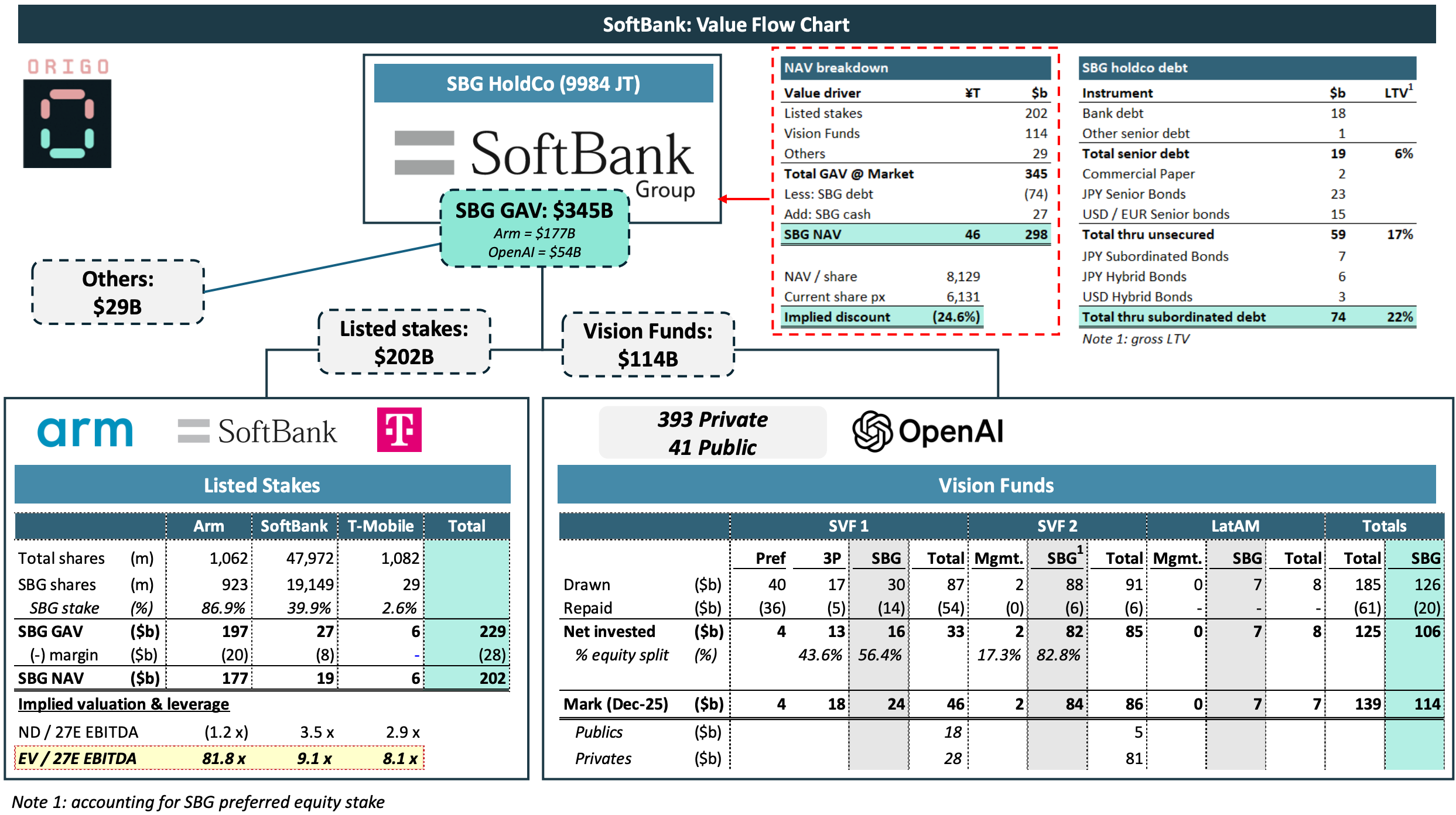

SoftBank Group (“SBG”) is a pure HoldCo (since spinning off its telecom subsidiary, SoftBank, in 2015). Today, there is approximately $345B of GAV (gross asset value) that flows to the HoldCo (net of OpCo debt or other margin loans). Additionally there is $74B of HoldCo level debt and $27B of cash which ultimately feed into the NAV calculation.

SBG value flow chart

There are two primary components to SBG’s $345B GAV: direct stakes it holds in listed companies ($202B) and its interest in the Vision Funds ($114B). In addition, there is $29B of value which flows through through from its NAV share in SB Northstar (its investment vehicle / asset management subsidiary) including various other miscellaneous listed/unlisted stakes.

Side note for any budding investment analyst reading this: no matter how complex a conglomerate / company appears, you should be able to breakdown and visualise the value flow on a single page like this. Consolidated figures in the case of SoftBank are misleading and do not properly tell the story.

Let’s now go through the underlying drivers in detail.